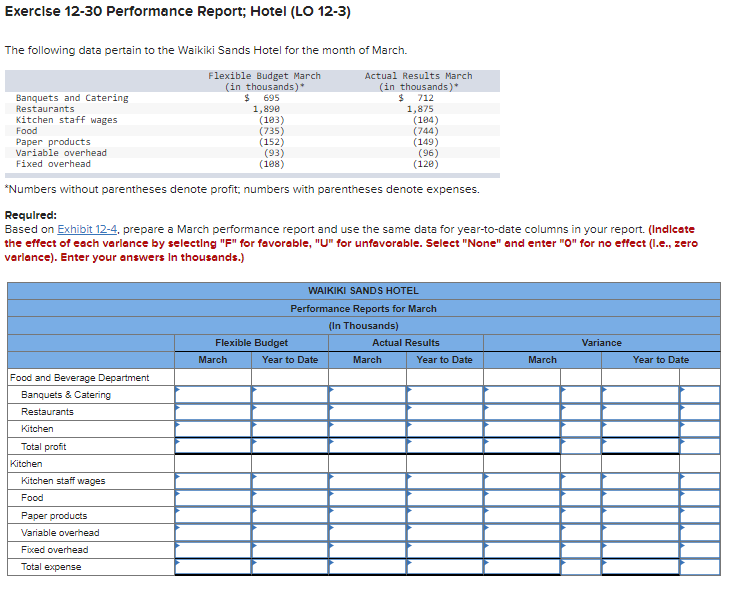

Exercise 12-30 Performance Report; Hotel (LO 12-3) The following data pertain to the Waikiki Sands Hotel for the month of March. Flexible Budget March Actual

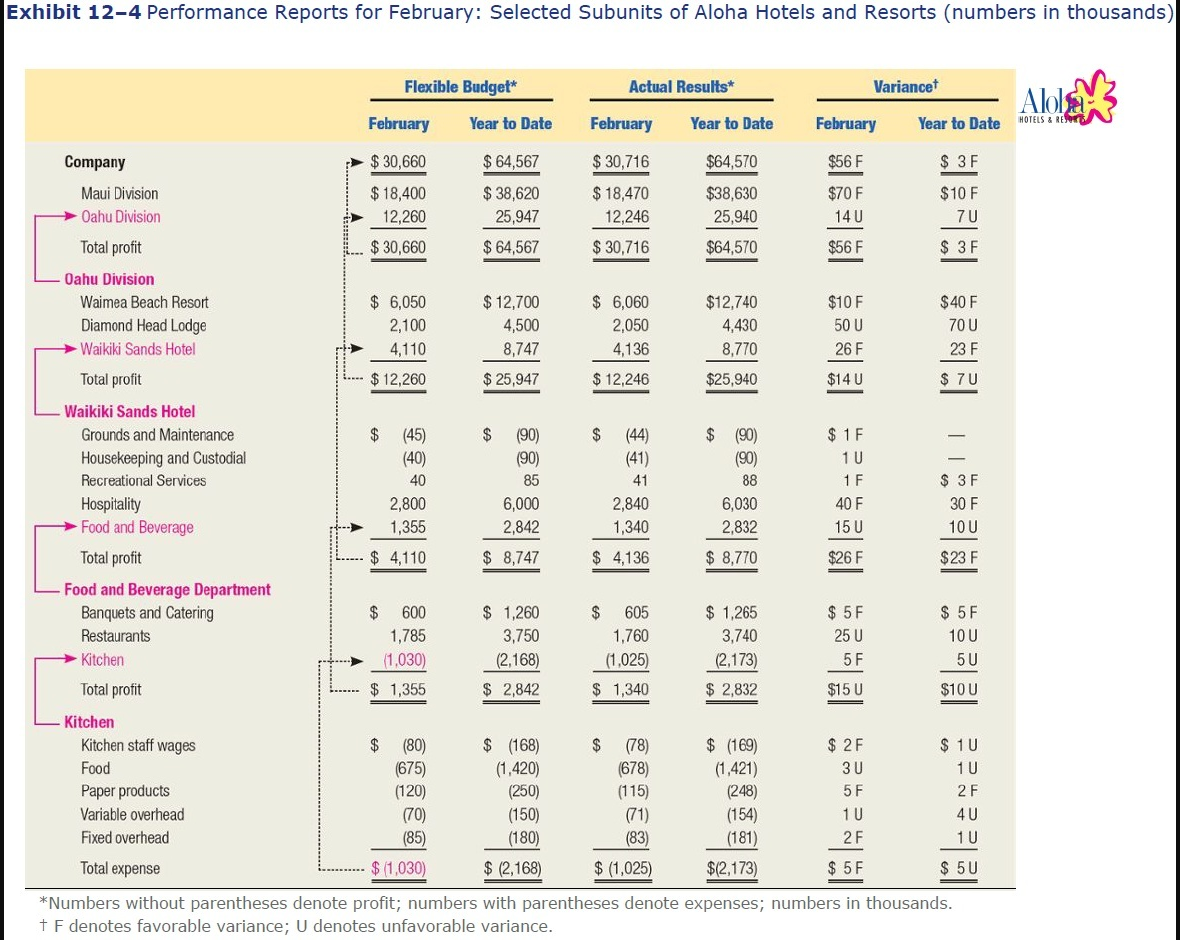

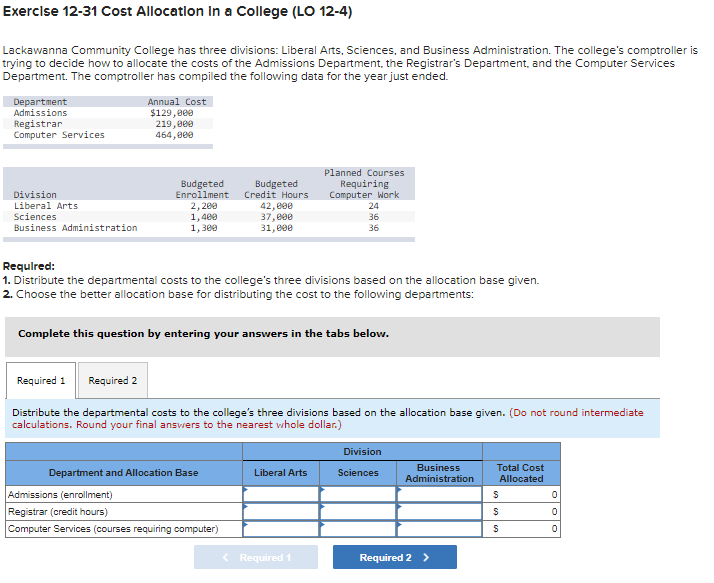

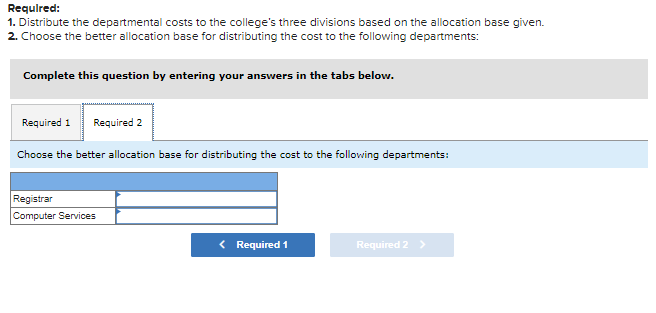

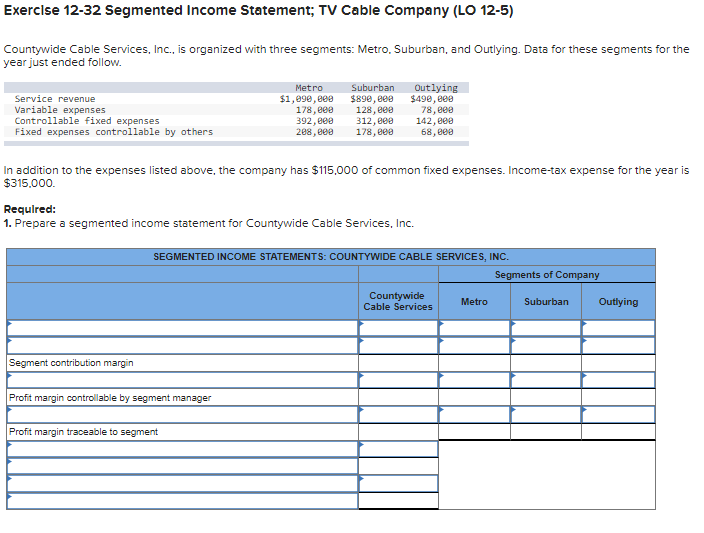

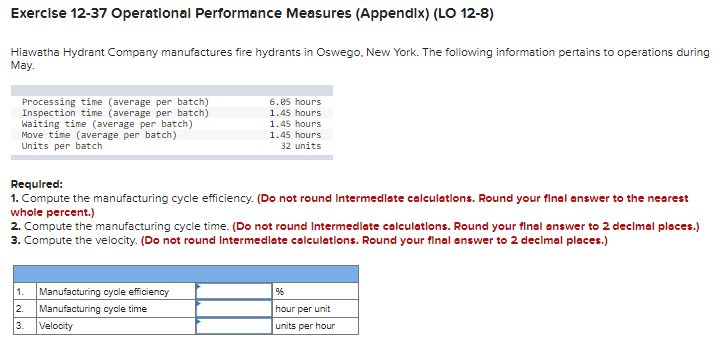

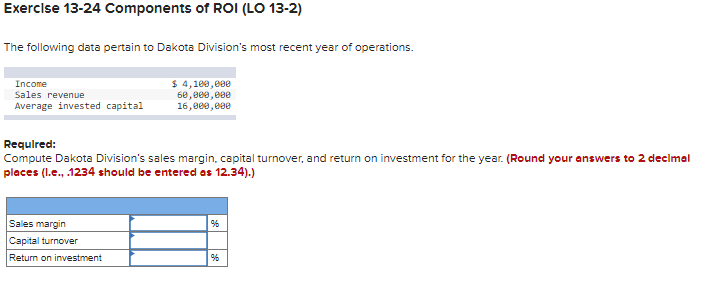

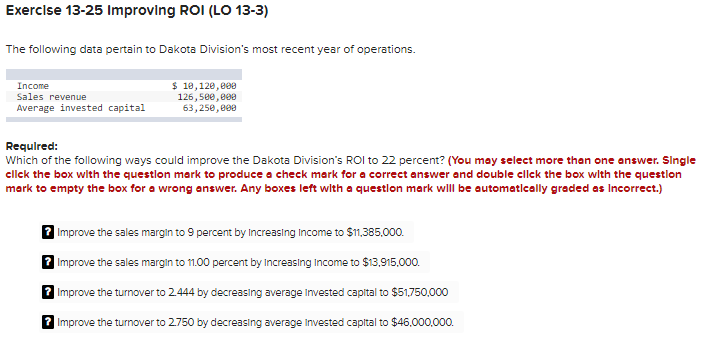

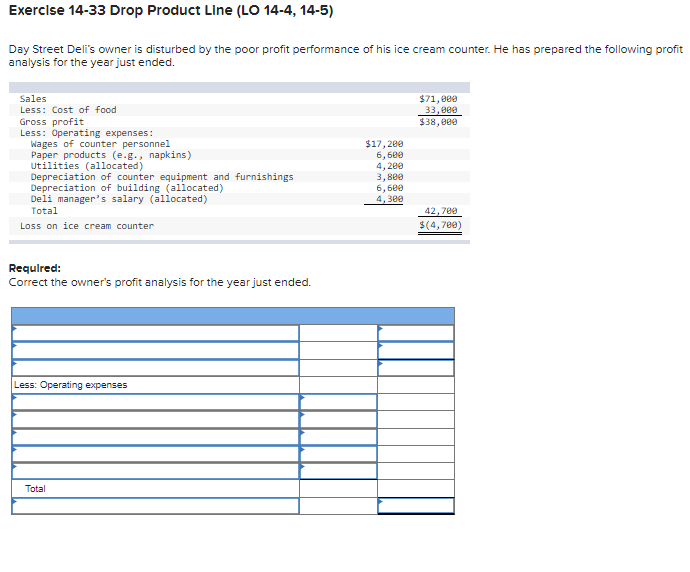

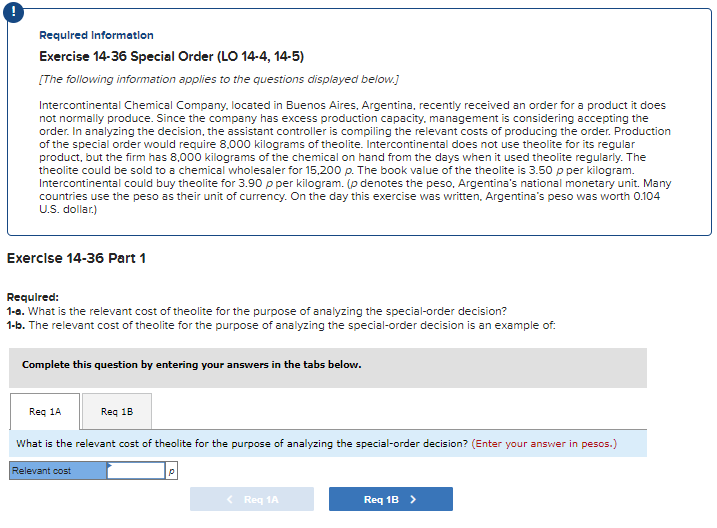

Exercise 12-30 Performance Report; Hotel (LO 12-3) The following data pertain to the Waikiki Sands Hotel for the month of March. Flexible Budget March Actual Results March (in thousands)* (in thousands)* Banquets and Catering $ 695 $ 712 Restaurants 1, 898 1, 875 Kitchen staff wages (103) (184) Food (735) (744) Paper products (152) (149) Variable overhead (93) (96) Fixed overhead (108) (128 ) "Numbers without parentheses denote profit: numbers with parentheses denote expenses. Required: Based on Exhibit 12-4, prepare a March performance report and use the same data for year-to-date columns in your report. (Indicate the effect of each variance by selecting "F" for favorable, "U" for unfavorable. Select "None" and enter "O" for no effect (L.e., zero variance). Enter your answers In thousands.) WAIKIKI SANDS HOTEL Performance Reports for March (In Thousands) Flexible Budget Actual Results Variance March Year to Date March Year to Date March Year to Date Food and Beverage Department Banquets & Catering Restaurants Kitchen Total profit Kitchen Kitchen staff wages Food Paper products Variable overhead Fixed overhead Total expenseExhibit 12-4 Performance Reports for February: Selected Subunits of Aloha Hotels and Resorts (numbers in thousands) Flexible Budget* Actual Results* Variancet Aloly February Year to Date February Year to Date February Year to Date HOTELS & REAL Company $ 30,660 $ 64,567 $ 30,716 $64,570 $56 F $ 3 F Maui Division $ 18,400 $ 38,620 $ 18,470 $38,630 $70 F $10 F Oahu Division 12,260 25,947 12,246 25,940 14 0 70 Total profit $ 30,660 $ 64,567 $ 30,716 $64,570 $56 F $ 3 F Oahu Division Waimea Beach Resort $ 6,050 $ 12,700 $ 6,060 $12,740 $10 F $40 F Diamond Head Lodge 2,100 4,500 2,050 4,430 50 U 70 U Waikiki Sands Hotel 4,110 8,747 4,136 8,770 26 F 23 F Total profit $ 12,260 $ 25,947 $ 12,246 $25,940 $14 U $ 7U Waikiki Sands Hotel Grounds and Maintenance (45 $ (90) $ (44) S (90) $ 1F Housekeeping and Custodial (40 (90) (41) (90) 1U Recreational Services 40 85 41 88 1 F $ 3F Hospitality 2,800 6,000 2,840 6,030 40 F 30 F Food and Beverage 1.355 2,842 1,340 2,832 15 U 10 U Total profit $ 4,110 $ 8,747 $ 4,136 $ 8,770 $26 F $23 F Food and Beverage Department Banquets and Catering 600 $ 1,260 $ 605 $ 1,265 $ 5F $ 5 F Restaurants 1,785 3,750 1,760 3,740 25 U 10U Kitchen (1,030) (2,168) (1,025) (2,173) 5 F 50 Total profit $ 1,355 $ 2,842 $ 1,340 $ 2,832 $15 U $10 U Kitchen Kitchen staff wages $ (80 $ (168) $ (78) $ (169) $ 2 F $ 10 Food (675) (1,420) 678 (1,421) 3U 10 Paper products (120) (250) (115) 248) 5 F 2 F Variable overhead (70) (150) (71) 154) 1U 4U Fixed overhead 85) 180) (83) (181) 2 F 10 Total expense $ 1,030 $ (2,168) $ (1,025 $(2,173) $ 5 F $ 5U *Numbers without parentheses denote profit; numbers with parentheses denote expenses; numbers in thousands. + F denotes favorable variance; U denotes unfavorable variance.Exercise 12-31 Cost Allocation In a College (LO 12-4) Lackawanna Community College has three divisions: Liberal Arts, Sciences, and Business Administration. The college's comptroller is trying to decide how to allocate the costs of the Admissions Department, the Registrar's Department, and the Computer Services Department. The comptroller has compiled the following data for the year just ended. Department Annual Cost Admissions $129, Bee Registrar 219, 080 Computer Services 464, 090 Planned Courses Budgeted Budgeted Requiring Division Enrollment Credit Hours Computer Work Liberal Arts 2, 289 42, 808 24 Sciences 1, 480 36 Business Administration 1, 380 31, 209 36 Required: 1. Distribute the departmental costs to the college's three divisions based on the allocation base given. 2. Choose the better allocation base for distributing the cost to the following departments: Complete this question by entering your answers in the tabs below. Required 1 Required 2 Distribute the departmental costs to the college's three divisions based on the allocation base given. (Do not round intermediate calculations. Round your final answers to the nearest whole dollar.) Division Department and Allocation Base Liberal Arts Sciences Business Total Cost Administration Allocated Admissions (enrollment) 0 Registrar (credit hours Computer Services (courses requiring computer) Required: 1. Distribute the departmental costs to the college's three divisions based on the allocation base given. 2. Choose the better allocation base for distributing the cost to the following departments: Complete this question by entering your answers in the tabs below. Required 1 Required 2 Choose the better allocation base for distributing the cost to the following departments: Registrar Computer Services Exercise 12-32 Segmented Income Statement; TV Cable Company (LO 12-5) Countywide Cable Services, Inc., is organized with three segments: Metro. Suburban, and Outlying. Data for these segments for the year just ended follow. Metro Suburban Outlying Service revenue $1,090, 808 $890, Be0 $490, 808 Variable expenses 178, 808 128, 808 78, 809 Controllable fixed expenses 392, 080 312, 890 142, 890 Fixed expenses controllable by others 208, 860 178, 808 68, 808 In addition to the expenses listed above, the company has $115,000 of common fixed expenses. Income-tax expense for the year is $315.000. Required: 1. Prepare a segmented income statement for Countywide Cable Services, Inc. SEGMENTED INCOME STATEMENTS: COUNTYWIDE CABLE SERVICES, INC Segments of Company Countywide Cable Services Metro Suburban Outlying Segment contribution margin Profit margin controllable by segment manager Profit margin traceable to segmentExercise 12-37 Operational Performance Measures (Appendix) (LO 12-8) Hiawatha Hydrant Company manufactures fire hydrants in Oswego. New York. The following information pertains to operations during May. Processing time (average per batch) 6.85 hours Inspection time (average per batch) 1. 45 hours Waiting time (average per batch) 1. 45 hours Move time (average per batch) 1. 45 hours Units per batch 32 units Required: 1. Compute the manufacturing cycle efficiency. (Do not round Intermediate calculations. Round your final answer to the nearest whole percent.) 2. Compute the manufacturing cycle time. (Do not round Intermediate calculations. Round your final answer to 2 decimal places.) 3. Compute the velocity. (Do not round Intermedlate calculations. Round your final answer to 2 decimal places.) 1. Manufacturing cycle efficiency 2. Manufacturing cycle time hour per unit 3. Velocity units per hourExercise 13-24 Components of ROI (LO 13-2) The following data pertain to Dakota Division's most recent year of operations. Income $ 4, 180, 808 Sales revenue 60, 080,898 Average invested capital 16,080,898 Required: Compute Dakota Division's sales margin, capital turnover, and return on investment for the year. (Round your answers to 2 decimal places (L.e., .1234 should be entered as 12.34).) Sales margin Capital turnover Return on investmentExercise 13-25 Improving ROI (LO 13-3) The following data pertain to Dakota Division's most recent year of operations. Income $ 10, 120, 209 Sales revenue 126,509, 909 Average invested capital 63, 250,809 Required: Which of the following ways could improve the Dakota Division's ROI to 22 percent? (You may select more than one answer. Single click the box with the question mark to produce a check mark for a correct answer and double click the box with the question mark to empty the box for a wrong answer. Any boxes left with a question mark will be automatically graded as Incorrect.) 7 Improve the sales margin to 9 percent by Increasing Income to $11,385,000. ? Improve the sales margin to 11.00 percent by Increasing Income to $13,915,000. ? Improve the turnover to 2.444 by decreasing average Invested capital to $51,750,000 7 Improve the turnover to 2.750 by decreasing average Invested capital to $46,000,000.Exercise 13-26 Residual Income (LO 13-2) The following data pertain to Dakota Division's most recent year of operations. Income $ 16,809, 980 Sales revenue 185,808, 080 Average invested capital 62,890, 080 Assume that the company's minimum desired rate of return on invested capital is 14 percent. Required: Compute Dakota Division's residual income for the year. Residual incomeRequired Information Exercise 13-29 ROI; Residual Income (LO 13-1, 13-2) [The following information applies to the questions displayed below.] Wyalusing Industries has manufactured prefabricated houses for over 20 years. The houses are constructed in sections to be assembled on customers' lots. Wyalusing expanded into the precut housing market when it acquired Fairmont Company. one of its suppliers. In this market, various types of lumber are precut into the appropriate lengths, banded into packages, and shipped to customers' lots for assembly. Wyalusing designated the Fairmont Division as an investment center. Wyalusing uses return on investment (ROI) as a performance measure with investment defined as average productive assets. Management bonuses are based in part on ROI. All investments are expected to earn a minimum return of 12 percent before income taxes. Fairmont's ROI has ranged from 24.8 to 28.0 percent since it was acquired. Fairmont had an investment opportunity in 20x1 that had an estimated ROI of 23 percent. Fairmont's management decided against the investment because it believed the investment would decrease the division's overall ROI. The 20x1 income statement for Fairmont Division follows. The division's productive assets were $33.600,000 at the end of 20x1, a 5 percent increase over the balance at the beginning of the year. FAIRMONT DIVISION Income Statement For the Year Ended December 31, 20x1 (in thousands ) Sales revenue $63, 480 Cost of goods sold 35, 180 Gross margin $28, 380 Operating expenses: Administrative $4,638 Selling 15, 470 20, 180 Income from operations before income taxes $ 8, 280 Exercise 13-29 Part 2 2. Would the management of Fairmont Division have been more likely to accept the investment opportunity it had in 20x1 if residual income were used as a performance measure instead of ROI? O Yes O NoExercise 14-33 Drop Product Line (LO 14-4, 14-5) Day Street Deli's owner is disturbed by the poor profit performance of his ice cream counter. He has prepared the following profit analysis for the year just ended. Sales $71, 080 Less: Cost of food 33,080 Gross profit $38, 080 Less: Operating expenses: Wages of counter personnel $17, 280 Paper products (e.g., napkins) 6, 680 Utilities (allocated) 4, 280 Depreciation of counter equipment and furnishings 3, 890 Depreciation of building (allocated) 6, 689 Deli manager's salary (allocated) 4,380 Total 42, 780 Loss on ice cream counter $(4,780) Required: Correct the owner's profit analysis for the year just ended. Less: Operating expenses TotalRequired Information Exercise 14-36 Special Order (LO 14-4, 14-5) [The following information applies to the questions displayed below.] Intercontinental Chemical Company, located in Buenos Aires, Argentina, recently received an order for a product it does not normally produce. Since the company has excess production capacity. management is considering accepting the order. In analyzing the decision, the assistant controller is compiling the relevant costs of producing the order. Production of the special order would require 8,000 kilograms of theolite. Intercontinental does not use theolite for its regular product, but the firm has 8,000 kilograms of the chemical on hand from the days when it used theolite regularly. The theolite could be sold to a chemical wholesaler for 15,200 p. The book value of the theolite is 3.50 p per kilogram. Intercontinental could buy theolite for 3.90 p per kilogram. (p denotes the peso, Argentina's national monetary unit. Many countries use the peso as their unit of currency. On the day this exercise was written. Argentina's peso was worth 0.104 U.S. dollar.) Exercise 14-36 Part 1 Required: 1-a. What is the relevant cost of theolite for the purpose of analyzing the special-order decision? 1-b. The relevant cost of theolite for the purpose of analyzing the special-order decision is an example of: Complete this question by entering your answers in the tabs below. Req 1A Req 18 What is the relevant cost of theolite for the purpose of analyzing the special-order decision? (Enter your answer in pesos.) Relevant cost p Complete this question by entering your answers in the tabs below. Req 1A Req 1B The relevant cost of theolite for the purpose of analyzing the special-order decision is an example of: The relevant cost of theolite for the purpose of analyzing the special-order decision is an example of: ! Required Information Exercise 14-36 Special Order (LO 14-4, 14-5) [The following information applies to the questions displayed below.] Intercontinental Chemical Company. located in Buenos Aires, Argentina, recently received an order for a product it does not normally produce. Since the company has excess production capacity, management is considering accepting the order. In analyzing the decision, the assistant controller is compiling the relevant costs of producing the order. Production of the special order would require 8,000 kilograms of theolite. Intercontinental does not use theolite for its regular product, but the firm has 8,000 kilograms of the chemical on hand from the days when it used theolite regularly. The theolite could be sold to a chemical wholesaler for 15,200 p. The book value of the theolite is 3.50 p per kilogram. Intercontinental could buy theolite for 3.90 p per kilogram. (p denotes the peso, Argentina's national monetary unit. Many countries use the peso as their unit of currency. On the day this exercise was written, Argentina's peso was worth 0.104 U.S. dollar.) Exercise 14-36 Part 2 2. Identify the relevance of each of the numbers given in the exercise in making the decision. Sales value Book value (c) Current purchase costExercise 14-40 Joint Products; Relevant Costs; Cost-Volume-Profit Analysis (LO 14-4, 14-6) Zytel Corporation produces cleaning compounds and solutions for industrial and household use. While most of its products are processed independently, a few are related. Grit 337, a coarse cleaning powder with many industrial uses, costs $2.40 a pound to make and sells for $3.60 a pound. A small portion of the annual production of this product is retained for further processing in the Mixing Department, where it is combined with several other ingredients to form a paste, which is marketed as a silver polish selling for $4.90 per jar. This further processing requires 1/4 pound of Grit 337 per jar. Costs of other ingredients, labor, and variable overhead associated with this further processing amount to $2.30 per jar. Variable selling costs are $0.20 per jar. If the decision were made to cease production of the silver polish, $8,200 of Mixing Department fixed costs could be avoided. Zytel has limited production capacity for Grit 337, but unlimited demand for the cleaning powder. Required: Calculate the minimum number of jars of silver polish that would have to be sold to justify further processing of Grit 337. (Round your Intermedlate calculations to 2 decimal places and final answer to the nearest whole number.) Minimum number of jars

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance