Answered step by step

Verified Expert Solution

Question

1 Approved Answer

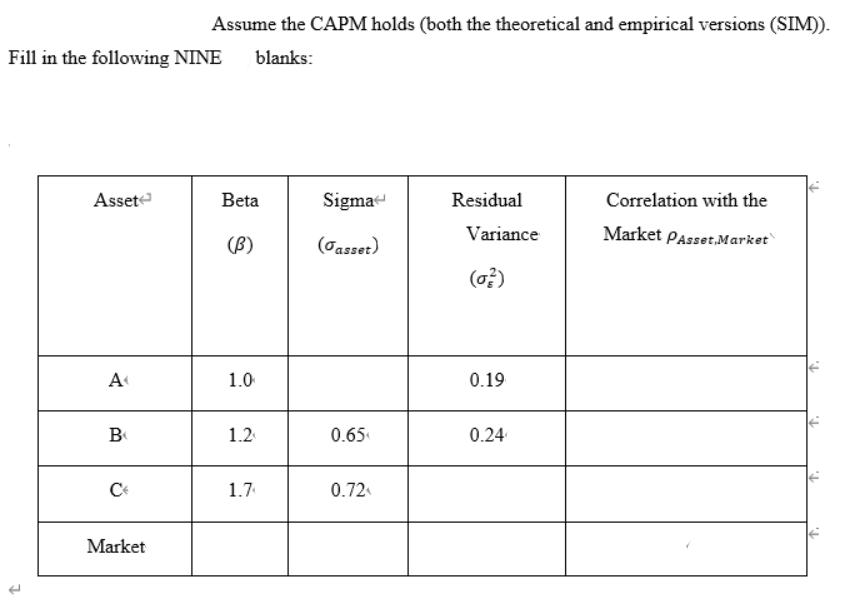

Fill in the following NINE blanks: t Asset A B C Assume the CAPM holds (both the theoretical and empirical versions (SIM)). Market Beta

Fill in the following NINE blanks: t Asset A B C Assume the CAPM holds (both the theoretical and empirical versions (SIM)). Market Beta (B) 1.0 1.2 1.7 Sigma (Jasset) 0.65 0.72 Residual Variance (0) 0.19 0.24 Correlation with the Market PAsset Market 's . .

Step by Step Solution

★★★★★

3.42 Rating (152 Votes )

There are 3 Steps involved in it

Step: 1

For Asset A Beta 10 Sigma Gasset 019 Residual Varia...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Applied Regression Analysis And Other Multivariable Methods

Authors: David G. Kleinbaum, Lawrence L. Kupper, Azhar Nizam, Eli S. Rosenberg

5th Edition

1285051084, 978-1285963754, 128596375X, 978-1285051086