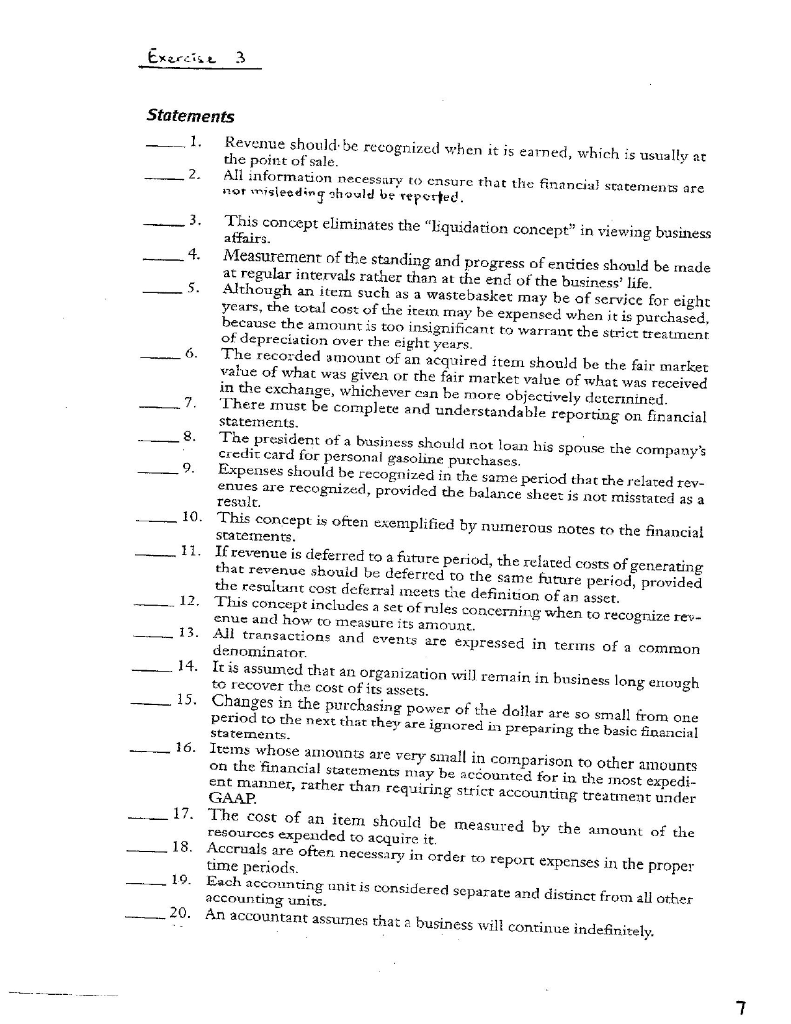

Exercise 3 3. 8. 9. Statements 1. Revenue should be recognized when it is earned, which is usually at the point of sale. 2. All information necessary to ensure that the financial statements are nor misleading should be reported. This concept eliminates the "Liquidation concept" in viewing business affairs. 4. Measurement of the standing and progress of entities should be made at regular intervals rather than at the end of the business life. 5. Although an item such as a wastebasket may be of service for eight years, the total cost of the item may be expensed when it is purchased. because the amount is too insignificant to warrant the strict treatment of depreciation over the eight years. 6. The recorded amount of an acquired item should be the fair market value of what was given or the fair market value of what was received in the exchange, whichever can be more objectively deterinined. 7. There must be complete and understandable reporting on financial statements. The president of a business should not loan his spouse the company's credit card for personal gasoline purchases. Expenses should be recognized in the same period that the related rev- enues are recognized, provided the balance sheet is not misstated as a result. 10. This concept is often exemplified by numerous notes to the financial 11. If revenue is deferred to a future period, the related costs of generating that revenue should be deferred to the same future period, provided the resultant cost deferral meets the definition of an asset. This concept includes a set of rules concerning when to recognize rev- enue and how to measure its amount. 13. All transactions and events are expressed in terms of a common denominator. 14. It is assumed that an organization will remain in business long enough to recover the cost of its assets. 15. Changes in the purchasing power of the dollar are so small from one period to the next that they are ignored in preparing the basic financial 16. Items whose amounts are very small in comparison to other amounts on the financial statements may be accounted for in the snost expedi- ent manner, rather than requiring strict accounting treatinent under 17. The cost of an item should be measured by the amount of the resources expended to acquire it. 18. Accruals are often necessary in order to report expenses in the proper time periods. 19. Each accounting unit is considered separate and distinct from all other accounting units. 20. An accountant assumes that a business will continue indefinitely. statements. 12 statements. GAAP 7 Exercise 3 3. 8. 9. Statements 1. Revenue should be recognized when it is earned, which is usually at the point of sale. 2. All information necessary to ensure that the financial statements are nor misleading should be reported. This concept eliminates the "Liquidation concept" in viewing business affairs. 4. Measurement of the standing and progress of entities should be made at regular intervals rather than at the end of the business life. 5. Although an item such as a wastebasket may be of service for eight years, the total cost of the item may be expensed when it is purchased. because the amount is too insignificant to warrant the strict treatment of depreciation over the eight years. 6. The recorded amount of an acquired item should be the fair market value of what was given or the fair market value of what was received in the exchange, whichever can be more objectively deterinined. 7. There must be complete and understandable reporting on financial statements. The president of a business should not loan his spouse the company's credit card for personal gasoline purchases. Expenses should be recognized in the same period that the related rev- enues are recognized, provided the balance sheet is not misstated as a result. 10. This concept is often exemplified by numerous notes to the financial 11. If revenue is deferred to a future period, the related costs of generating that revenue should be deferred to the same future period, provided the resultant cost deferral meets the definition of an asset. This concept includes a set of rules concerning when to recognize rev- enue and how to measure its amount. 13. All transactions and events are expressed in terms of a common denominator. 14. It is assumed that an organization will remain in business long enough to recover the cost of its assets. 15. Changes in the purchasing power of the dollar are so small from one period to the next that they are ignored in preparing the basic financial 16. Items whose amounts are very small in comparison to other amounts on the financial statements may be accounted for in the snost expedi- ent manner, rather than requiring strict accounting treatinent under 17. The cost of an item should be measured by the amount of the resources expended to acquire it. 18. Accruals are often necessary in order to report expenses in the proper time periods. 19. Each accounting unit is considered separate and distinct from all other accounting units. 20. An accountant assumes that a business will continue indefinitely. statements. 12 statements. GAAP 7