Answered step by step

Verified Expert Solution

Question

1 Approved Answer

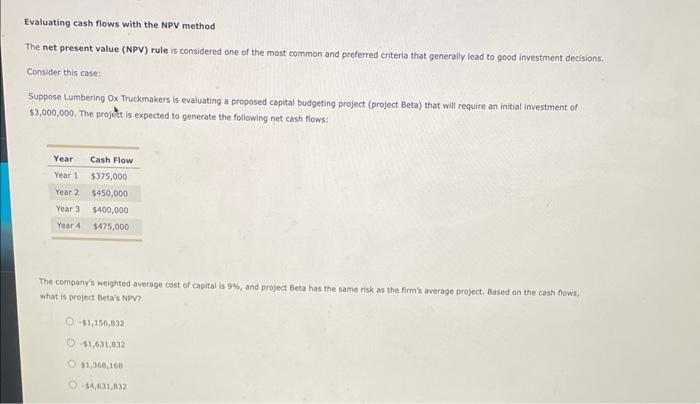

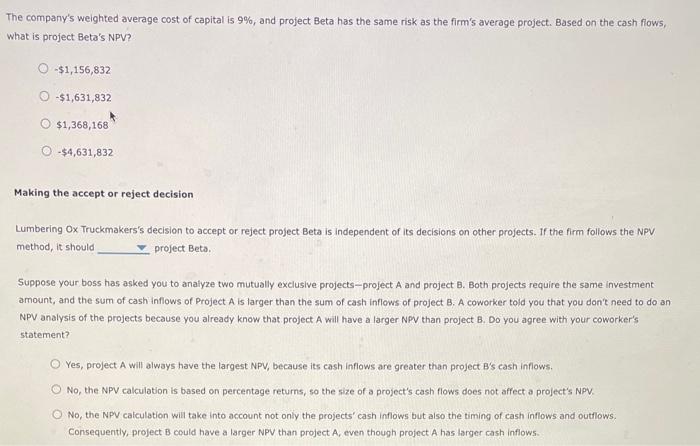

Evaluating cash flows with the NPV method The net present value (NPV) rule is considered one of the most common and preferred criteria that generally

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

How To Become An Exceptional Real Estate Investor Becoming The Unique And Valued Real Estate Investor

Authors: Alexander Eichmann

1st Edition

979-8864277386