Answered step by step

Verified Expert Solution

Question

1 Approved Answer

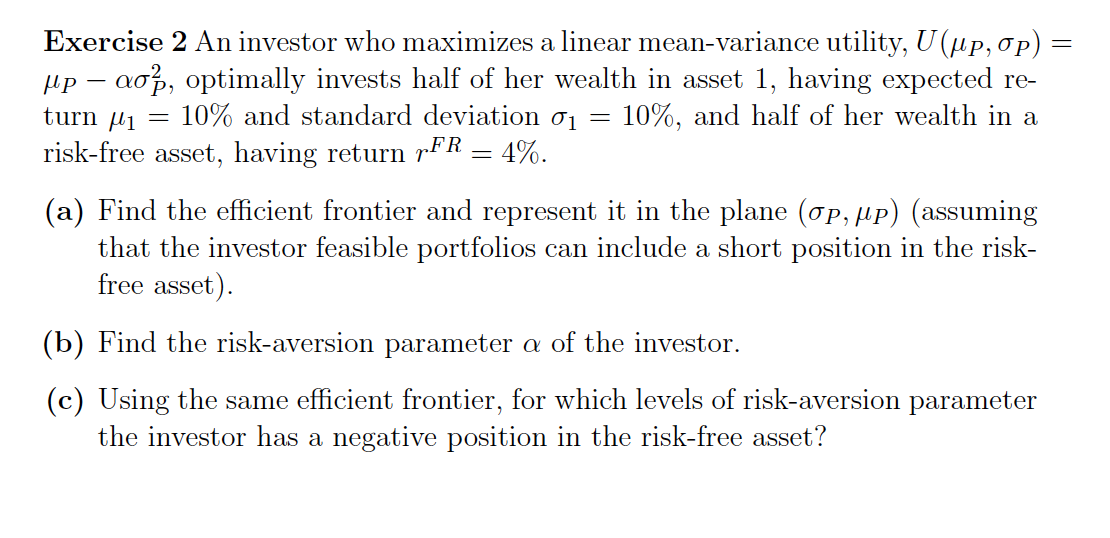

Exercise 2 An investor who maximizes a linear mean - variance utility, U ( P , P ) = P - P 2 , optimally

Exercise An investor who maximizes a linear meanvariance utility,

optimally invests half of her wealth in asset having expected re

turn and standard deviation and half of her wealth in a

riskfree asset, having return

a Find the efficient frontier and represent it in the plane assuming

that the investor feasible portfolios can include a short position in the risk

free asset

b Find the riskaversion parameter of the investor.

c Using the same efficient frontier, for which levels of riskaversion parameter

the investor has a negative position in the riskfree asset?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quantitative Financial Analytics The Path To Investment Profits

Authors: Edward E Williams, John A Dobelman

1st Edition

9813224258, 978-9813224254