Answered step by step

Verified Expert Solution

Question

1 Approved Answer

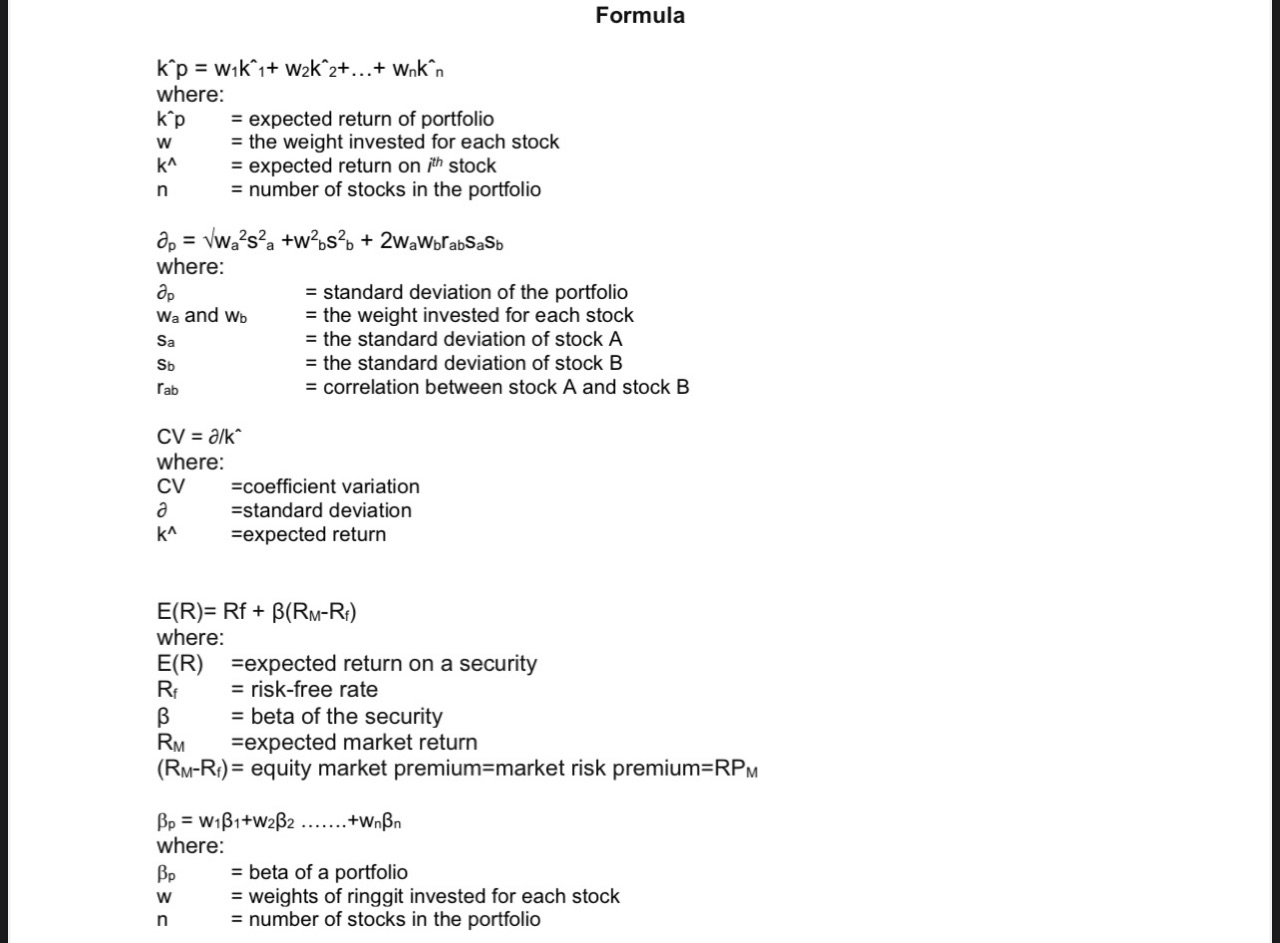

finance Formula k p =W1k 1+ W2k^2+...+ Wnk^n where: kp W k^ n = expected return of portfolio the weight invested for each stock =

finance

Formula k p =W1k 1+ W2k^2+...+ Wnk^n where: kp W k^ n = expected return of portfolio the weight invested for each stock = expected return on ith stock = number of stocks in the portfolio ap = wa2s2a +w2bs + 2WaWbabSaSb where: ap Wa and Wb Sa Sb rab CV = a/k = standard deviation of the portfolio = the weight invested for each stock = the standard deviation of stock A the standard deviation of stock B = correlation between stock A and stock B =coefficient variation where: CV a =standard deviation k^ =expected return E(R) Rf+(RM-Rf) expected return on a security where: E(R) Rf = risk-free rate RM = beta of the security =expected market return (RM-R) equity market premium-market risk premium=RPM p = W11+W22 where: ..+Wnn = beta of a portfolio W = weights of ringgit invested for each stock n = number of stocks in the portfolio

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduction To Corporate Finance

Authors: Laurence Booth, Sean Cleary

3rd Edition

978-1118300763, 1118300769