Answered step by step

Verified Expert Solution

Question

1 Approved Answer

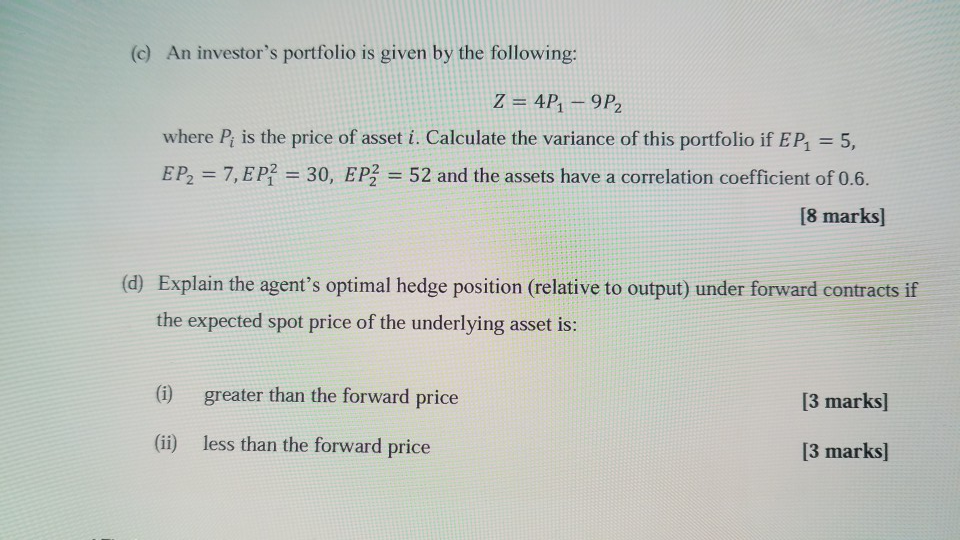

Financial calculators are NOT allowed. (c) An investor's portfolio is given by the following: Z = 4P1-9P2 where P is the price of asset i.

Financial calculators are NOT allowed.

(c) An investor's portfolio is given by the following: Z = 4P1-9P2 where P is the price of asset i. Calculate the variance of this portfolio if EP1 5, EPo = 7,EP-30, EPS = 52 and the assets have a correlation coefficient of 0.6 18 marks] (d) Explain the agent's optimal hedge position (relative to output) under forward contracts if the expected spot price of the underlying asset is: (i) greater than the forward price 3 marks] (ii) less than the forward price 13 marks] (c) An investor's portfolio is given by the following: Z = 4P1-9P2 where P is the price of asset i. Calculate the variance of this portfolio if EP1 5, EPo = 7,EP-30, EPS = 52 and the assets have a correlation coefficient of 0.6 18 marks] (d) Explain the agent's optimal hedge position (relative to output) under forward contracts if the expected spot price of the underlying asset is: (i) greater than the forward price 3 marks] (ii) less than the forward price 13 marks]Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Asset Allocation And Private Markets A Guide To Investing With Private Equity Private Debt And Private Real Assets

Authors: Cyril Demaria, Maurice Pedergnana, Remy He, Roger Rissi, Sarah Debrand

1st Edition

1119381002, 978-1119381006