Answered step by step

Verified Expert Solution

Question

1 Approved Answer

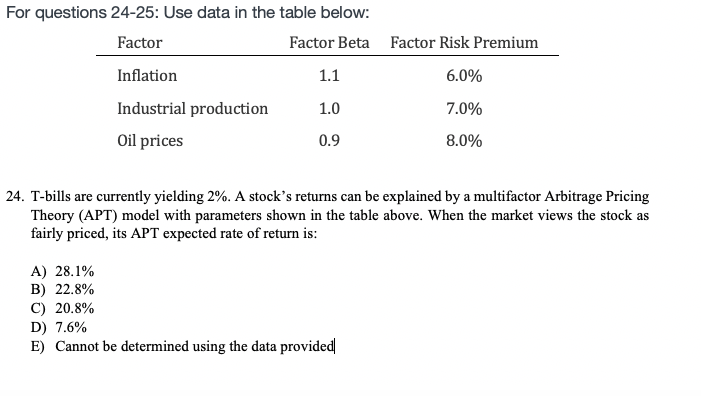

Factor Risk Premium For questions 24-25: Use data in the table below: Factor Factor Beta Inflation 1.1 Industrial production 1.0 Oil prices 0.9 6.0% 7.0%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Stochastic Volatility In Financial Markets Crossing The Bridge To Continuous Time

Authors: Antonio Mele, Fabio Fornari

1st Edition

0792378423, 1461545331, 9780792378426, 9781461545330