Answered step by step

Verified Expert Solution

Question

1 Approved Answer

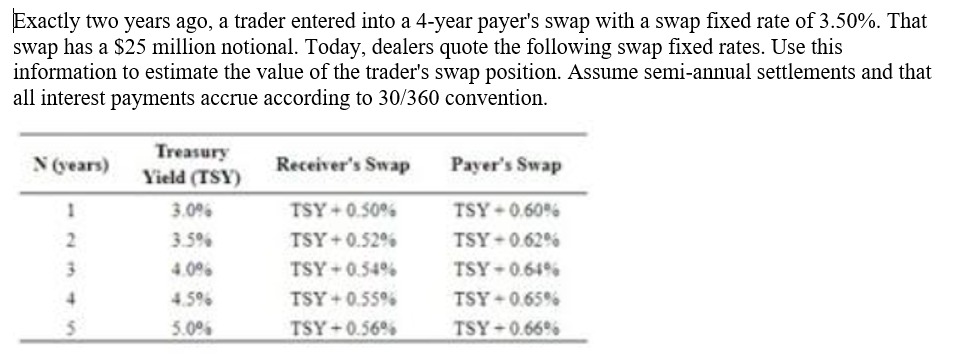

Exactly two years ago, a trader entered into a 4 - year payer's swap with a swap fixed rate of 3 . 5 0 %

Exactly two years ago, a trader entered into a year payer's swap with a swap fixed rate of That

swap has a $ million notional. Today, dealers quote the following swap fixed rates. Use this

information to estimate the value of the trader's swap position. Assume semiannual settlements and that

all interest payments accrue according to convention.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Ecological Money And Finance

Authors: Thomas Lagoarde-Segot

1st Edition

3031142314, 978-3031142314