Question

Eva received $68,000 in compensation payments from JAZZ Corp. during 2018. Eva incurred $13,500 in business expenses relating to her work for JAZZ Corp. JAZZ

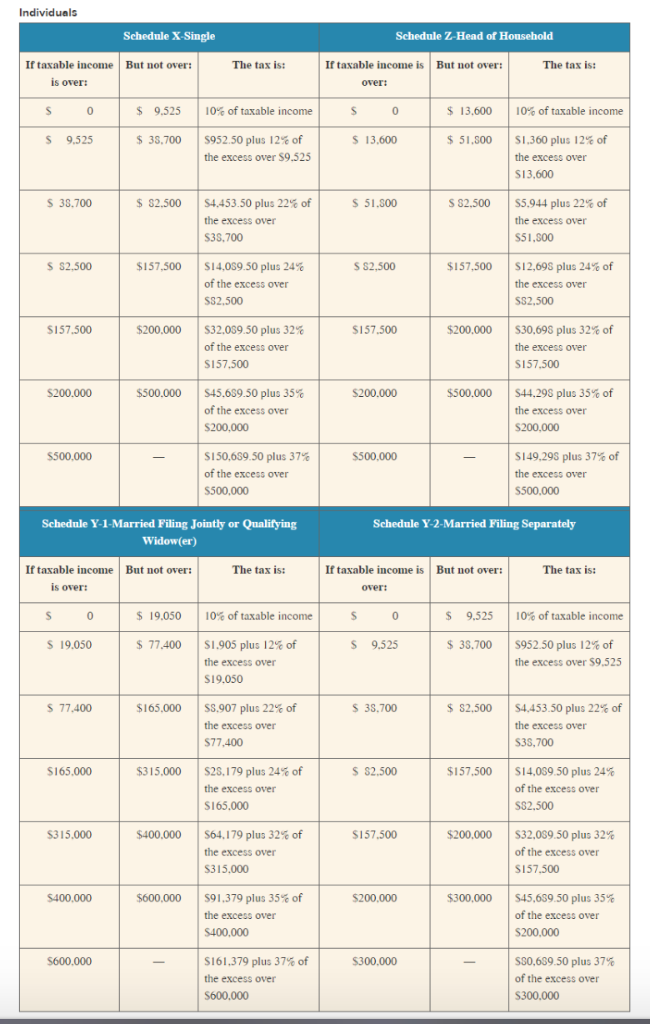

Eva received $68,000 in compensation payments from JAZZ Corp. during 2018. Eva incurred $13,500 in business expenses relating to her work for JAZZ Corp. JAZZ did not reimburse Eva for any of these expenses. Eva is single and she deducts a standard deduction of $12,000. Based on these facts answer the following questions: Use Tax Rate Schedule for reference.

a. Assume that Eva is considered to be an employee. What amount of FICA taxes is she required to pay for the year?

b. Assume that Eva is considered to be an employee. What is her regular income tax liability for the year?

c. Assume that Eva is considered to be a self-employed contractor. What is her self-employment tax liability and additional Medicare tax liability for the year?

d. Assume that Eva is considered to be a self-employed contractor. What is her regular tax liability for the year?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Audit Of The Universe Are We Guarding Our Cocooning Atmosphere Watching Over Our Life Giving Water And Fertile Soil Respecting Our Nourishing Flora And Prodigious Fauna Are We Managing Earths Resources For Better Or Worse

Authors: Sam Kneller

1st Edition

B08DBYMT4K, 979-8668249695