Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Excel formulas would be preferred, but answer it please :) The hypothetical sequential-pay structure with floater, inverse floater, and accrual bond classes AND the collateral

Excel formulas would be preferred, but answer it please :)

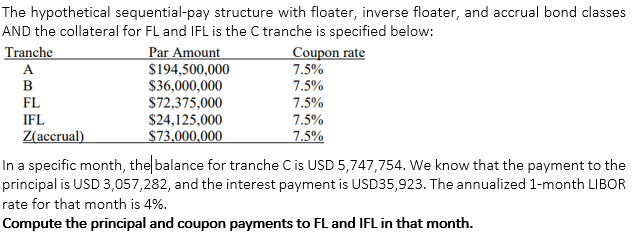

The hypothetical sequential-pay structure with floater, inverse floater, and accrual bond classes AND the collateral for FL and IFL is the C tranche is specified below: Tranche Par Amount Coupon rate A $194,500,000 7.5% B $36,000,000 7.5% FL $72,375,000 7.5% IFL $24,125,000 7.5% Zaccrual) $73,000,000 7.5% In a specific month, the balance for tranche Cis USD 5,747,754. We know that the payment to the principal is USD 3,057,282, and the interest payment is USD35,923. The annualized 1-month LIBOR rate for that month is 4%. Compute the principal and coupon payments to FL and IFL in that month. The hypothetical sequential-pay structure with floater, inverse floater, and accrual bond classes AND the collateral for FL and IFL is the C tranche is specified below: Tranche Par Amount Coupon rate A $194,500,000 7.5% B $36,000,000 7.5% FL $72,375,000 7.5% IFL $24,125,000 7.5% Zaccrual) $73,000,000 7.5% In a specific month, the balance for tranche Cis USD 5,747,754. We know that the payment to the principal is USD 3,057,282, and the interest payment is USD35,923. The annualized 1-month LIBOR rate for that month is 4%. Compute the principal and coupon payments to FL and IFL in that monthStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Matlab An Introduction with Applications

Authors: Amos Gilat

5th edition

1118629868, 978-1118801802, 1118801806, 978-1118629864