Answered step by step

Verified Expert Solution

Question

1 Approved Answer

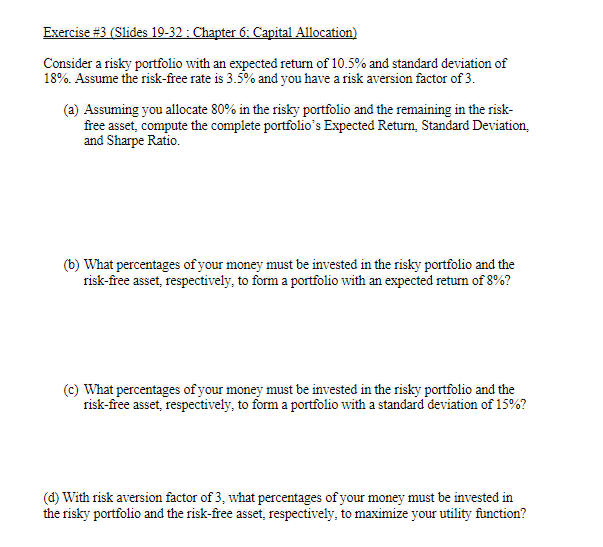

Exercise # 3 ( Slides 1 9 - 3 2 : Chapter 6 : Capital Allocation ) Consider a risky portfolio with an expected

Exercise #Slides : Chapter : Capital Allocation

Consider a risky portfolio with an expected return of and standard deviation of Assume the riskfree rate is and you have a risk aversion factor of

a Assuming you allocate in the risky portfolio and the remaining in the riskfree asset, compute the complete portfolio's Expected Return, Standard Deviation, and Sharpe Ratio.

b What percentages of your money must be invested in the risky portfolio and the riskfree asset, respectively, to form a portfolio with an expected return of

c What percentages of your money must be invested in the risky portfolio and the riskfree asset, respectively, to form a portfolio with a standard deviation of

d With risk aversion factor of what percentages of your money must be invested in the risky portfolio and the riskfree asset, respectively, to maximize your utility function?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Management

Authors: Eugene F. Brigham, Joel F. Houston

Concise 6th Edition

324664559, 978-0324664553