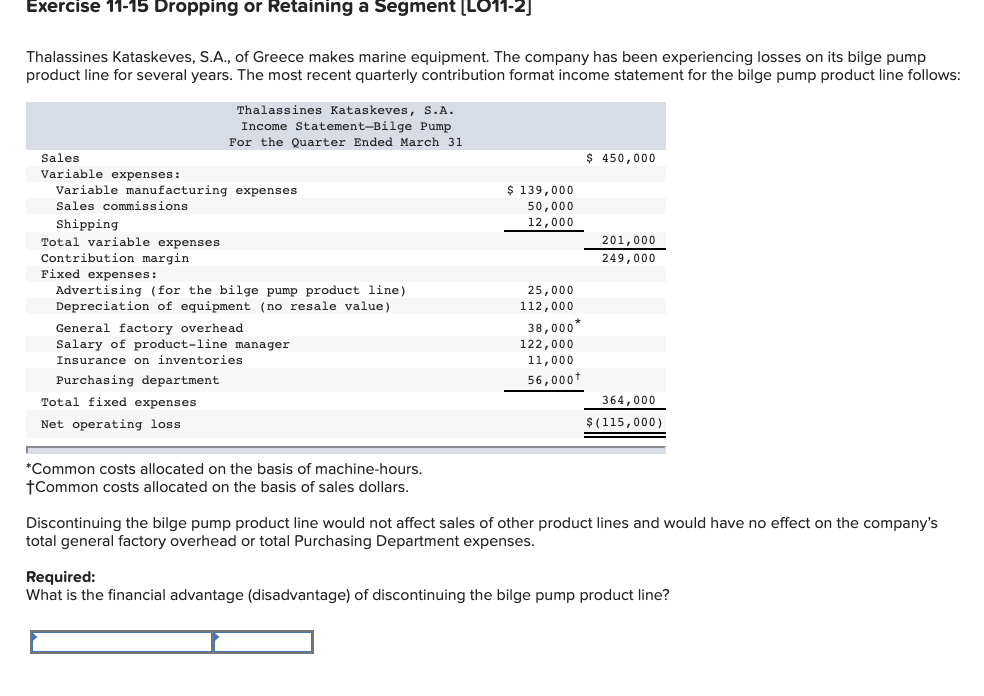

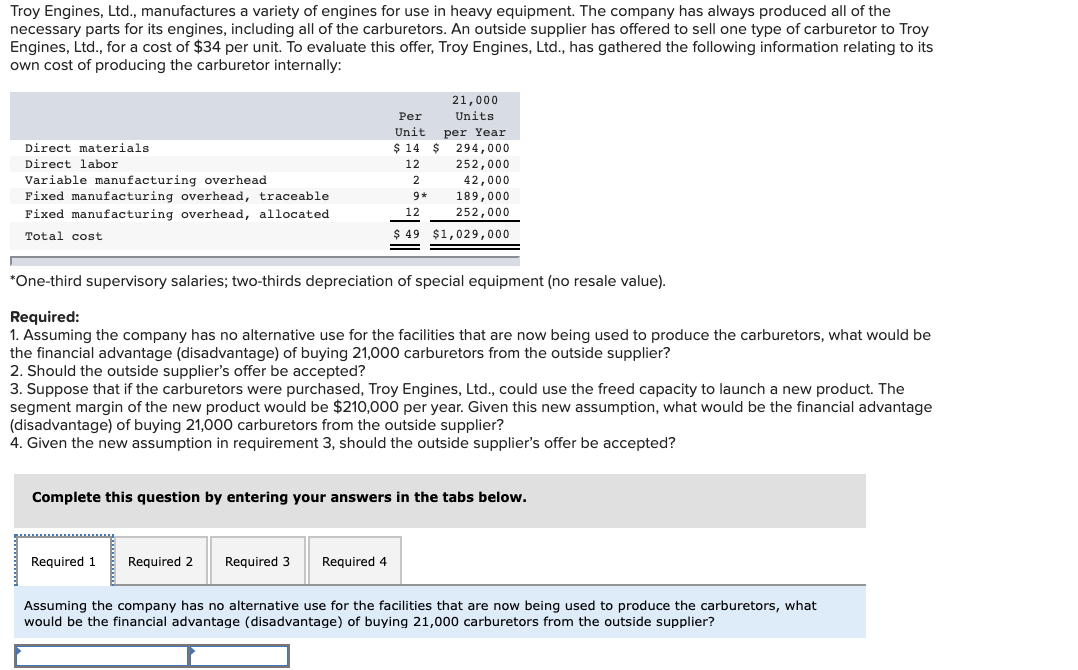

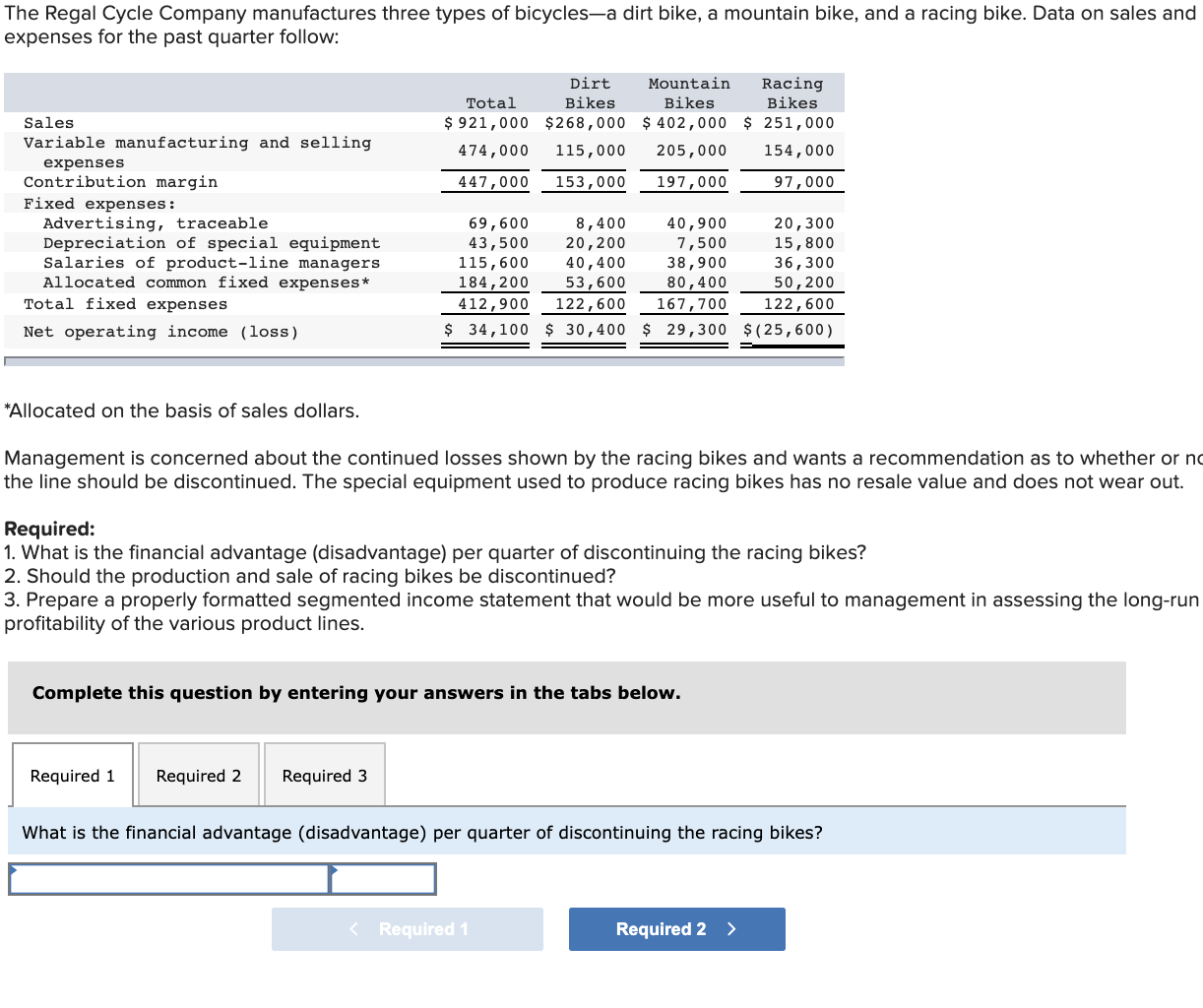

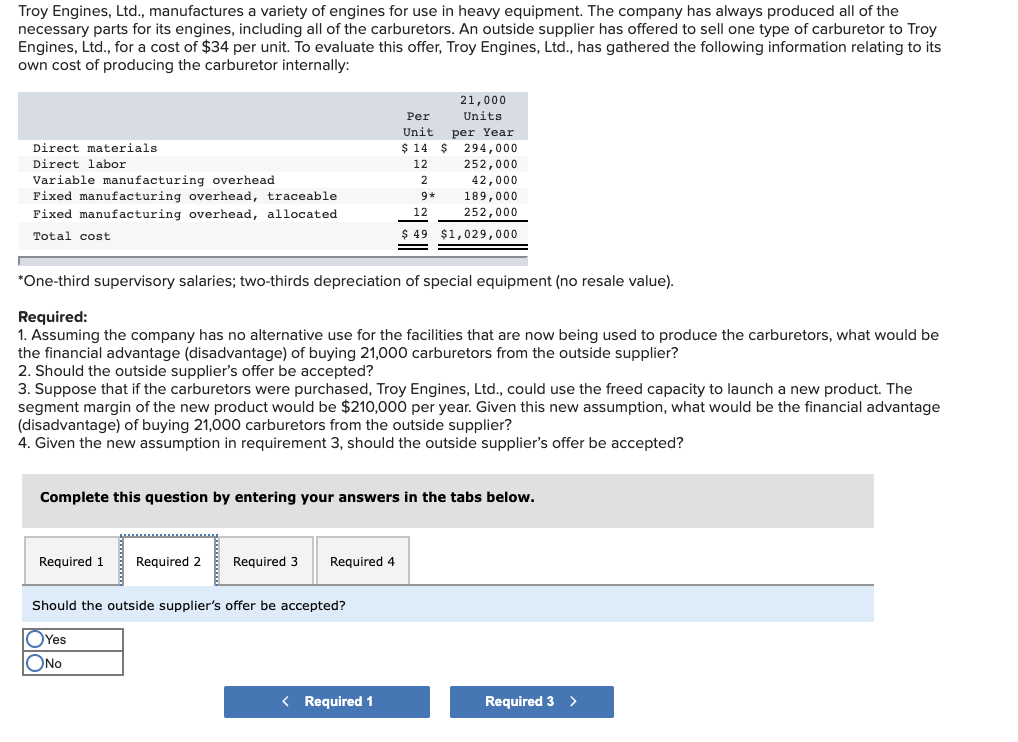

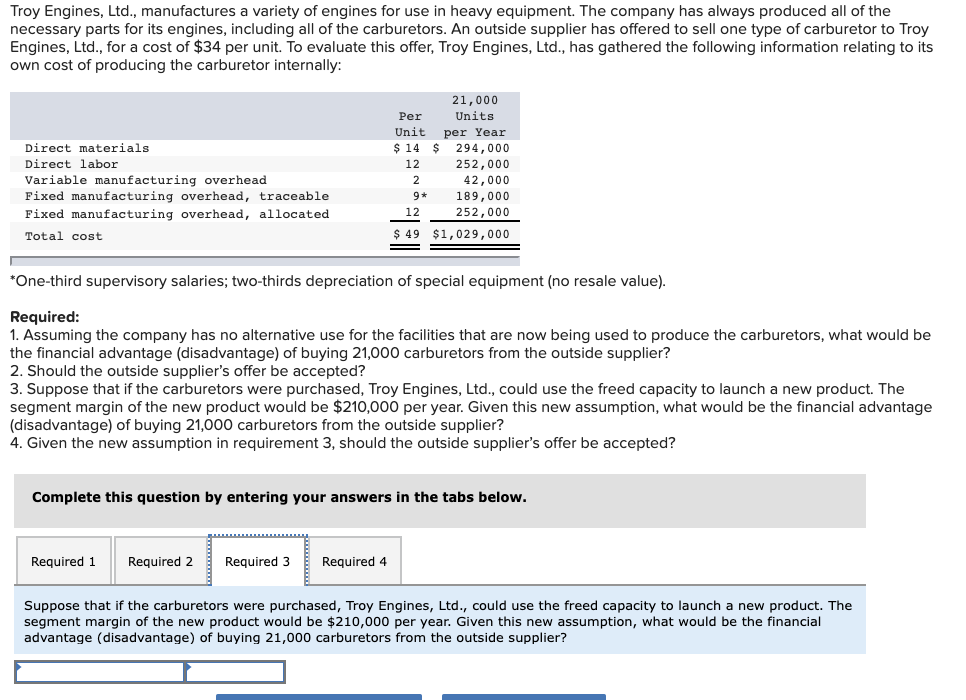

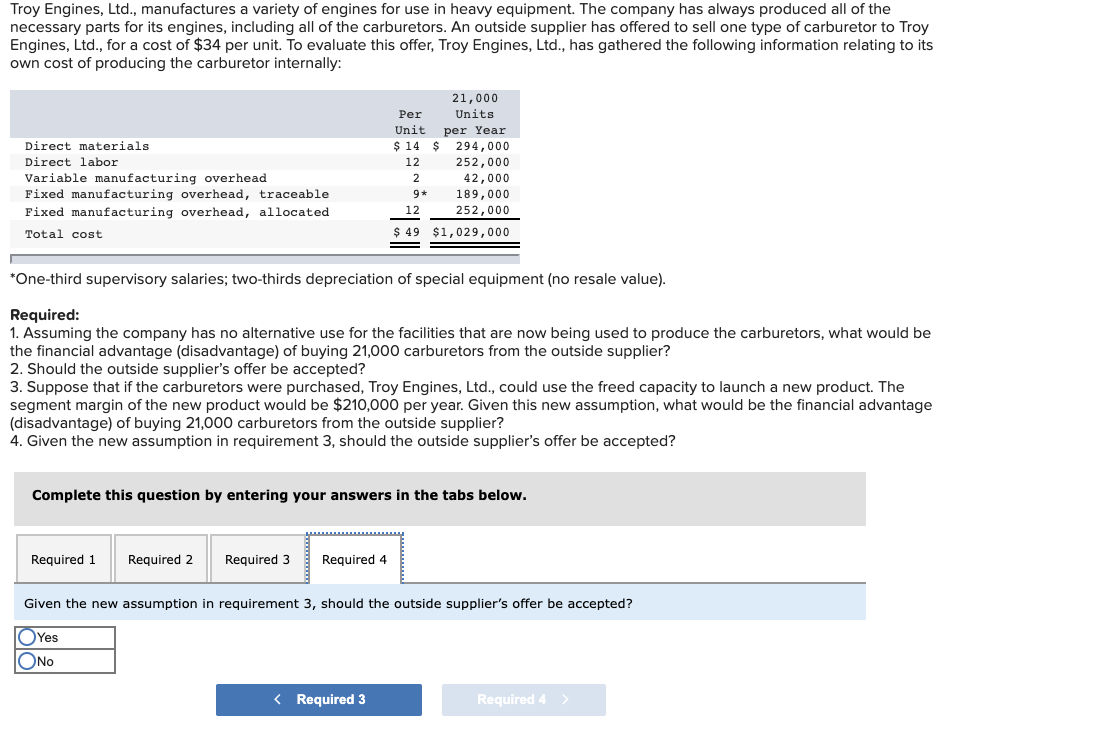

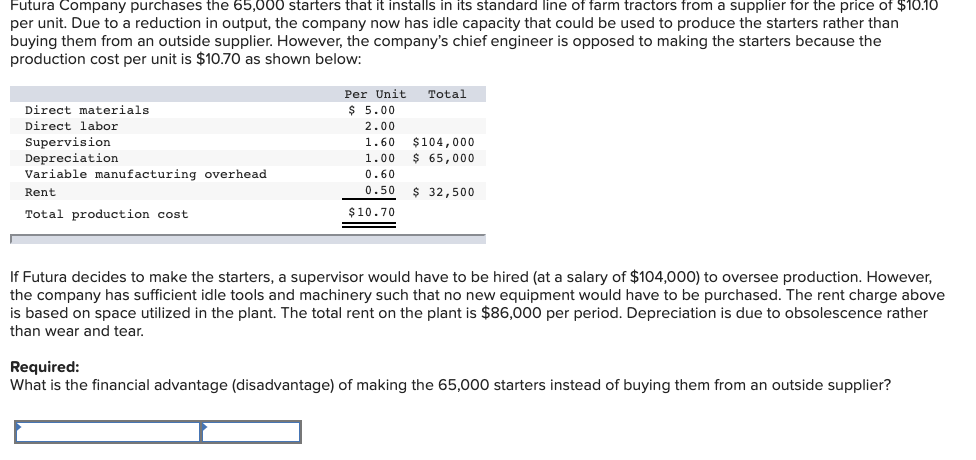

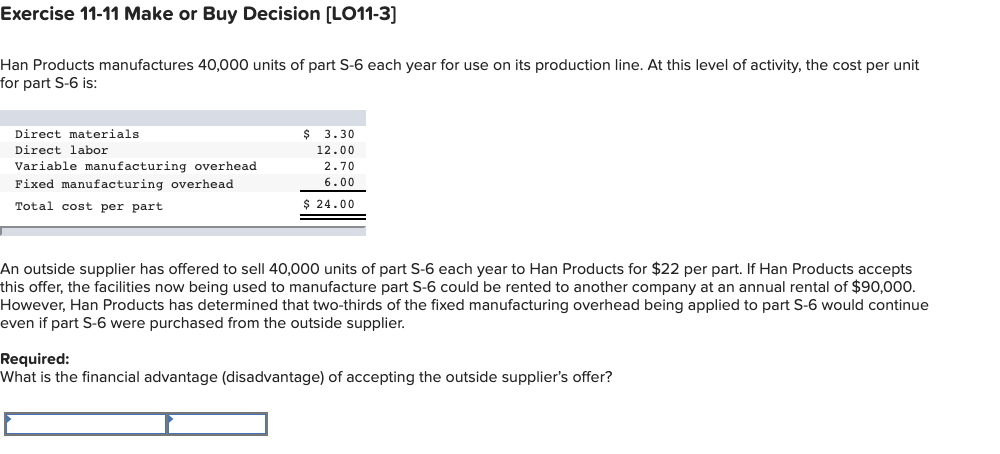

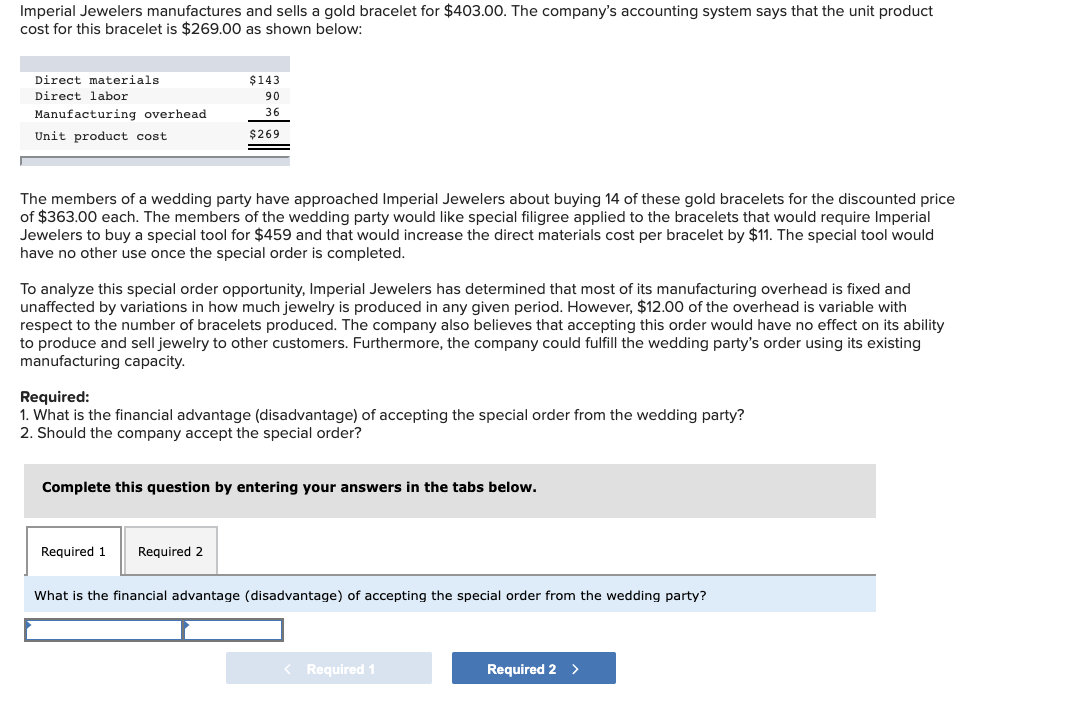

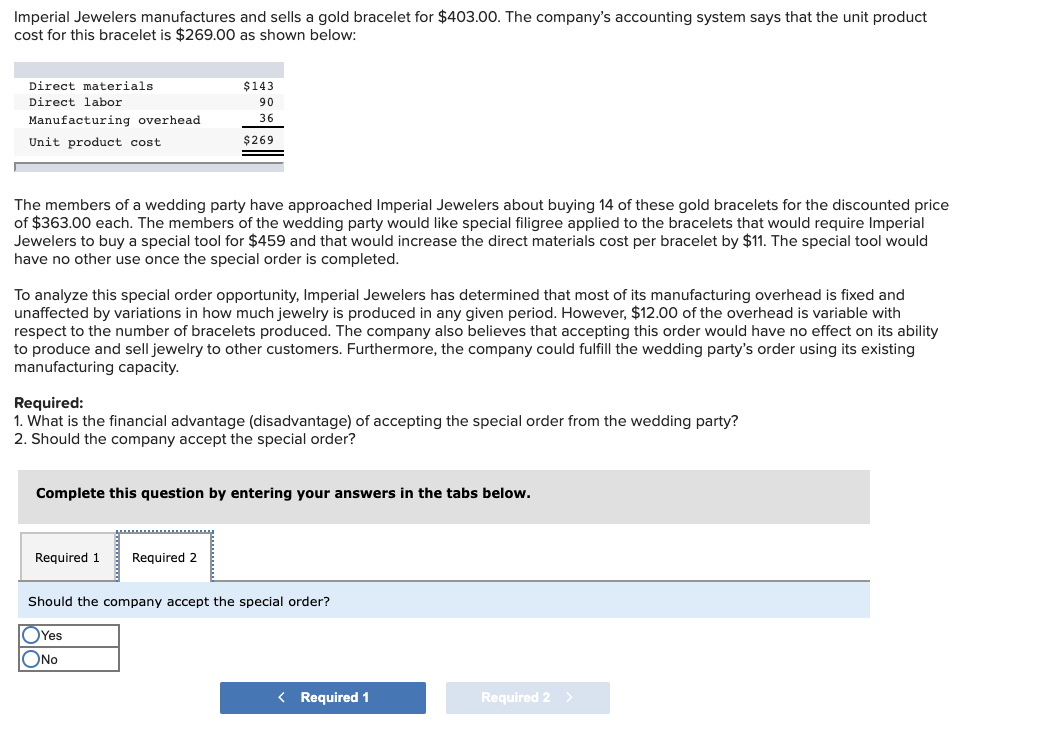

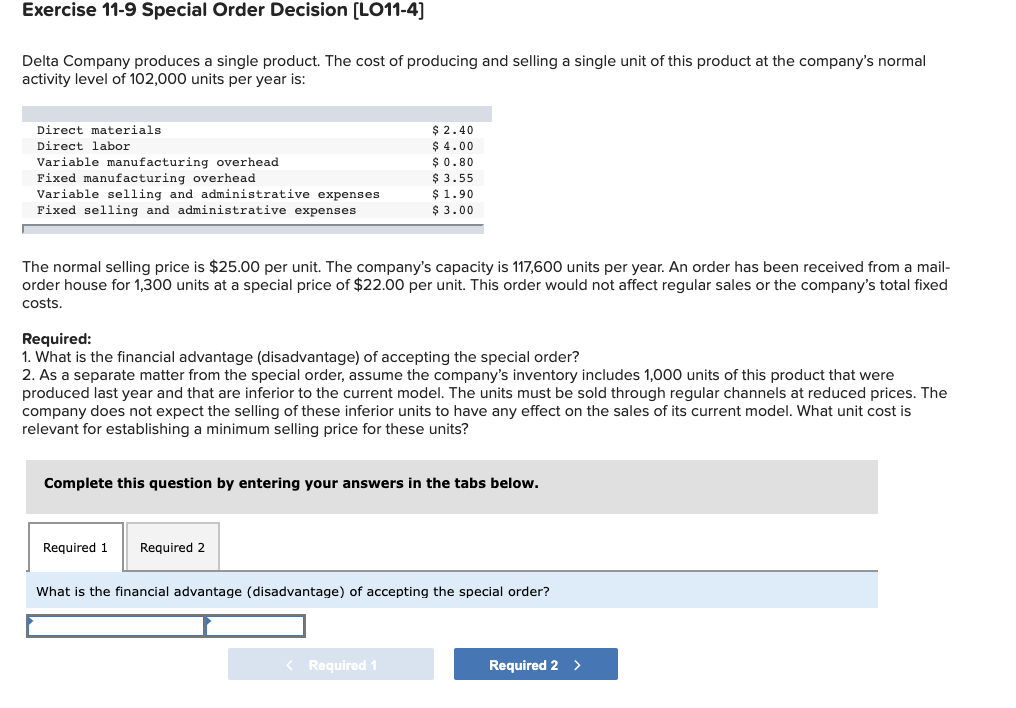

Exercise 11-15 Dropping or Retaining a Segment (LO11-2) Thalassines kataskeves, S.A., of Greece makes marine equipment. The company has been experiencing losses on its bilge pump product line for several years. The most recent quarterly contribution format income statement for the bilge pump product line follows: $ 450,000 $ 139,000 50,000 12,000 201,000 249,000 Thalassines Kataskeves, S.A. Income Statement-Bilge Pump For the Quarter Ended March 31 Sales Variable expenses: Variable manufacturing expenses Sales commissions Shipping Total variable expenses Contribution margin Fixed expenses: Advertising (for the bilge pump product line) Depreciation of equipment (no resale value) General factory overhead Salary of product-line manager Insurance on inventories Purchasing department Total fixed expenses Net operating loss 25,000 112,000 38,000* 122,000 11,000 56,000+ 364,000 $(115, 000) *Common costs allocated on the basis of machine-hours. Common costs allocated on the basis of sales dollars. Discontinuing the bilge pump product line would not affect sales of other product lines and would have no effect on the company's total general factory overhead or total Purchasing Department expenses. Required: What is the financial advantage (disadvantage) of discontinuing the bilge pump product line? Troy Engines, Ltd., manufactures a variety of engines for use in heavy equipment. The company has always produced all of the necessary parts for its engines, including all of the carburetors. An outside supplier has offered to sell one type of carburetor to Troy Engines, Ltd., for a cost of $34 per unit. To evaluate this offer, Troy Engines, Ltd., has gathered the following information relating to its own cost of producing the carburetor internally: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead, traceable Fixed manufacturing overhead, allocated Total cost 21,000 Per Units Unit per Year $ 14 $ 294,000 12 252,000 2 42,000 9* 189,000 12 252,000 $ 49 $1,029,000 *One-third supervisory salaries; two-thirds depreciation of special equipment (no resale value). Required: 1. Assuming the company has no alternative use for the facilities that are now being used to produce the carburetors, what would be the financial advantage (disadvantage) of buying 21,000 carburetors from the outside supplier? 2. Should the outside supplier's offer be accepted? 3. Suppose that if the carburetors were purchased, Troy Engines, Ltd., could use the freed capacity to launch a new product. The segment margin of the new product would be $210,000 per year. Given this new assumption, what would be the financial advantage (disadvantage) of buying 21,000 carburetors from the outside supplier? 4. Given the new assumption in requirement 3, should the outside supplier's offer be accepted? Complete this question by entering your answers in the tabs below. Required 1 Required 2 Required 3 Required 4 Assuming the company has no alternative use for the facilities that are now being used to produce the carburetors, what would be the financial advantage (disadvantage) of buying 21,000 carburetors from the outside supplier? The Regal Cycle Company manufactures three types of bicycles-a dirt bike, a mountain bike, and a racing bike. Data on sales and expenses for the past quarter follow: Dirt Mountain Racing Total Bikes Bikes Bikes $ 921,000 $268,000 $ 402,000 $ 251,000 474,000 115,000 205,000 154,000 447,000 153,000 197,000 97,000 Sales Variable manufacturing and selling expenses Contribution margin Fixed expenses: Advertising, traceable Depreciation of special equipment Salaries of product-line managers Allocated common fixed expenses* Total fixed expenses Net operating income (loss) 69,600 8,400 40,900 20,300 43,500 20,200 7,500 15,800 115,600 40,400 38,900 36,300 184,200 53,600 80,400 50,200 412,900 122,600 167,700 122,600 $ 34,100 $ 30,400 $ 29,300 $(25,600) *Allocated on the basis of sales dollars. Management is concerned about the continued losses shown by the racing bikes and wants a recommendation as to whether or no the line should be discontinued. The special equipment used to produce racing bikes has no resale value and does not wear out. Required: 1. What is the financial advantage (disadvantage) per quarter of discontinuing the racing bikes? 2. Should the production and sale of racing bikes be discontinued? 3. Prepare a properly formatted segmented income statement that would be more useful to management in assessing the long-run profitability of the various product lines. Complete this question by entering your answers in the tabs below. Required 1 Required 2 Required 3 What is the financial advantage (disadvantage) per quarter of discontinuing the racing bikes? The Regal Cycle Company manufactures three types of bicycles-a dirt bike, a mountain bike, and a racing bike. Data on sales and expenses for the past quarter follow: Dirt Mountain Racing Total Bikes Bikes Bikes $ 921,000 $268,000 $ 402,000 $ 251,000 474,000 115,000 205,000 154,000 447,000 153,000 197,000 97,000 Sales Variable manufacturing and selling expenses Contribution margin Fixed expenses: Advertising, traceable Depreciation of special equipment Salaries of product-line managers Allocated common fixed expenses* Total fixed expenses Net operating income (loss) 69,600 8,400 40,900 20,300 43,500 20,200 7,500 15,800 115,600 40,400 38,900 36,300 184,200 53,600 80,400 50,200 412,900 122,600 167,700 122,600 $ 34,100 $ 30,400 $ 29,300 $(25,600) *Allocated on the basis of sales dollars. Management is concerned about the continued losses shown by the racing bikes and wants recommendation as to whether or not the line should be discontinued. The special equipment used to produce racing bikes has no resale value and does not wear out. Required: 1. What is the financial advantage (disadvantage) per quarter of discontinuing the racing bikes? 2. Should the production and sale of racing bikes be discontinued? 3. Prepare a properly formatted segmented income statement that would be more useful to management in assessing the long-run profitability of the various product lines. Complete this question by entering your answers in the tabs below. Required 1 Required 2 Required 3 Should the production and sale of racing bikes be discontinued? Yes ONO expenses for the past quarter follow: Dirt Mountain Racing Total Bikes Bikes Bikes $ 921,000 $268,000 $ 402,000 $ 251,000 474,000 115,000 205,000 154,000 447,000 153,000 197,000 97,000 Sales Variable manufacturing and selling expenses Contribution margin Fixed expenses: Advertising, traceable Depreciation of special equipment Salaries of product-line managers Allocated common fixed expenses Total fixed expenses Net operating income (loss) 69,600 8,400 40,900 20,300 43,500 20, 200 7,500 15,800 115,600 40,400 38,900 36,300 184,200 53,600 80,400 50,200 412,900 122,600 167,700 122,600 $ 34,100 $ 30,400 $ 29,300 $(25,600) *Allocated on the basis of sales dollars. Management is concerned about the continued losses shown by the racing bikes and wants a recommendation as to whether or not the line should be discontinued. The special equipment used to produce racing bikes has no resale value and does not wear out. Required: 1. What is the financial advantage (disadvantage) per quarter of discontinuing the racing bikes? 2. Should the production and sale of racing bikes be discontinued? 3. Prepare a properly formatted segmented income statement that would be more useful to management in assessing the long-run profitability of the various product lines. Complete this question by entering your answers in the tabs below. Required 1 1 Required 2 Required 3 Prepare a properly formatted segmented income statement that would be more useful to management in assessing the long- run profitability of the various product lines. Totals Dirt Bikes Mountain Bikes Racing Bikes 0 0 0 0 Sales Variable manufacturing and selling expenses Contribution margin (loss) Traceable fixed expenses: : Advertising Depreciation of special equipment Salaries of the product line managers Total traceable fixed expenses Product line segment margin (loss) 0 0 0 0 0 0 $ o $ 0 $ 0 Net operating income (loss) $ 0 Troy Engines, Ltd., manufactures a variety of engines for use in heavy equipment. The company has always produced all of the necessary parts for its engines, including all of the carburetors. An outside supplier has offered to sell one type of carburetor to Troy Engines, Ltd., for a cost of $34 per unit. To evaluate this offer, Troy Engines, Ltd., has gathered the following information relating to its own cost of producing the carburetor internally: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead, traceable Fixed manufacturing overhead, allocated Total cost 21,000 Per Units Unit per Year $ 14 $ 294,000 12 252,000 2 42,000 9* 189,000 12 252,000 $ 49 $1,029,000 *One-third supervisory salaries; two-thirds depreciation of special equipment (no resale value). Required: 1. Assuming the company has no alternative use for the facilities that are now being used to produce the carburetors, what would be the financial advantage (disadvantage) of buying 21,000 carburetors from the outside supplier? 2. Should the outside supplier's offer be accepted? 3. Suppose that if the carburetors were purchased, Troy Engines, Ltd., could use the freed capacity to launch a new product. The segment margin of the new product would be $210,000 per year. Given this new assumption, what would be the financial advantage (disadvantage) of buying 21,000 carburetors from the outside supplier? 4. Given the new assumption in requirement 3, should the outside supplier's offer be accepted? Complete this question by entering your answers in the tabs below. Required 1 Required 2 Required 3 Required 4 Suppose that if the carburetors were purchased, Troy Engines, Ltd., could use the freed capacity to launch a new product. The segment margin of the new product would be $210,000 per year. Given this new assumption, what would be the financial advantage (disadvantage) of buying 21,000 carburetors from the outside supplier? Troy Engines, Ltd., manufactures a variety of engines for use in heavy equipment. The company has always produced all of the necessary parts for its engines, including all of the carburetors. An outside supplier has offered to sell one type of carburetor to Troy Engines, Ltd., for a cost of $34 per unit. To evaluate this offer, Troy Engines, Ltd., has gathered the following information relating to its own cost of producing the carburetor internally: Units 21,000 Per Unit per Year $ 14 $ 294,000 12 252,000 2 9 189,000 12 252,000 $ 49 $1,029,000 Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead, traceable Fixed manufacturing overhead, allocated Total cost 42,000 *One-third supervisory salaries; two-thirds depreciation of special equipment (no resale value). Required: 1. Assuming the company has no alternative use for the facilities that are now being used to produce the carburetors, what would be the financial advantage (disadvantage) of buying 21,000 carburetors from the outside supplier? 2. Should the outside supplier's offer be accepted? 3. Suppose that if the carburetors were purchased, Troy Engines, Ltd., could use the freed capacity to launch a new product. The segment margin of the new product would be $210,000 per year. Given this new assumption, what would be the financial advantage (disadvantage) of buying 21,000 carburetors from the outside supplier? 4. Given the new assumption in requirement 3, should the outside supplier's offer be accepted? Complete this question by entering your answers in the tabs below. Required 1 Required 2 Required 3 Required 4 Given the new assumption in requirement 3, should the outside supplier's offer be accepted? Yes ONO Imperial Jewelers manufactures and sells a gold bracelet for $403.00. The company's accounting system says that the unit product cost for this bracelet is $269.00 as shown below: Direct materials Direct labor Manufacturing overhead Unit product cost $143 90 36 $269 The members of a wedding party have approached Imperial Jewelers about buying 14 of these gold bracelets for the discounted price of $363.00 each. The members of the wedding party would like special filigree applied to the bracelets that would require Imperial Jewelers to buy a special tool for $459 and that would increase the direct materials cost per bracelet by $11. The special tool would have no other use once the special order is completed. To analyze this special order opportunity, Imperial Jewelers has determined that most of its manufacturing overhead is fixed and unaffected by variations in how much jewelry is produced in any given period. However, $12.00 of the overhead is variable with respect to the number of bracelets produced. The company also believes that accepting this order would have no effect on its ability to produce and sell jewelry to other customers. Furthermore, the company could fulfill the wedding party's order using its existing manufacturing capacity. Required: 1. What is the financial advantage (disadvantage) of accepting the special order from the wedding party? 2. Should the company accept the special order? Complete this question by entering your answers in the tabs below. Required 1 Required 2 Should the company accept the special order? Yes ONO Exercise 11-9 Special Order Decision (LO11-4] Delta Company produces a single product. The cost of producing and selling a single unit of this product at the company's normal activity level of 102,000 units per year is: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Variable selling and administrative expenses Fixed selling and administrative expenses $ 2.40 $ 4.00 $ 0.80 $ 3.55 $ 1.90 $ 3.00 The normal selling price is $25.00 per unit. The company's capacity is 117,600 units per year. An order has been received from a mail- order house for 1,300 units at a special price of $22.00 per unit. This order would not affect regular sales or the company's total fixed costs Required: 1. What is the financial advantage (disadvantage) of accepting the special order? 2. As a separate matter from the special order, assume the company's inventory includes 1,000 units of this product that were produced last year and that are inferior to the current model. The units must be sold through regular channels at reduced prices. The company does not expect the selling of these inferior units to have any effect on the sales of its current model. What unit cost is relevant for establishing a minimum selling price for these units? Complete this question by entering your answers in the tabs below. Required 1 Required 2 What is the financial advantage (disadvantage) of accepting the special order? Delta Company produces a single product. The cost of producing and selling a single unit of this product at the company's normal activity level of 102,000 units per year is: Direct materials Direct labor Variable manufacturing overhead Fixed manufacturing overhead Variable selling and administrative expenses Fixed selling and administrative expenses $ 2.40 $ 4.00 $ 0.80 $ 3.55 $ 1.90 $ 3.00 The normal selling price is $25.00 per unit. The company's capacity is 117,600 units per year. An order has been received from a mail- order house for 1,300 units at a special price of $22.00 per unit. This order would not affect regular sales or the company's total fixed costs. Required: 1. What is the financial advantage (disadvantage) of accepting the special order? 2. As a separate matter from the special order, assume the company's inventory includes 1,000 units of this product that were produced last year and that are inferior to the current model. The units must be sold through regular channels at reduced prices. The company does not expect the selling of these inferior units to have any effect on the sales of its current model. What unit cost is relevant for establishing a minimum selling price for these units? Complete this question by entering your answers in the tabs below. Required 1 Required 2 As a separate matter from the special order, assume the company's inventory includes 1,000 units of this product that were produced last year and that are inferior to the current model. The units must be sold through regular channels at reduced prices. The company does not expect the selling of these inferior units to have any effect on the sales of its current model. What unit cost is relevant for establishing a minimum selling price for these units? (Round your answer to 2 decimal places.) Show less Relevant cost per unit