Answered step by step

Verified Expert Solution

Question

1 Approved Answer

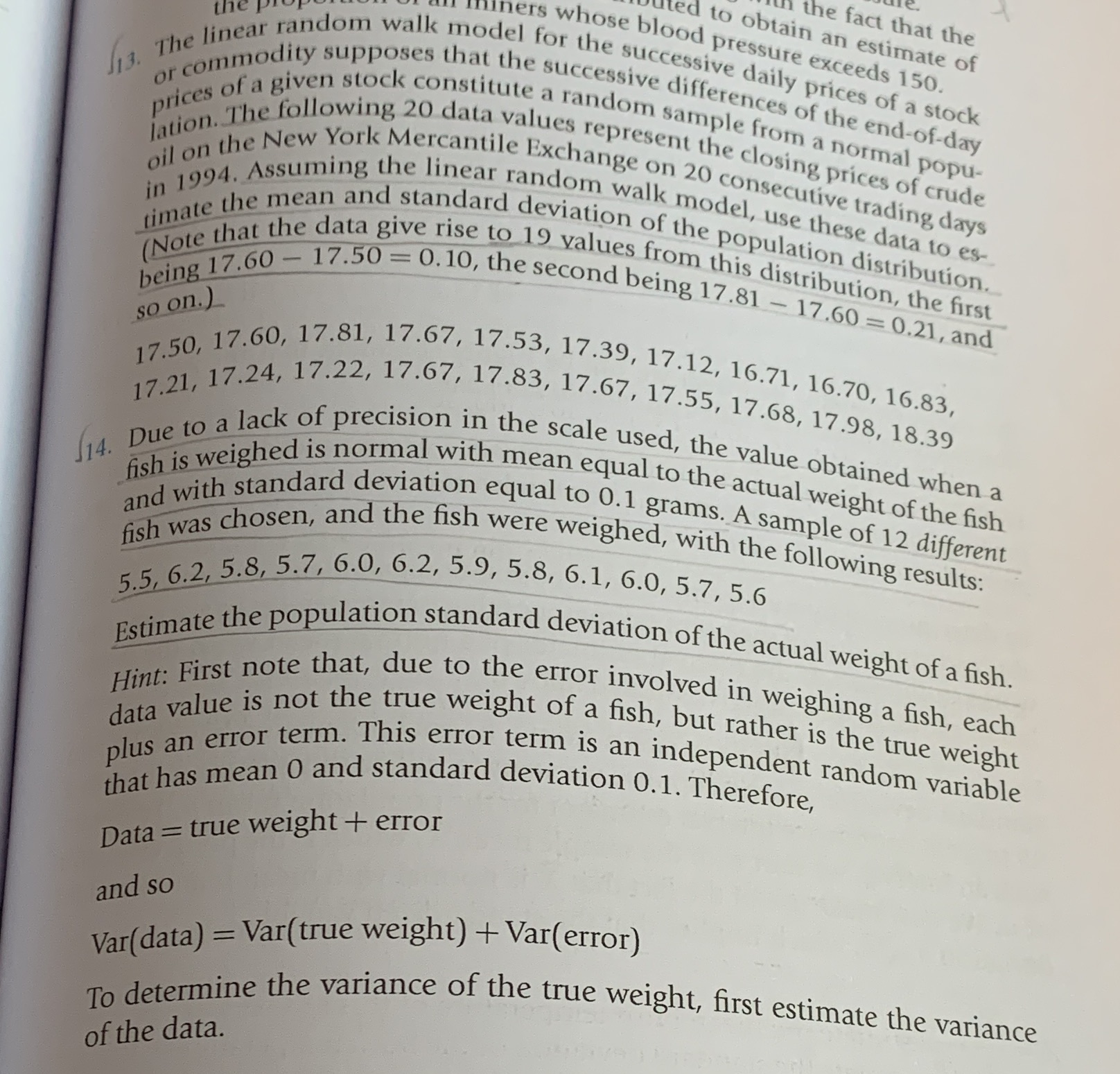

Ex. 13,14 in the fact that the ited to obtain an estimate of Iners whose blood pressure exceeds 150. The linear random walk model for

Ex. 13,14

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Recent Developments Of Mathematical Fluid Mechanics

Authors: Herbert Amann, Yoshikazu Giga, Hideo Kozono, Hisashi Okamoto, Masao Yamazaki

1st Edition

3034809395, 9783034809399