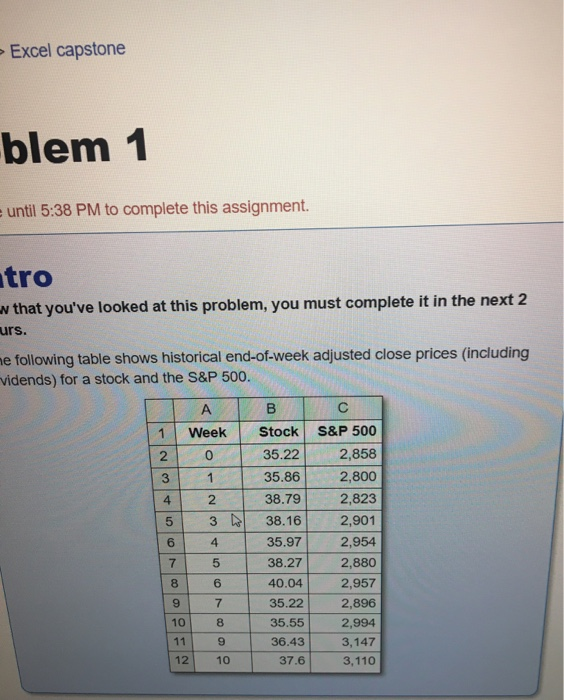

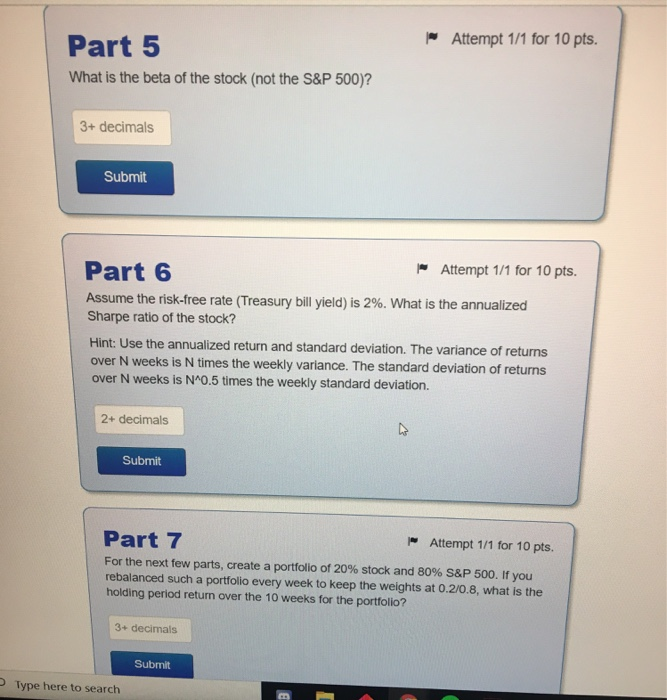

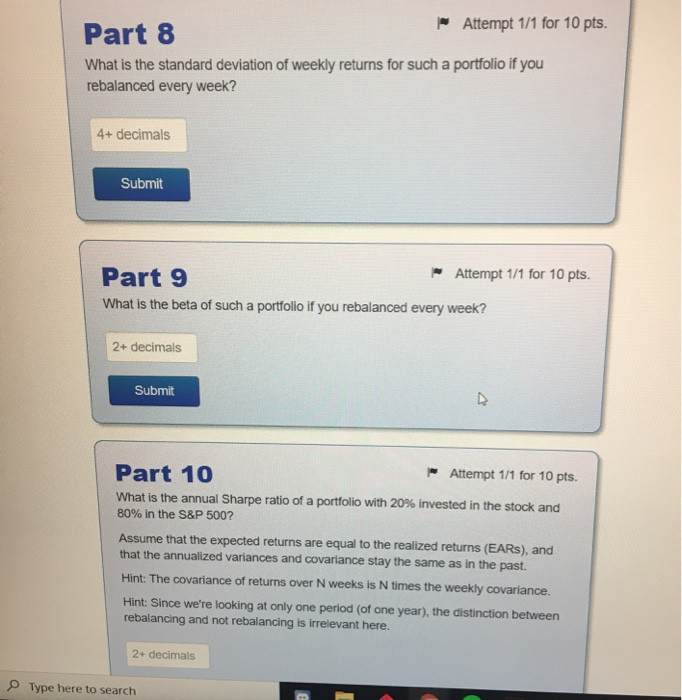

Excel capstone blem 1 until 5:38 PM to complete this assignment. tro w that you've looked at this problem, you must complete it in the next 2 urs. me following table shows historical end-of-week adjusted close prices (including vidends) for a stock and the S&P 500. A B 1 Week 0 ON 1 Stock 35.22 35.86 38.79 38.16 35.97 4 4 2 5 3 4 S&P 500 2,858 2,800 2,823 2,901 2,954 2,880 2,957 2,896 2,994 3,147 3,110 6 7 5 38.27 00 6 40.04 9 7 10 8 35.22 35.55 36.43 11 9 12 10 37.6 Attempt 1/1 for 10 pts. Part 5 What is the beta of the stock (not the S&P 500)? 3+ decimals Submit Part 6 | Attempt 1/1 for 10 pts. Assume the risk-free rate (Treasury bill yield) is 2%. What is the annualized Sharpe ratio of the stock? Hint: Use the annualized return and standard deviation. The variance of returns over N weeks is N times the weekly variance. The standard deviation of returns over N weeks is N^0.5 times the weekly standard deviation. 2+ decimals a Submit Part 7 Attempt 1/1 for 10 pts. For the next few parts, create a portfolio of 20% stock and 80% S&P 500. If you rebalanced such a portfolio every week to keep the weights at 0.2/0.8, what is the holding period return over the 10 weeks for the portfolio? 3+ decimals Submit Type here to search Part 8 Attempt 1/1 for 10 pts. What is the standard deviation of weekly returns for such a portfolio if you rebalanced every week? 4+ decimals Submit Part 9 Attempt 1/1 for 10 pts. What is the beta of such a portfolio if you rebalanced every week? 2+ decimals Submit Part 10 Attempt 1/1 for 10 pts. What is the annual Sharpe ratio of a portfolio with 20% invested in the stock and 80% in the S&P 500? Assume that the expected returns are equal to the realized returns (EARS), and that the annualized variances and covariance stay the same as in the past. Hint: The covariance of returns over N weeks is N times the weekly covariance. Hint: Since we're looking at only one period (of one year), the distinction between rebalancing and not rebalancing is irrelevant here. 2-decimals Type here to search Excel capstone blem 1 until 5:38 PM to complete this assignment. tro w that you've looked at this problem, you must complete it in the next 2 urs. me following table shows historical end-of-week adjusted close prices (including vidends) for a stock and the S&P 500. A B 1 Week 0 ON 1 Stock 35.22 35.86 38.79 38.16 35.97 4 4 2 5 3 4 S&P 500 2,858 2,800 2,823 2,901 2,954 2,880 2,957 2,896 2,994 3,147 3,110 6 7 5 38.27 00 6 40.04 9 7 10 8 35.22 35.55 36.43 11 9 12 10 37.6 Attempt 1/1 for 10 pts. Part 5 What is the beta of the stock (not the S&P 500)? 3+ decimals Submit Part 6 | Attempt 1/1 for 10 pts. Assume the risk-free rate (Treasury bill yield) is 2%. What is the annualized Sharpe ratio of the stock? Hint: Use the annualized return and standard deviation. The variance of returns over N weeks is N times the weekly variance. The standard deviation of returns over N weeks is N^0.5 times the weekly standard deviation. 2+ decimals a Submit Part 7 Attempt 1/1 for 10 pts. For the next few parts, create a portfolio of 20% stock and 80% S&P 500. If you rebalanced such a portfolio every week to keep the weights at 0.2/0.8, what is the holding period return over the 10 weeks for the portfolio? 3+ decimals Submit Type here to search Part 8 Attempt 1/1 for 10 pts. What is the standard deviation of weekly returns for such a portfolio if you rebalanced every week? 4+ decimals Submit Part 9 Attempt 1/1 for 10 pts. What is the beta of such a portfolio if you rebalanced every week? 2+ decimals Submit Part 10 Attempt 1/1 for 10 pts. What is the annual Sharpe ratio of a portfolio with 20% invested in the stock and 80% in the S&P 500? Assume that the expected returns are equal to the realized returns (EARS), and that the annualized variances and covariance stay the same as in the past. Hint: The covariance of returns over N weeks is N times the weekly covariance. Hint: Since we're looking at only one period (of one year), the distinction between rebalancing and not rebalancing is irrelevant here. 2-decimals Type here to search