Answered step by step

Verified Expert Solution

Question

1 Approved Answer

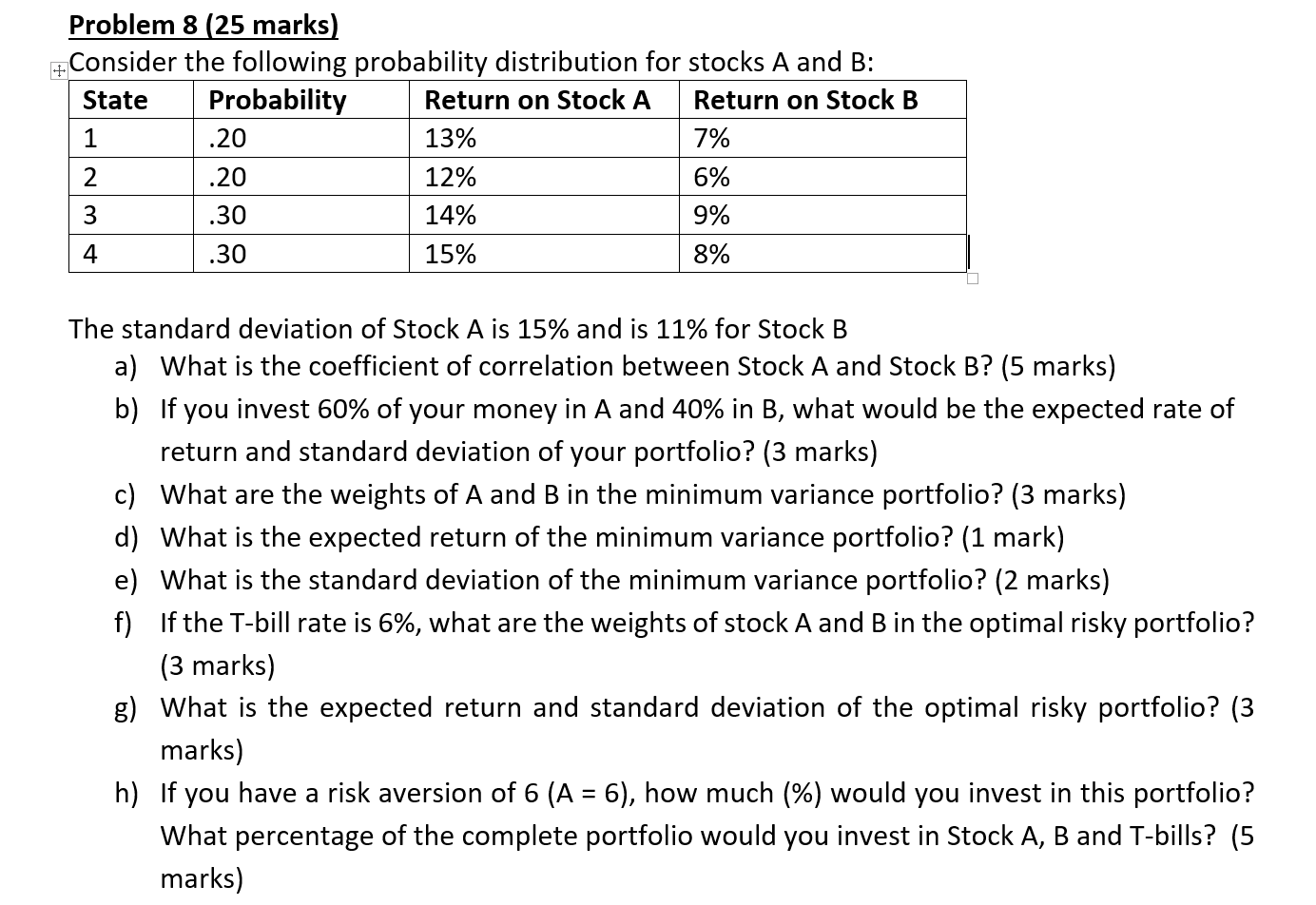

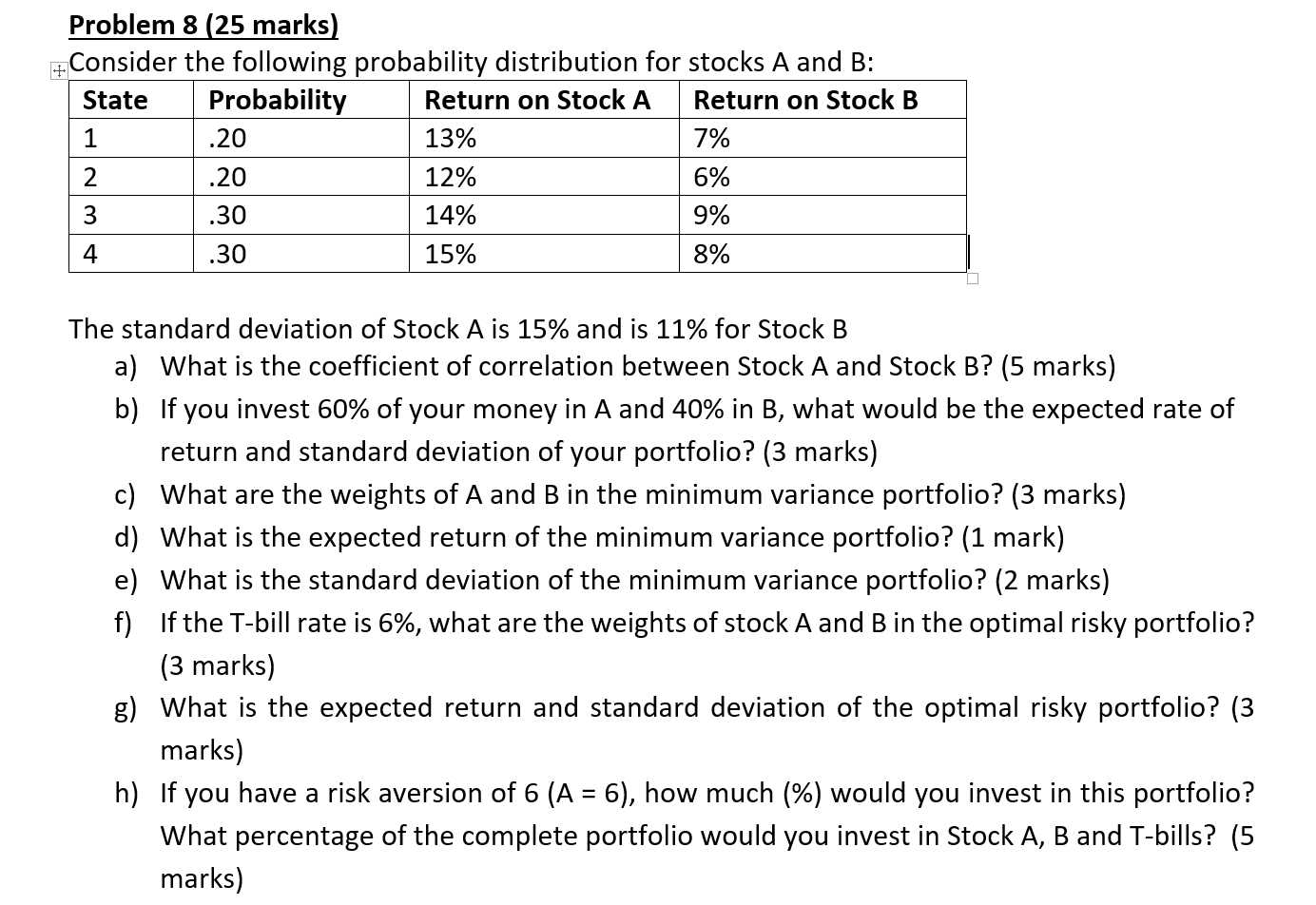

Problem 8 (25 marks) Consider the following probability distribution for stocks A and B: State 1 2 3 4 Probability .20 .20 .30 .30

Problem 8 (25 marks) Consider the following probability distribution for stocks A and B: State 1 2 3 4 Probability .20 .20 .30 .30 Return on Stock A Return on Stock B 15% 70/0 6% 90/0 8% The standard deviation of Stock A is 15% and is 11% for Stock B a) b) c) d) e) f) g) h) What is the coefficient of correlation between Stock A and Stock B? (5 marks) If you invest 60% of your money in A and 40% in B, what would be the expected rate of return and standard deviation of your portfolio? (3 marks) What are the weights of A and B in the minimum variance portfolio? (3 marks) What is the expected return of the minimum variance portfolio? (1 mark) What is the standard deviation of the minimum variance portfolio? (2 marks) If the T-bill rate is 6%, what are the weights of stock A and B in the optimal risky portfolio? (3 marks) What is the expected return and standard deviation of the optimal risky portfolio? (3 marks) If you have a risk aversion of 6 (A = 6), how much (%) would you invest in this portfolio? What percentage of the complete portfolio would you invest in Stock A, B and T-bills? (5 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Theory And Practice

Authors: Eugene Brigham, Michael Ehrhardt, Jerome Gessaroli, Richard Nason

3rd Canadian Edition

017658305X, 978-0176583057