Answered step by step

Verified Expert Solution

Question

1 Approved Answer

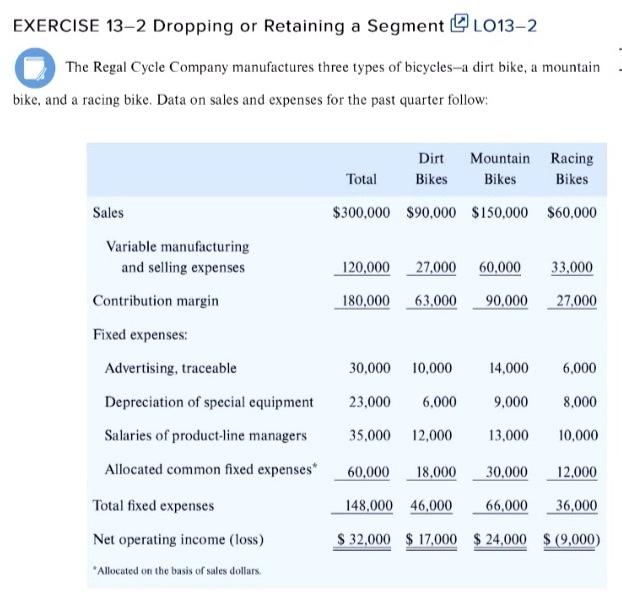

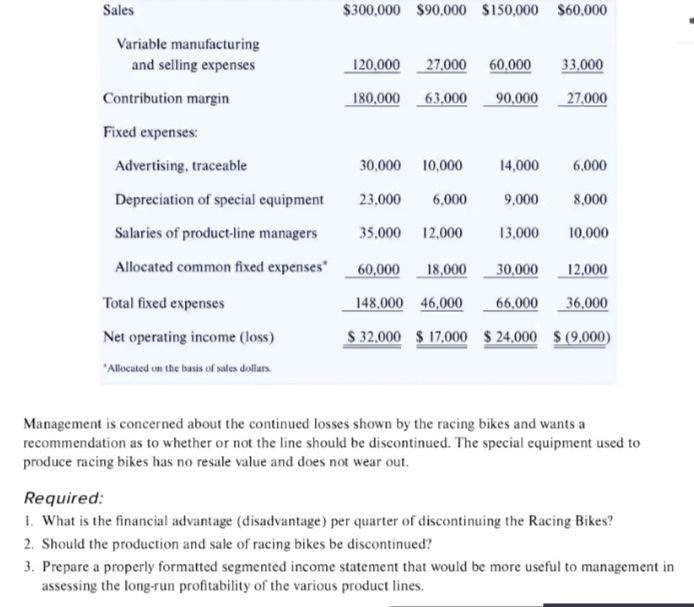

EXERCISE 13-2 Dropping or Retaining a Segment L013-2 The Regal Cycle Company manufactures three types of bicycles-a dirt bike, a mountain bike, and a racing

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Performance Audit Report Property Assessment Division Department Of Revenue

Authors: Montana Legislature Office Of The L

1st Edition

1019260211, 978-1019260210