Fill in the form with the code of the following table(the third picture)

for Example

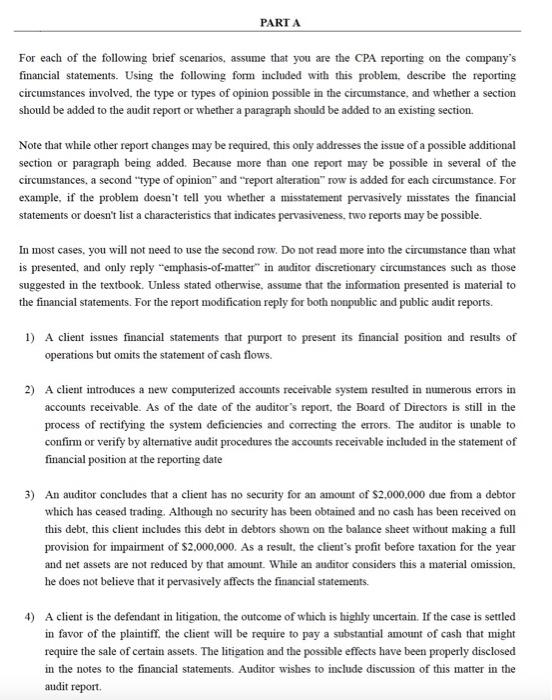

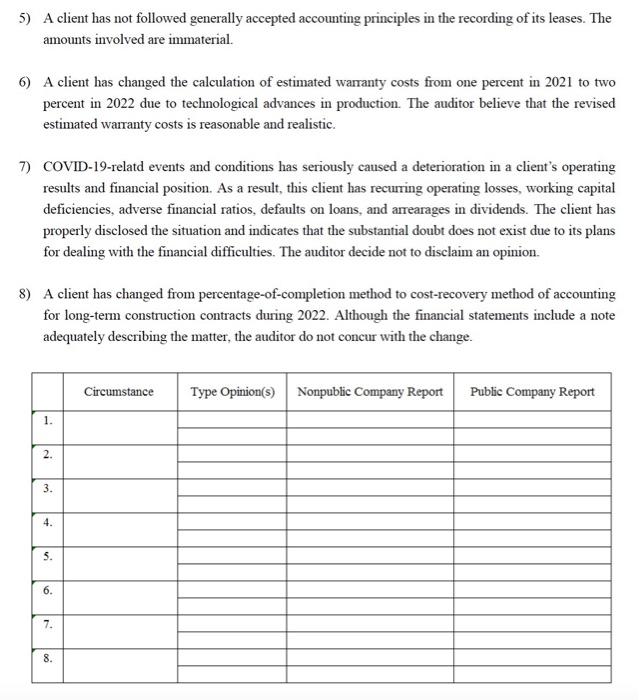

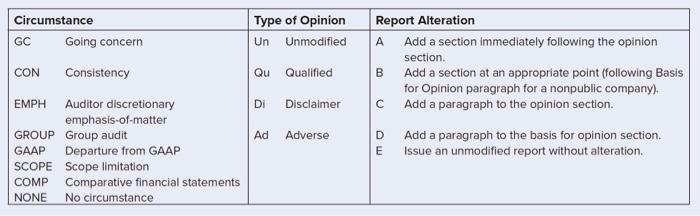

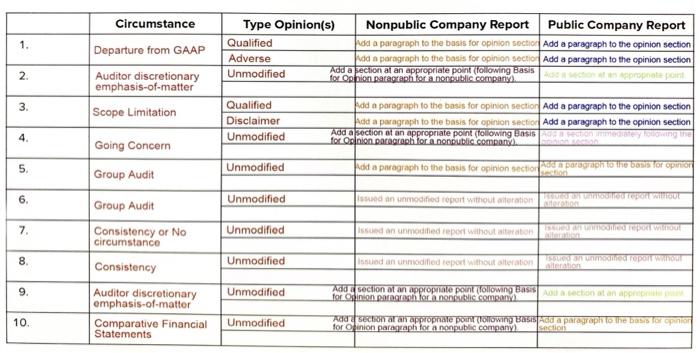

PARTA For each of the following brief scenarios, assume that you are the CPA reporting on the company's financial statements. Using the following form included with this problem, describe the reporting circumstances involved, the type or types of opinion possible in the circumstance, and whether a section should be added to the audit report or whether a paragraph should be added to an existing section. Note that while other report changes may be required, this only addresses the issue of a possible additional section or paragraph being added. Because more than one report may be possible in several of the circumstances, a second "type of opinion" and "report alteration" row is added for each circumstance. For example, if the problem doesn't tell you whether a misstatement pervasively misstates the financial statements or doesn't list a characteristics that indicates pervasiveness, two reports may be possible. In most cases, you will not need to use the second row. Do not read more into the circumstance than what is presented, and only reply emphasis-of-matter in auditor discretionary circumstances such as those suggested in the textbook. Unless stated otherwise, assume that the information presented is material to the financial statements. For the report modification reply for both nonpublic and public audit reports. 1) A client issues financial statements that purport to present its financial position and results of operations but omits the statement of cash flows. 2) A client introduces a new computerized accounts receivable system resulted in numerous errors in accounts receivable. As of the date of the auditor's report, the Board of Directors is still in the process of rectifying the system deficiencies and correcting the errors. The auditor is unable to confinnor verify by alterative audit procedures the accounts receivable included in the statement of financial position at the reporting date 3) An auditor concludes that a client has no security for an amount of $2.000.000 due from a debtor which has ceased trading. Although no security has been obtained and no cash has been received on this debt, this client includes this debt in debtors shown on the balance sheet without making a full provision for impairment of $2.000.000. As a result, the client's profit before taxation for the year and net assets are not reduced by that amount. While an auditor considers this a material omission. he does not believe that it pervasively affects the financial statements. 4) A client is the defendant in litigation, the outcome of which is highly uncertain. If the case is settled in favor of the plaintiff. the client will be require to pay a substantial amount of cash that might require the sale of certain assets. The litigation and the possible effects have been properly disclosed in the notes to the financial statements. Auditor wishes to include discussion of this matter in the audit report 5) A client has not followed generally accepted accounting principles in the recording of its leases. The amounts involved are immaterial. 6) A client has changed the calculation of estimated warranty costs from one percent in 2021 to two percent in 2022 due to technological advances in production. The auditor believe that the revised estimated warranty costs is reasonable and realistic. 7) COVID-19-relatd events and conditions has seriously caused a deterioration in a client's operating results and financial position. As a result, this client has recurring operating losses, working capital deficiencies, adverse financial ratios, defaults on loans, and arrearages in dividends. The client has properly disclosed the situation and indicates that the substantial doubt does not exist due to its plans for dealing with the financial difficulties. The auditor decide not to disclaim an opinion. 8) A client has changed from percentage-of-completion method to cost-recovery method of accounting for long-term construction contracts during 2022. Although the financial statements include a note adequately describing the matter, the auditor do not concur with the change. Circumstance Type Opinion(s) Nonpublic Company Report Public Company Report 1. 2. 3. 4. 5. 6. 7. 8 . Circumstance GC Going concern CON Consistency Type of Opinion Un Unmodified Qu Qualified Report Alteration A Add a section immediately following the opinion section B Add a section at an appropriate point (following Basis for Opinion paragraph for a nonpublic company) C Add a paragraph to the opinion section. D Add a paragraph to the basis for opinion section. E Issue an unmodified report without alteration. DI Disclaimer Ad Adverse EMPH Auditor discretionary emphasis-of-matter GROUP Group audit GAAP Departure from GAAP SCOPE Scope limitation COMP Comparative financial statements NONE No circumstance 1. Circumstance Departure from GAAP Auditor discretionary emphasis-of-matter Scope Limitation Type Opinion(s) Nonpublic Company Report Public Company Report Qualified dd a paragraph to the basis for opinion section Add a paragraph to the opinion section Adverse Add a paragraph to the basis for opinion section Add a paragraph to the opinion section Unmodified Add a section at an appropriate point (following Basis for Opinion paragraph for a nonpublic company po pot 2. 3. Qualified Disclaimer Unmodified dd a paragraph to the basis for opinion section Add a paragraph to the opinion section Add a paragraph to the basis for opinion sectio Add a paragraph to the opinion section Add a section at an appropriate point following Basis TING for Onion, paragraph for anonpublic company) 4. Going Concern 5 . Unmodified Group Audit dida paragraph to the basis for opinion sector pronto the basis for por 6. Unmodified issued an unmodified report without tation TITUTE OUE 7. Group Audit Consistency or No circumstance Unmodified Issued an unmodified report without an COW 8 . Unmodified Issued an unidified report without alteration En moderoport 9. Unmodified Consistency Auditor discretionary emphasis of matter Comparative Financial Statements Ada section at an appropriate point lollowing section at an app tar opinion paran Danikaiccompani 10. Unmodified Ada Saran appropriate pourrowing Add a paragraph to the for Onion parempi torinnenpublic company