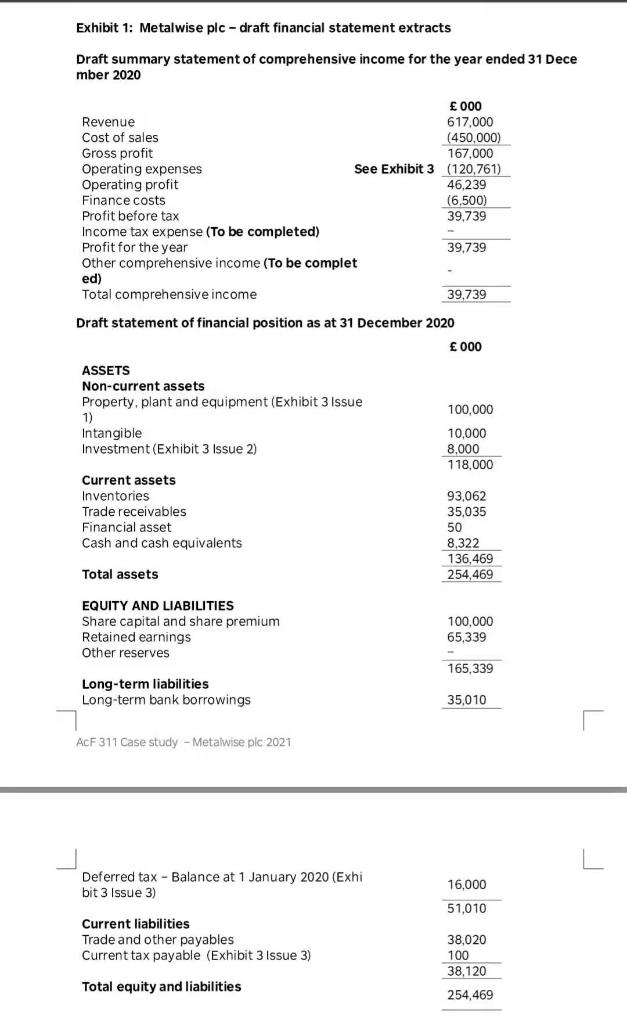

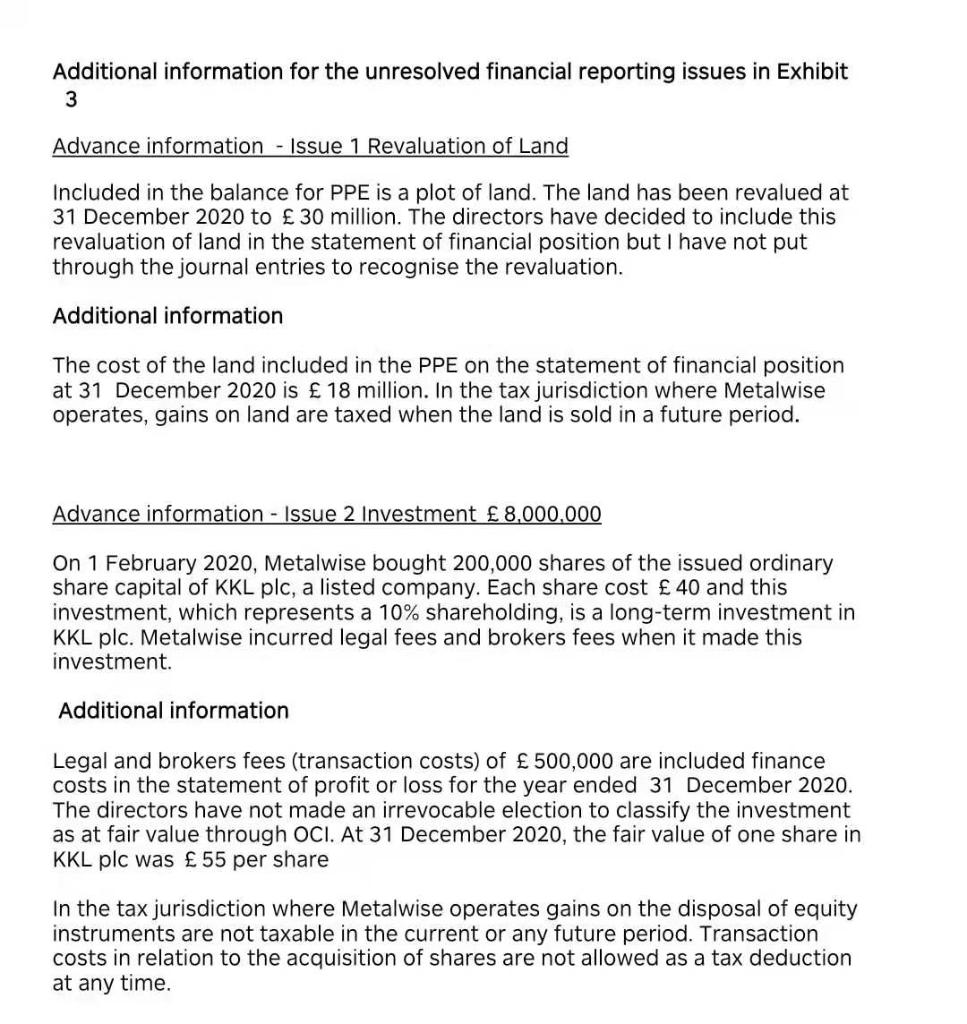

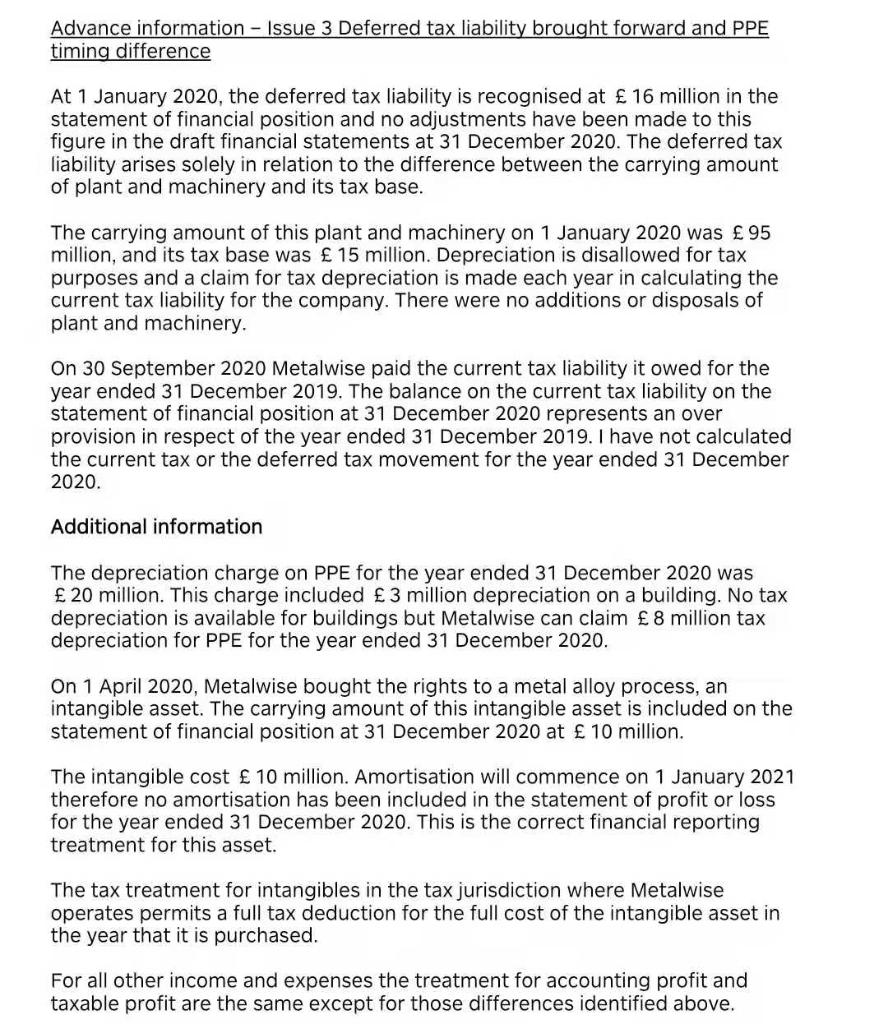

Exhibit 1: Metalwise plc-draft financial statement extracts Draft summary statement of comprehensive income for the year ended 31 Dece mber 2020 000 Revenue 617,000 Cost of sales (450,000) Gross profit 167,000 Operating expenses See Exhibit 3 (120,761) Operating profit 46.239 Finance costs (6,500) Profit before tax 39,739 Income tax expense (To be completed) Profit for the year 39,739 Other comprehensive income (To be complet ed) Total comprehensive income 39,739 Draft statement of financial position as at 31 December 2020 000 ASSETS Non-current assets Property, plant and equipment (Exhibit 3 Issue 1) Intangible Investment (Exhibit 3 Issue 2) 100,000 10,000 8,000 118,000 Current assets Inventories Trade receivables Financial asset Cash and cash equivalents 93,062 35,035 50 8,322 136,469 254,469 Total assets EQUITY AND LIABILITIES Share capital and share premium Retained earnings Other reserves 100,000 65,339 165,339 Long-term liabilities Long-term bank borrowings 35,010 ACF 311 Case study - Metalwise plc 2021 Deferred tax - Balance at 1 January 2020 (Exhi bit 3 Issue 3) 16,000 51,010 Current liabilities Trade and other payables Current tax payable (Exhibit 3 Issue 3) 38,020 100 38,120 Total equity and liabilities 254,469 Additional information for the unresolved financial reporting issues in Exhibit 3 Advance information - Issue 1 Revaluation of Land Included in the balance for PPE is a plot of land. The land has been revalued at 31 December 2020 to 30 million. The directors have decided to include this revaluation of land in the statement of financial position but I have not put through the journal entries to recognise the revaluation. Additional information The cost of the land included in the PPE on the statement of financial position at 31 December 2020 is 18 million. In the tax jurisdiction where Metalwise operates, gains on land are taxed when the land is sold in a future period. Advance information - Issue 2 Investment 8,000,000 On 1 February 2020, Metalwise bought 200,000 shares of the issued ordinary share capital of KKL plc, a listed company. Each share cost 40 and this investment, which represents a 10% shareholding, is a long-term investment in KKL plc. Metalwise incurred legal fees and brokers fees when it made this investment. Additional information Legal and brokers fees (transaction costs) of 500,000 are included finance costs in the statement of profit or loss for the year ended 31 December 2020. The directors have not made an irrevocable election to classify the investment as at fair value through OCI. At 31 December 2020, the fair value of one share in KKL plc was 55 per share In the tax jurisdiction where Metalwise operates gains on the disposal of equity instruments are not taxable in the current or any future period. Transaction costs in relation to the acquisition of shares are not allowed as a tax deduction at any time. Advance information - Issue 3 Deferred tax liability brought forward and PPE timing difference At 1 January 2020, the deferred tax liability is recognised at 16 million in the statement of financial position and no adjustments have been made to this figure in the draft financial statements at 31 December 2020. The deferred tax liability arises solely in relation to the difference between the carrying amount of plant and machinery and its tax base. The carrying amount of this plant and machinery on 1 January 2020 was 95 million, and its tax base was 15 million. Depreciation is disallowed for tax purposes and a claim for tax depreciation is made each year in calculating the current tax liability for the company. There were no additions or disposals of plant and machinery. On 30 September 2020 Metalwise paid the current tax liability it owed for the year ended 31 December 2019. The balance on the current tax liability on the statement of financial position at 31 December 2020 represents an over provision in respect of the year ended 31 December 2019. I have not calculated the current tax or the deferred tax movement for the year ended 31 December 2020. Additional information The depreciation charge on PPE for the year ended 31 December 2020 was 20 million. This charge included 3 million depreciation on a building. No tax depreciation is available for buildings but Metalwise can claim 8 million tax depreciation for PPE for the year ended 31 December 2020. On 1 April 2020, Metalwise bought the rights to a metal alloy process, an intangible asset. The carrying amount of this intangible asset is included on the statement of financial position at 31 December 2020 at 10 million. The intangible cost 10 million. Amortisation will commence on 1 January 2021 therefore no amortisation has been included in the statement of profit or loss for the year ended 31 December 2020. This is the correct financial reporting treatment for this asset. The tax treatment for intangibles in the tax jurisdiction where Metalwise operates permits a full tax deduction for the full cost of the intangible asset in the year that it is purchased. For all other income and expenses the treatment for accounting profit and taxable profit are the same except for those differences identified above. The tax rate is 20% Required: a) For Issue 1 Revaluation of land and Issue 2 Investment, . explain the appropriate financial reporting treatment making reference to relevant accounting standards; and set out the accounting adjustments required to correct the financial statements for Metalwise plc for the year ended 31 December 2020. Maximum words for part a) = 450 (10 marks) b) Including your recommended adjustments from part a) and the advance and additional information for Issue 3, calculate the current and deferred tax liabilities for Metalwise plc for the year ended 31 December 2020. Set out the journals to adjust the statement of comprehensive income and the statement of financial position. (20 marks) c) Prepare a revised statement of comprehensive income and statement of financial position for Metalwise plc for the year ended 31 December 2020 which reflects your adjustments for a) and b) above. You must show your workings. (20 marks)