Question

Explain in a minimum of one paragrapth on the Point/Counterpoint topics from Chapters 11, 12, and 13. Chapter 11: Offshore Financial Centers Chapter 12: Strategic

Explain in a minimum of one paragrapth on the Point/Counterpoint topics from Chapters 11, 12, and 13.

Chapter 11: Offshore Financial Centers Chapter 12: Strategic Planning Chapter 13: Companies in Violent Areas

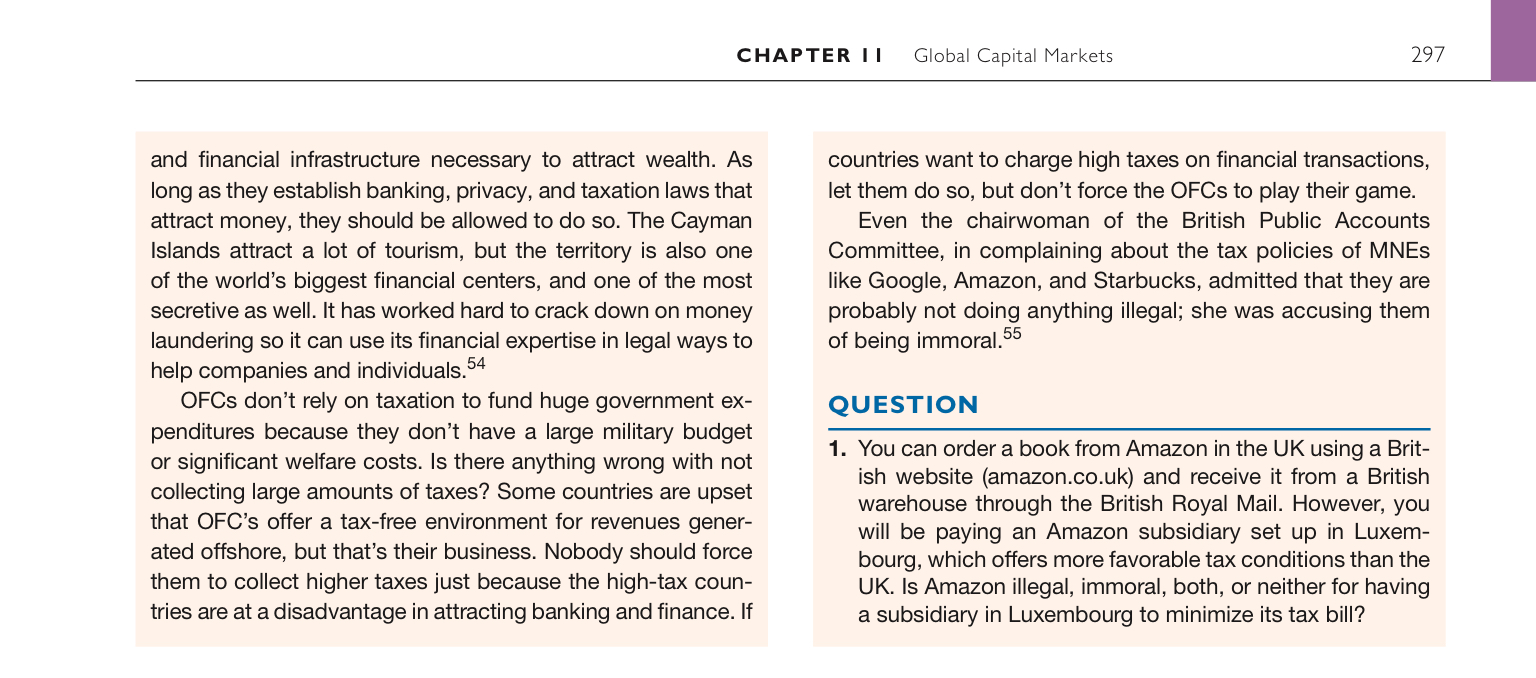

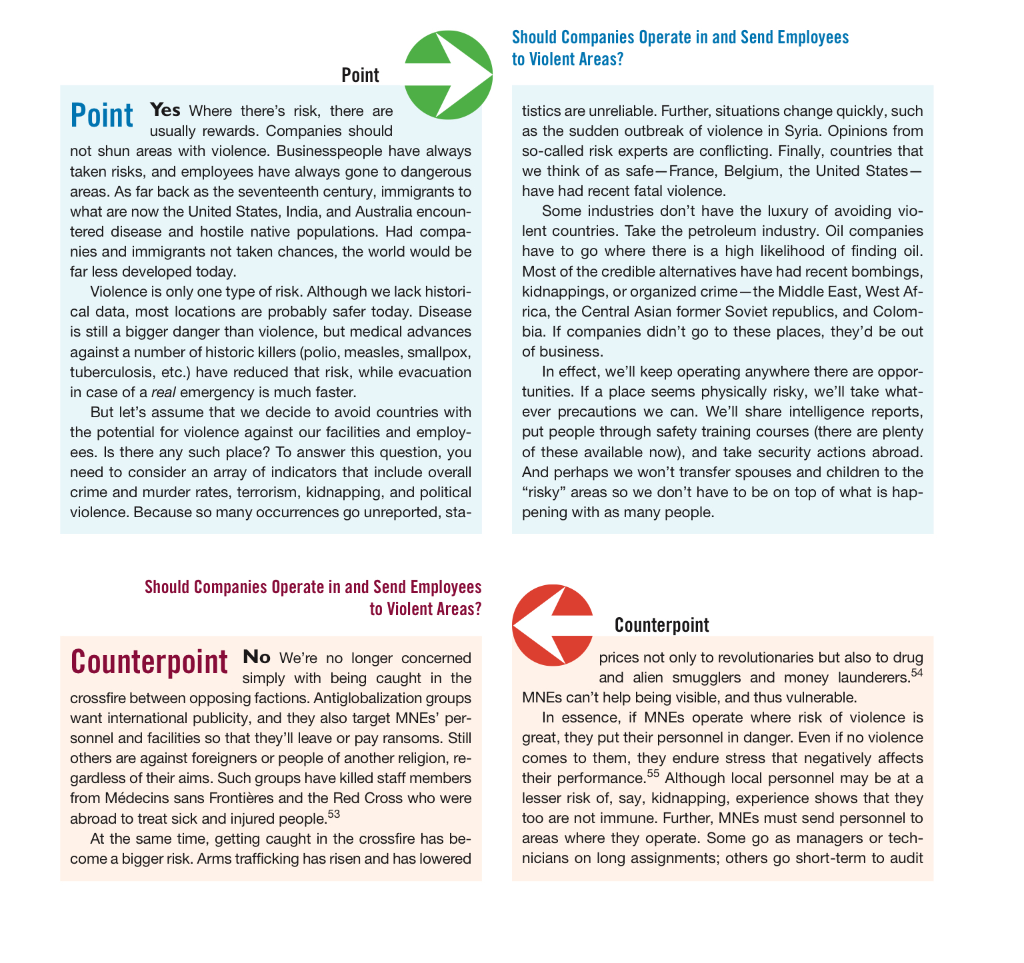

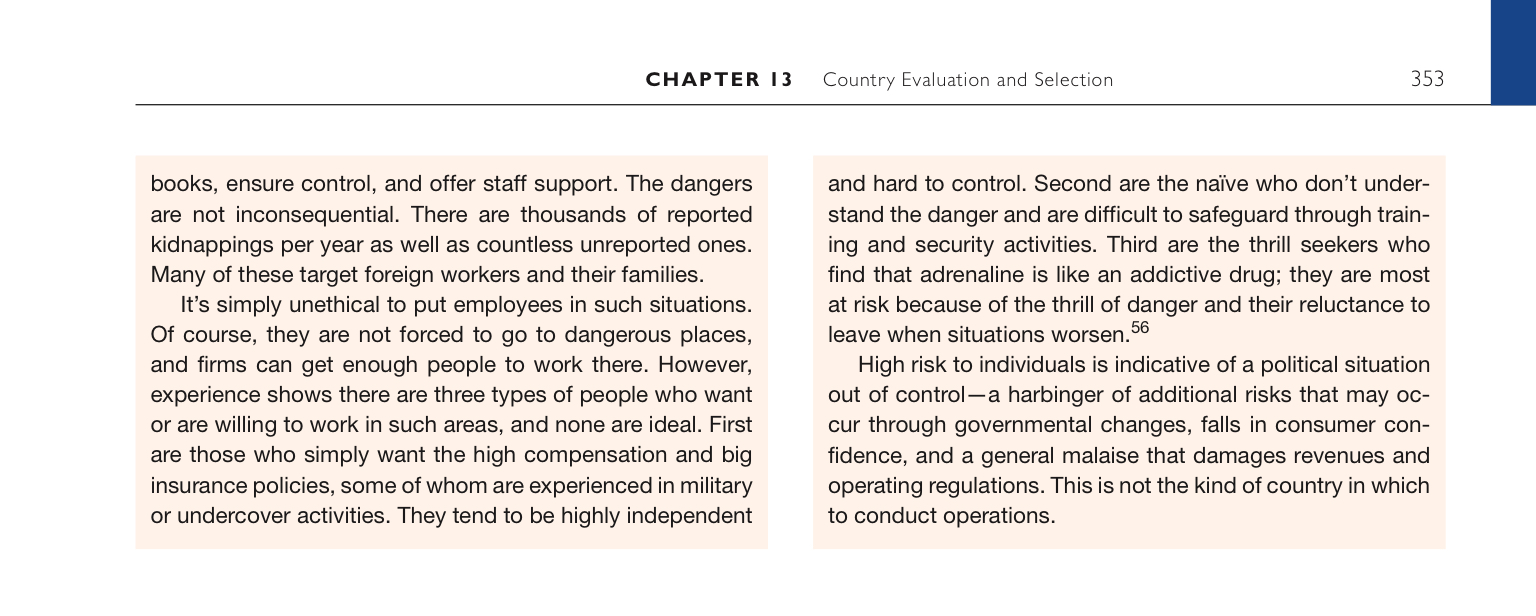

Chapter 11

Chapter 12

Chapter 13

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Principles Of Cost Accounting

Authors: Edward J. Vanderbeck

15th Edition

978-0840037039, 0840037031