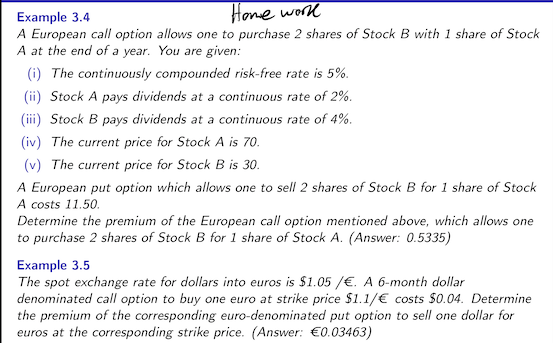

Example 3.4 Home world A European call option allows one to purchase 2 shares of Stock B with 1 share of Stock A at the end of a year. You are given: () The continuously compounded risk-free rate is 5% (ii) Stock A pays dividends at a continuous rate of 2%. (ii) Stock B pays dividends at a continuous rate of 4%. (iv) The current price for Stock A is 70. (v) The current price for Stock Bis 30. A European put option which allows one to sell 2 shares of Stock B for 1 share of Stock A costs 11.50 Determine the premium of the European call option mentioned above, which allows one to purchase 2 shares of Stock B for 1 share of Stock A. (Answer: 0.5335) Example 3.5 The spot exchange rate for dollars into euros is $1.05 /. A 6-month dollar denominated call option to buy one euro at strike price $1.1/ costs $0.04. Determine the premium of the corresponding euro-denominated put option to sell one dollar for euros at the corresponding strike price. (Answer: 0.03463) Example 3.4 Home world A European call option allows one to purchase 2 shares of Stock B with 1 share of Stock A at the end of a year. You are given: () The continuously compounded risk-free rate is 5% (ii) Stock A pays dividends at a continuous rate of 2%. (ii) Stock B pays dividends at a continuous rate of 4%. (iv) The current price for Stock A is 70. (v) The current price for Stock Bis 30. A European put option which allows one to sell 2 shares of Stock B for 1 share of Stock A costs 11.50 Determine the premium of the European call option mentioned above, which allows one to purchase 2 shares of Stock B for 1 share of Stock A. (Answer: 0.5335) Example 3.5 The spot exchange rate for dollars into euros is $1.05 /. A 6-month dollar denominated call option to buy one euro at strike price $1.1/ costs $0.04. Determine the premium of the corresponding euro-denominated put option to sell one dollar for euros at the corresponding strike price. (Answer: 0.03463)