Question

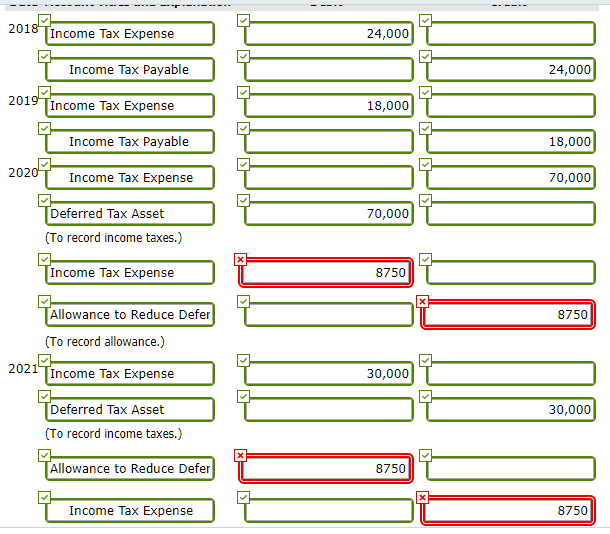

Exercise 19-24 Beilman Inc. reports the following pretax income (loss) for both book and tax purposes. Year Pretax Income (Loss) Tax Rate 2018 $120,000 20

| |||||||||||||||||||||||||||||||||||||||

| |||||||||

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Teams Audit

Authors: Kevin Barham

1st Edition

1907766030, 978-1907766039