Answered step by step

Verified Expert Solution

Question

1 Approved Answer

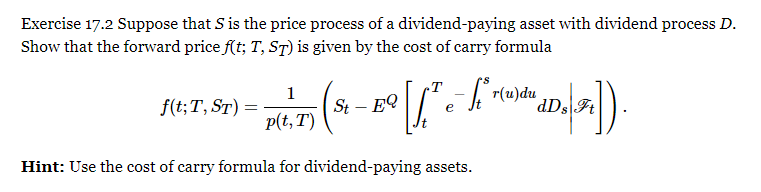

Exercises question from Arbitrage Theory in Continuous Time by Tomas Bjrk Exercise 17.2 Suppose that S is the price process of a dividend-paying asset with

Exercises question from Arbitrage Theory in Continuous Time by Tomas Bjrk

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Underground Credit Builders Handbook What You Need To Know To Build Personal And Business Credit Successfully

Authors: Fourth Dimension

1st Edition

0998060909, 978-0998060903