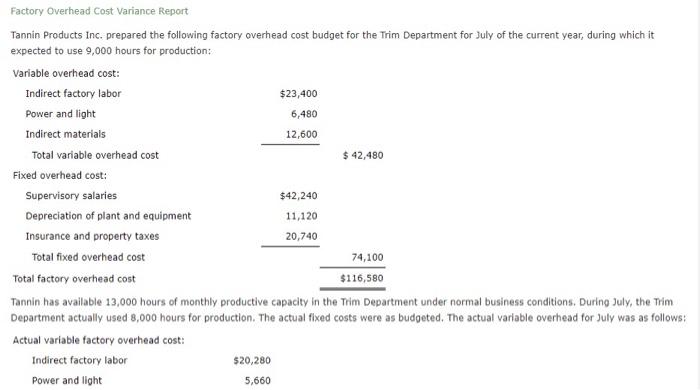

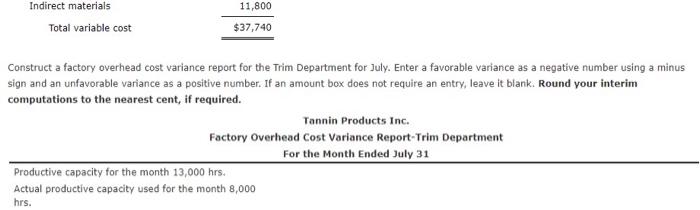

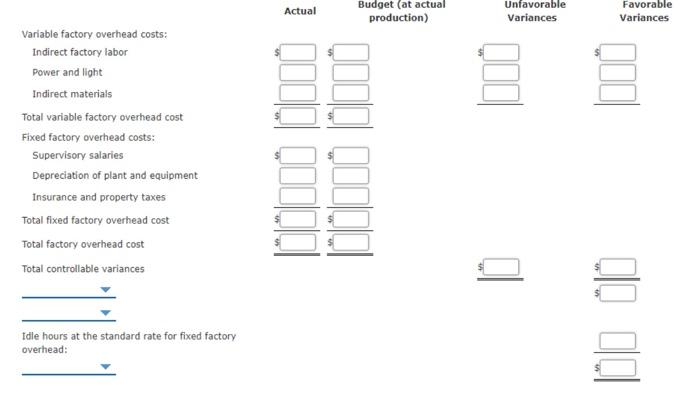

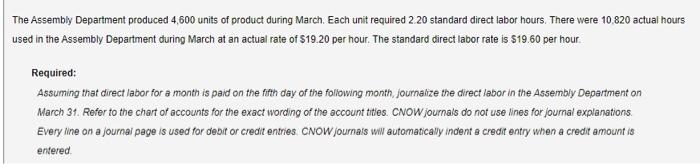

Factory Overhead Cost Variance Report Tannin Products Inc. prepared the following factory overhead cost budget for the Trim Department for July of the current year, during which it expected to use 9,000 hours for production: Variable overhead cost: Indirect factory labor $23,400 Power and light 6,480 Indirect materials 12,600 Total variable overhead cost $ 42,480 Fixed overhead cost: Supervisory salaries $42,240 Depreciation of plant and equipment 11,120 Insurance and property taxes 20,740 Total fixed overhead cost 74,100 Total factory overhead cost $116,580 Tannin has available 13,000 hours of monthly productive capacity in the Trim Department under normal business conditions. During July, the Trim Department actually used 8,000 hours for production. The actual fixed costs were as budgeted. The actual variable overhead for July was as follows: Actual variable factory overhead cost: Indirect factory labor $20,280 Power and light 5,660 11,800 Indirect materials Total variable cost $37,740 Construct a factory overhead cost variance report for the Trim Department for July. Enter a favorable variance as a negative number using a minus sign and an unfavorable variance as a positive number. If an amount box does not require an entry, leave it blank. Round your interim computations to the nearest cent, if required. Tannin Products Inc. Factory Overhead Cost Variance Report-Trim Department For the Month Ended July 31 Productive capacity for the month 13,000 hrs. Actual productive capacity used for the month 8,000 hrs. Actual Budget (at actual production) Unfavorable Variances Favorable Variances Variable factory overhead costs: Indirect factory labor Power and light Indirect materials Total variable factory overhead cost Fixed factory overhead costs: Supervisory salaries Depreciation of plant and equipment Insurance and property taxes Total fixed factory overhead cost Total factory overhead cost Total controllable variances Idle hours at the standard rate for fixed factory overhead: The Assembly Department produced 4,600 units of product during March. Each unit required 2 20 standard direct labor hours. There were 10,820 actual hours used in the Assembly Department during March at an actual rate of $19.20 per hour. The standard direct labor rate is $19.60 per hour. Required: Assuming that direct labor for a month is paid on the fifth day of the following month journalize the direct labor in the Assembly Department on March 31. Refer to the chart of accounts for the exact wording of the account titles. CNOW journals do not use lines for journal explanations Every line on a journal page is used for debit or credit entries. CNOW journals will automatically indente credit entry when a credit amount is entered