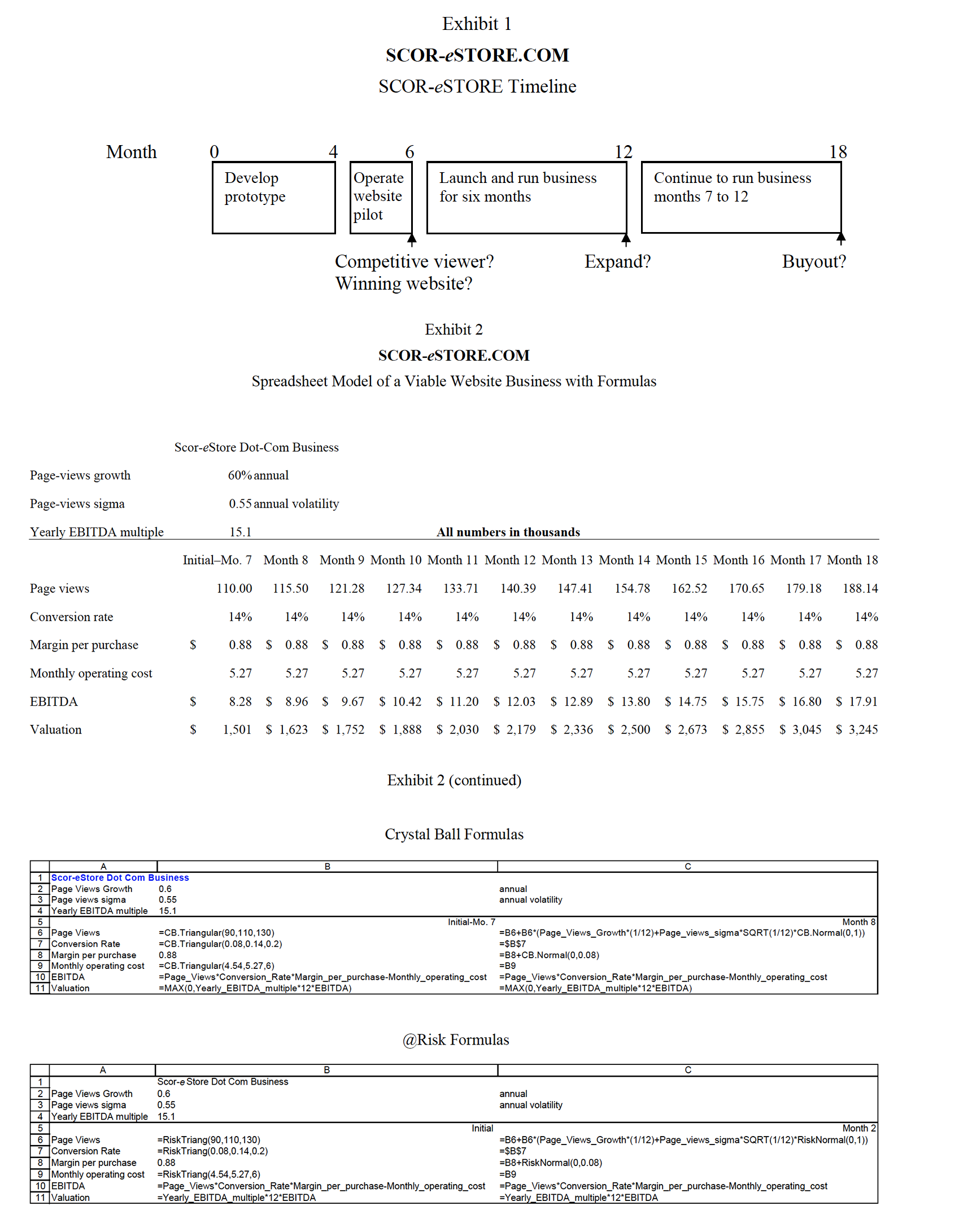

Exhibit 1 SCOR-eSTORE.COM SCOR-eSTORE Timeline Month 12 18 Develop Operate Launch and run business Continue to run business prototype website for six months months 7

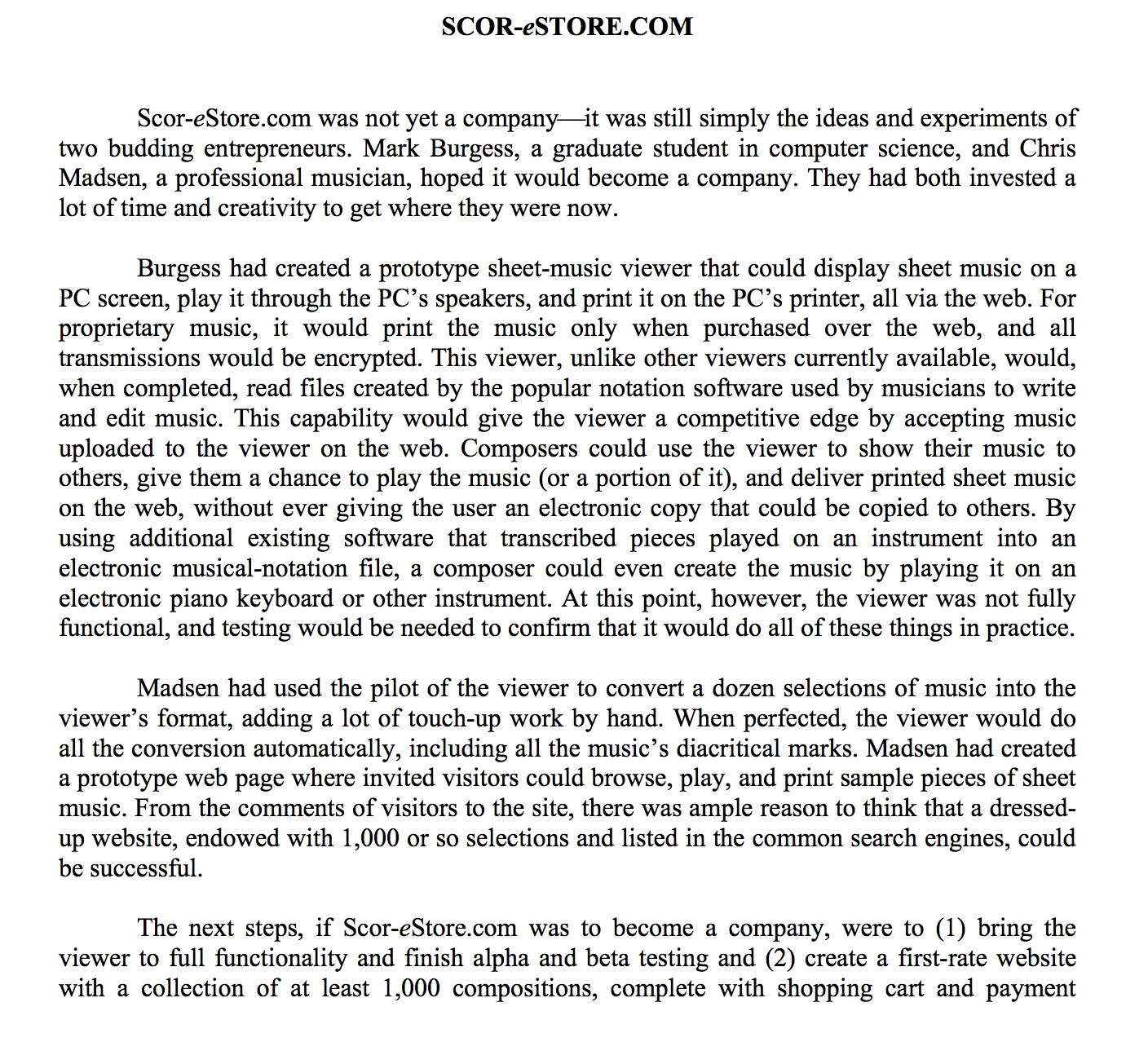

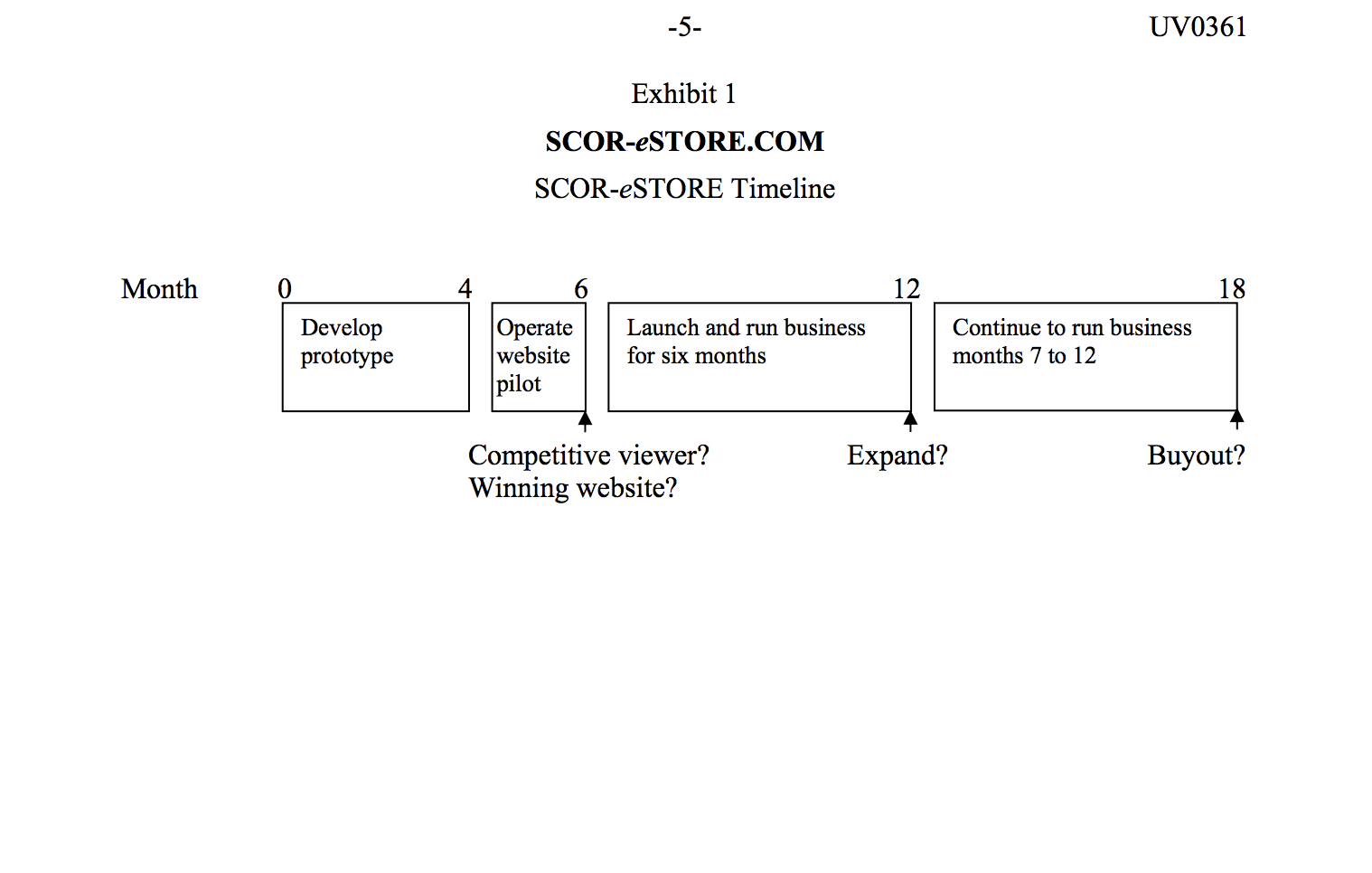

Exhibit 1 SCOR-eSTORE.COM SCOR-eSTORE Timeline Month 12 18 Develop Operate Launch and run business Continue to run business prototype website for six months months 7 to 12 pilot Competitive viewer? Expand? Buyout? Winning website? Exhibit 2 SCOR-eSTORE.COM Spreadsheet Model of a Viable Website Business with Formulas Scor-eStore Dot-Com Business Page-views growth 60% annua Page-views sigma 0.55 annual volatility Yearly EBITDA multiple 15.1 All numbers in thousands Initial-Mo. 7 Month 8 Month 9 Month 10 Month 11 Month 12 Month 13 Month 14 Month 15 Month 16 Month 17 Month 18 Page views 1 10.00 115.50 121.28 127.34 133.71 140.39 147.41 154.78 162.52 170.65 179.18 188.14 Conversion rate 14% 14% 14% 14% 14% 14% 14% 14% 14% 14% 14% 14% Margin per purchase 0.88 $ 0.88 $ 0.88 5 0.88 5 0.88 5 0.88 $ 0.88 $ 0.88 $ 0.88 5 0.88 5 0.88 $ 0.88 Monthly operating cost 5.27 5.27 5.27 5.27 5.27 5.27 5.27 5.27 5.27 5.27 5.27 5.27 EBITDA 8.28 $ 8.96 $ 9.67 $ 10.42 $ 11.20 $ 12.03 $ 12.89 $ 13.80 $ 14.75 $ 15.75 $ 16.80 $ 17.91 Valuation 1,501 $ 1,623 $ 1,752 $ 1,888 $ 2,030 $ 2,179 $ 2,336 $ 2,500 $ 2,673 $ 2,855 $ 3,045 $ 3,245 Exhibit 2 (continued) Crystal Ball Formulas 1 Scor-eStore Dot Com Business 2 Page Views Growth 0.6 annual 3 Page views sigma 0.55 annual volatility 4 Yearly EBITDA multiple 15.1 Initial-Mo. Month 8 6 Page Views =CB.Triangular(90, 1 10, 130) =B6+B6*(Page_Views_Growth*(1/12)+Page_views_sigma*SQRT(1/12)*CB.Normal(0,1)) 7 Conversion Rate =CB.Triangular(0.08,0.14,0.2) =$B$7 8 Margin per purchase 0.88 =B8+CB.Normal(0,0.08) 9 Monthly operating cost =CB.Triangular(4.54,5.27,6) =B9 10 EBITDA =Page_Views*Conversion_Rate*Margin_per_purchase-Monthly_operating_cost =Page_Views*Conversion_Rate*Margin_per_purchase-Monthly_operating_cost 11 Valuation =MAX(0, Yearly_EBITDA_multiple*12*EBITDA) =MAX(0, Yearly_EBITDA_multiple*12*EBITDA) @Risk Formulas Scor-e Store Dot Com Business 2 Page Views Growth 06 annual 3 Page views sigma 0.55 annual volatility 4 Yearly EBITDA multiple 15.1 5 Initial Month 2 6 Page Views =Risk Triang(90, 110, 130) =B6+86*(Page_Views_Growth*(1/12)+Page_views_sigma*SQRT(1/12)*RiskNormal(0,1)) 7 Conversion Rate =Risk Triang(0.08,0.14,0.2) =$B$7 8 Margin per purchase 0.88 =B8+RiskNormal(0,0.08) 9 Monthly operating cost =Risk Triang(4.54,5.27,6) =B9 10 EBITDA =Page_Views*Conversion_Rate*Margin_per_purchase-Monthly_operating_cost =Page_Views*Conversion_Rate*Margin_per_purchase-Monthly_operating_cost 11 Valuation =Yearly_EBITDA_multiple* 12*EBITDA =Yearly_EBITDA_multiple*12*EBITDASCOR-eSTORE.COM ScoreStore.com was not yet a companyit was still simply the ideas and experiments of two budding entrepreneurs. Mark Burgess, a graduate student in computer science, and Chris Madsen, a professional musician, hoped it would become a company. They had both invested a lot of time and creativity to get where they were now. Burgess had created a prototype sheet-music viewer that could display sheet music on a PC screen, play it through the PC's speakers, and print it on the PC's printer, all via the web. For proprietary music, it would print the music only when purchased over the web, and all transmissions would be encrypted. This viewer, unlike other viewers currently available, would, when completed, read les created by the popular notation software used by musicians to write and edit music. This capability would give the viewer a competitive edge by accepting music uploaded to the viewer on the web. Composers could use the viewer to show their music to others, give them a chance to play the music (or a portion of it), and deliver printed sheet music on the web, without ever giving the user an electronic copy that could be copied to others. By using additional existing software that transcribed pieces played on an instrument into an electronic musical-notation le, a composer could even create the music by playing it on an electronic piano keyboard or other instrument. At this point, however, the viewer was not fully functional, and testing would be needed to conrm that it would do all of these things in practice. Madsen had used the pilot of the viewer to convert a dozen selections of music into the viewer's format, adding a lot of touch-up work by hand. When perfected, the viewer would do all the conversion automatically, including all the music's diacritical marks. Madsen had created a prototype web page where invited visitors could browse, play, and print sample pieces of sheet music. From the comments of visitors to the site, there was ample reason to think that a dressed- up website, endowed with 1,000 or so selections and listed in the common search engines, could be successful. The next steps, if Scor-eStore.com was to become a company, were to (1) bring the viewer to full functionality and nish alpha and beta testing and (2) create a rst-rate website with a collection of at least 1,000 compositions, complete with shopping cart and payment capabilities. About $90,000 would be needed to pay the two principals subsistence wages and to lease computer equipment and use home ofces (for about four months) and then to operate the website for a couple of months. By the end of six months, they would know whether the business was viable. Burgess and Madsen had approached a variety of venture capitalists, iends, and friends of friends for funding, as they themselves were penniless. For various reasons, they had not managed to find a mutually acceptable deal with an investor, and they were down to their last prospect. Lance Bernard was considering a proposal whereby he would put up the entire $90,000 and take one-third ownership of Scor-eStore.com. Bernard had said to Burgess and Madsen that \"someone will make a lot of money with an online sheet-music business. It's the perfect way to deliver musicno stores, no sales clerks, no inventory; you don't even need to buy paper or do any printing and binding.\" In the privacy of his ofce, Bernard made some quick calculations, however, that led him to ow on the investment. Bernard believed that only about four sheet-music websites would survive to be worth anything, and that it would be apparent a couple of months after the website was ofcially opened (six months in the future) whether Scor-eStore.com would be among them. If it were not in the top group by then, in Bemard's mind, the business would not be worth pursuing further and it should just die. If the website were among the top four at that time, he would sell his share for what he thought would be about $500,000 and move on to something new.I Assessing a 15% chance2 that the website business would be viable, he multiplied 15% by $500,000, obtaining $75,000, discounted it for six months at his usual rate of 20%, and concluded that his share of the business should be valued at no more than $68,465, which is $75,000 + 1.25. This amount was less than the $90,000 investment, so Bernard planned to pass on the opportunity. He threw the le in his bag and headed for a casual dinner with some of his venture-capital buddies. At dinner that evening, Bernard mentioned the online music opportunity and lamented, \"If an idea this good doesn't cut it, why do people invest in Internet start-ups?\" Questions about the underlying business model prompted Bernard to describe how the business would work. He told them that two things were required: a competitively mctional viewer and a winning website with attractive content. After four months he would know about the viewer, and in months 5 and 6 he could test the website. If this viewer were not functional after four months, his test of the website could still be performed by licensing an existing, more limited viewer and hand-editing the pieces for the music collection in the test. Then the others entered the conversation: Allen: Suppose the viewer is competitively functional and yet, after six months, the website is not a winner. Could vou abandon the web business and sell the technologv. mavbe Bernard: Soares: Bernard: Estes: Bernard: Bouchek: Well, I believe that I could, and this would create some additional value to reward the development effort. In fact, the principals told me that, for an additional $25,000 of my money, they could turn a working viewer into a shrink-wrapped software product. But they, and I, wouldn't want to run a software business. They told me that they could sell the software rights for something like $450,000, and I would then get a third of that. If you could use the technology separately, what about going ahead with the website separately? Suppose the viewer is not functional after four months, but the website proves to be a winner with a little extra effort by the end of month 6what could you do with the website and the music content? First of all, if the viewer didn't work, I'm sure we could arrange temporary rights with the alternate inferior viewer to test the website. If the website is successful, we could, after six months, build a website business by switching to a license of the alternate viewer. The value of the web business would be lower since the licensed viewer would not read les from existing notation software. I think we would sell the business to the owner of the other viewer in that case. We could probably get $300,000 for the sale, and remember, I only get a third of that. Do you have any ideas on how to expand on the basic business if both the technology and website are successful after six months? One thing that came up in our conversations was to build upon our viewer's ability to directly read the les created by working composers. We thought about adding a capability for composers to upload their compositions to the website and earn either free copies of other works or royalties. This capability could be added after six months of operating a viable business, or 12 months from now. The online upload capability would take an additional $450,000 at the time the decision to expand was taken. I would put up my third of this money, and the other owners would nd nancing for their shares of it as well. The upload expansion would about double the value of the business (by the end of month 12 of operation, 18 months from now) from its base level without the expanded capability. I think the decision to nance this expansion would be taken only if the venture showed a good EBITDA.3 I know if the EBITDA were as much as $18,000 per month we would expand, maybe for less. I would make sure in our start-up agreements that I had the right to make the decision about whether to expand in this particular way. I've now heard three grand ideas to add value to your venture. Let me add one more before dessert comes. This is based on something I've been wondering since you started talking about this business. Who has control in this business, and to what started talking about this business. Who has control in this business, and to what extent do you think these guys can make the right calls on running the company? Can you nd a way to get more ownership and, perhaps, control if it is a viable business? Bernard: One thing that worries me is that, if Chris and Mark get a working viewer, and quality website content together, they may not have enough business skill to really develop 3 Earnings before interest, taxes, depreciation, and amortization. leument is authorized for use only by Me: Shalabi in Business Investment Valuation-1-1-1-1 taught by FERHAT AKBAS, University of Illinois at Chicago from Jan 2022 to Jul : For the exclusive use of M. Shalabi, 202 -4- UV0361 and run the business. The thing is, they realize this also, unlike many founders. I believe they will agree to let me buy out some of their shares if the business works wellat least enough to give me control of the business and pick the management. Let's assume they would accept a clause in our start-up documents that would allow me to pay, say, $250,000, to buy 17% more of the company (giving me a controlling 501/3.% share) 18 months from now. They'd be happy to get some cash for their success and, at the same time, retain interest in the business. Bouchek: That clause could give you a bargain price on what could, at that time, be very valuable shares, even without considering the extra worth of having a controlling interest. You're lucky that they would give you that. I'll tell you what: I'll pay for dinner if you let me have the deal. Bernard: Well, I'm not going to give the deal away and I want to think more about the value of the ideas the four of you have given me. Let me say thanks to you all by taking care of the check. Bernard picked up the paper napkin showing the timeline he had drawn while they spoke Bernard picked up the paper napkin showing the timeline he had drawn while they spoke (Exhibit 1), said goodbye to his friends, and drove home, thinking that each idea he'd gotten from the dinner conversation could be worth hundreds of times the cost of dinner. Are there other opportunities he ought to consider as well? First, he would evaluate the current ideas. Tomorrow he would ask his newly minted MBA hire to develop a model to value a viable base business, starting after the six-month development period, assuming that both the viewer and website prove out (see Exhibit 2 for the spreadsheet model4 that was produced). The two of them could then see how much incremental gain arose from each of the four ideas, over and above the value of the original opportunity he had been ready to reject. The spreadsheet would be useful for those opportunities that arose after the business became viable. His usual approach was to value companies using a multiple of EBITDA. The analysis he envisioned would only go up to 18 months, as he would denitely sell his interest at that point. He felt condent that he could maintain decision-making control in return for putting up the money needed for each opportunity. The equal share ownership would not change if he actually canin out any of the ideas, except for Bouchek's buyout idea. He wondered whether $18,000 per month EBITDA was the right cutoff point for going ahead with the expansion, as well as how he would decide whether to purchase additional shares and control of the company. Control of a viable company was worth around $100,000 in and of itself, he thought. The valuation model would allow him to assess the value of each idea so he could revisit the decision about the basic investment opportunity. -5- UV0361 Exhibit 1 SCOR-eSTORE.COM SCOR-eSTORE Timeline Month O 4 6 12 18 Develop Operate Launch and run business Continue to run business prototype website for six months months 7 to 12 pilot Competitive viewer? Expand? Buyout? Winning website

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance