Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Financal Derivatives. Please answer A-D I really need help in getting the whole lengthy question answered. If you would help, I would greatly appreciate it.

Financal Derivatives. Please answer A-D

I really need help in getting the whole lengthy question answered. If you would help, I would greatly appreciate it. But whatever anyone can answer is fine. Thanks!

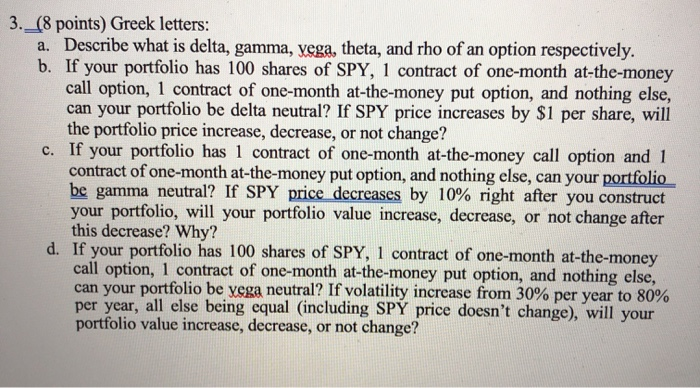

3. _(8 points) Greek letters: a. Describe what is delta, gamma, yega, theta, and rho of an option respectively. b. If your portfolio has 100 shares of SPY, 1 contract of one-month at-the-money call option, 1 contract of one-month at-the-money put option, and nothing else, can your portfolio be delta neutral? If SPY price increases by $1 per share, will the portfolio price increase, decrease, or not change? c. If your portfolio has 1 contract of one-month at-the-money call option and 1 contract of one-month at-the-money put option, and nothing else, can your portfolio be gamma neutral? If SPY price decreases by 10% right after you construct your portfolio, will your portfolio value increase, decrease, or not change after this decrease? Why? d. If your portfolio has 100 shares of SPY, 1 contract of one-month at-the-money call option, 1 contract of one-month at-the-money put option, and nothing else, can your portfolio be vega neutral? If volatility increase from 30% per year to 80% per year, all else being equal (including SPY price doesn't change), will your portfolio value increase, decrease, or not change? 3. _(8 points) Greek letters: a. Describe what is delta, gamma, yega, theta, and rho of an option respectively. b. If your portfolio has 100 shares of SPY, 1 contract of one-month at-the-money call option, 1 contract of one-month at-the-money put option, and nothing else, can your portfolio be delta neutral? If SPY price increases by $1 per share, will the portfolio price increase, decrease, or not change? c. If your portfolio has 1 contract of one-month at-the-money call option and 1 contract of one-month at-the-money put option, and nothing else, can your portfolio be gamma neutral? If SPY price decreases by 10% right after you construct your portfolio, will your portfolio value increase, decrease, or not change after this decrease? Why? d. If your portfolio has 100 shares of SPY, 1 contract of one-month at-the-money call option, 1 contract of one-month at-the-money put option, and nothing else, can your portfolio be vega neutral? If volatility increase from 30% per year to 80% per year, all else being equal (including SPY price doesn't change), will your portfolio value increase, decrease, or not change Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

COMMENT INVESTIR ABC DE LA FINANCE

Authors: OLIVIER CHAZOULE

1st Edition

2020367521, 978-2020367523