Answered step by step

Verified Expert Solution

Question

1 Approved Answer

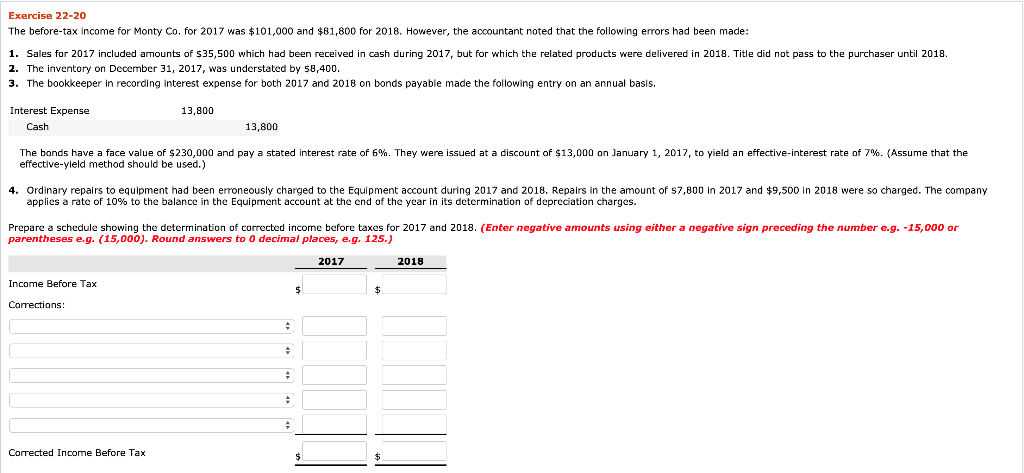

Exercise 22-20 The before-tax income for Monty Co. for 2017 was $101,000 and $81,800 for 2018. However, the accountant noted that the following errors had

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Evaluating The Effectiveness On Internal Audit Departments

Authors: Dereje Ferede Asrat, Sewale Abate Ayalew

1st Edition

3659298387, 978-3659298387