Answered step by step

Verified Expert Solution

Question

1 Approved Answer

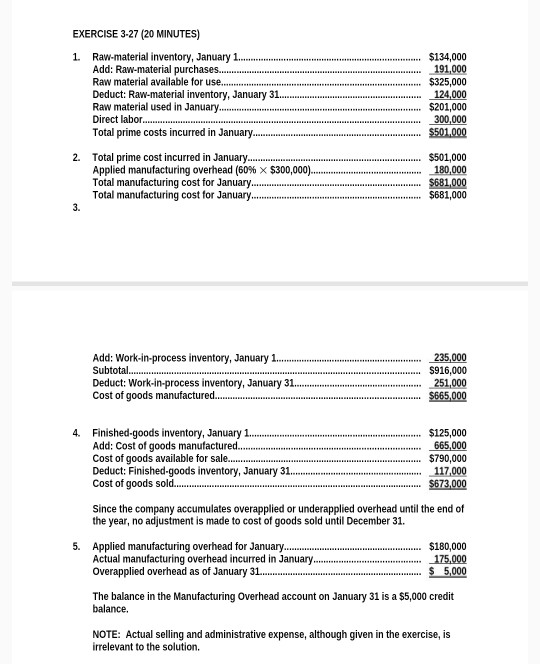

EXERCISE 3-27 (20 MINUTES) 1 Raw-material inventory, January 1. ............ Add: Raw-material purchases. Raw material available for use... Deduct: Raw-material inventory, January 31. Raw material

EXERCISE 3-27 (20 MINUTES) 1 Raw-material inventory, January 1. ............ Add: Raw-material purchases. Raw material available for use... Deduct: Raw-material inventory, January 31. Raw material used in January Direct labor.......... Total prime costs incurred in January... $134,000 191,000 $325,000 124,000 5201,000 300,000 $501.000 2. Total prime cost incurred in January Applied manufacturing overhead (60% X $300,000) Total manufacturing cost for January.... Total manufacturing cost for January... $501,000 180,000 $681,000 $681,000 Add: Work-in-process inventory, January 1........................ Subtotal.. Deduct: Work-in-process inventory, January 31....... Cost of goods manufactured. 235,000 S916,000 251,000 $665,000 4. Finished-goods inventory, January 1........ Add: Cost of goods manufactured.. Cost of goods available for sale.... Deduct: Finished-goods inventory, January 31.. Cost of goods sold...... $125,000 665,000 $790,000 117,000 $673.000 Since the company accumulates overapplied or underapplied overhead until the end of the year, no adjustment is made to cost of goods sold until December 31. 5. Applied manufacturing overhead for January Actual manufacturing overhead incurred in January....... Overapplied overhead as of January 31 ... $180,000 175.000 $ 5,000 The balance in the Manufacturing Overhead account on January 31 is a $5,000 credit balance. NOTE: Actual selling and administrative expense, although given in the exercise, is irrelevant to the solution. EXERCISE 3-27 (20 MINUTES) 1 Raw-material inventory, January 1. ............ Add: Raw-material purchases. Raw material available for use... Deduct: Raw-material inventory, January 31. Raw material used in January Direct labor.......... Total prime costs incurred in January... $134,000 191,000 $325,000 124,000 5201,000 300,000 $501.000 2. Total prime cost incurred in January Applied manufacturing overhead (60% X $300,000) Total manufacturing cost for January.... Total manufacturing cost for January... $501,000 180,000 $681,000 $681,000 Add: Work-in-process inventory, January 1........................ Subtotal.. Deduct: Work-in-process inventory, January 31....... Cost of goods manufactured. 235,000 S916,000 251,000 $665,000 4. Finished-goods inventory, January 1........ Add: Cost of goods manufactured.. Cost of goods available for sale.... Deduct: Finished-goods inventory, January 31.. Cost of goods sold...... $125,000 665,000 $790,000 117,000 $673.000 Since the company accumulates overapplied or underapplied overhead until the end of the year, no adjustment is made to cost of goods sold until December 31. 5. Applied manufacturing overhead for January Actual manufacturing overhead incurred in January....... Overapplied overhead as of January 31 ... $180,000 175.000 $ 5,000 The balance in the Manufacturing Overhead account on January 31 is a $5,000 credit balance. NOTE: Actual selling and administrative expense, although given in the exercise, is irrelevant to the solution

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: J. David Spiceland ,Wayne M. Thomas ,Don Herrmann

2nd Revised Edition

0071088385, 978-0071088381