Answered step by step

Verified Expert Solution

Question

1 Approved Answer

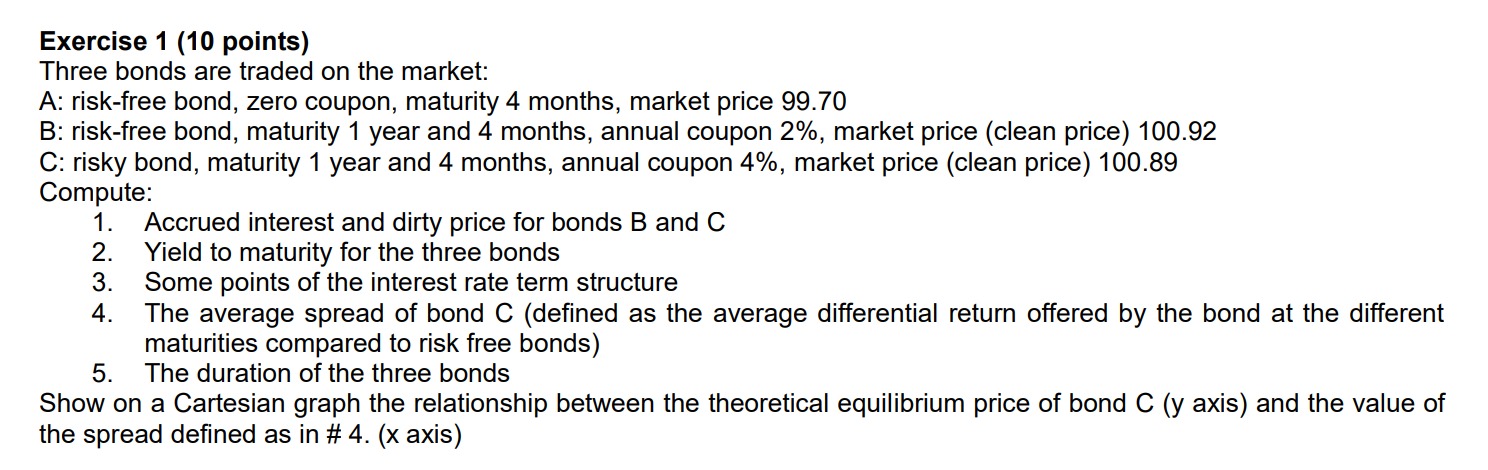

Exercise 1 ( 1 0 points ) Three bonds are traded on the market: A: risk - free bond, zero coupon, maturity 4 months, market

Exercise points

Three bonds are traded on the market:

A: riskfree bond, zero coupon, maturity months, market price

B: riskfree bond, maturity year and months, annual coupon market price clean price

C: risky bond, maturity year and months, annual coupon market price clean price

Compute:

Accrued interest and dirty price for bonds B and

Yield to maturity for the three bonds

Some points of the interest rate term structure

The average spread of bond defined as the average differential return offered by the bond at the different

maturities compared to risk free bonds

The duration of the three bonds

Show on a Cartesian graph the relationship between the theoretical equilibrium price of bond axis and the value of

the spread defined as in # x axis

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Project Finance In Theory And Practice Designing Structuring And Financing Private And Public Projects

Authors: Stefano Gatti

4th Edition

032398360X, 9780323983600