FINANCIAL:

CUSTOMER:

PROCESS:

LEARNING AND GROWTH:

I just need help on how to solve each category on excel, thank you

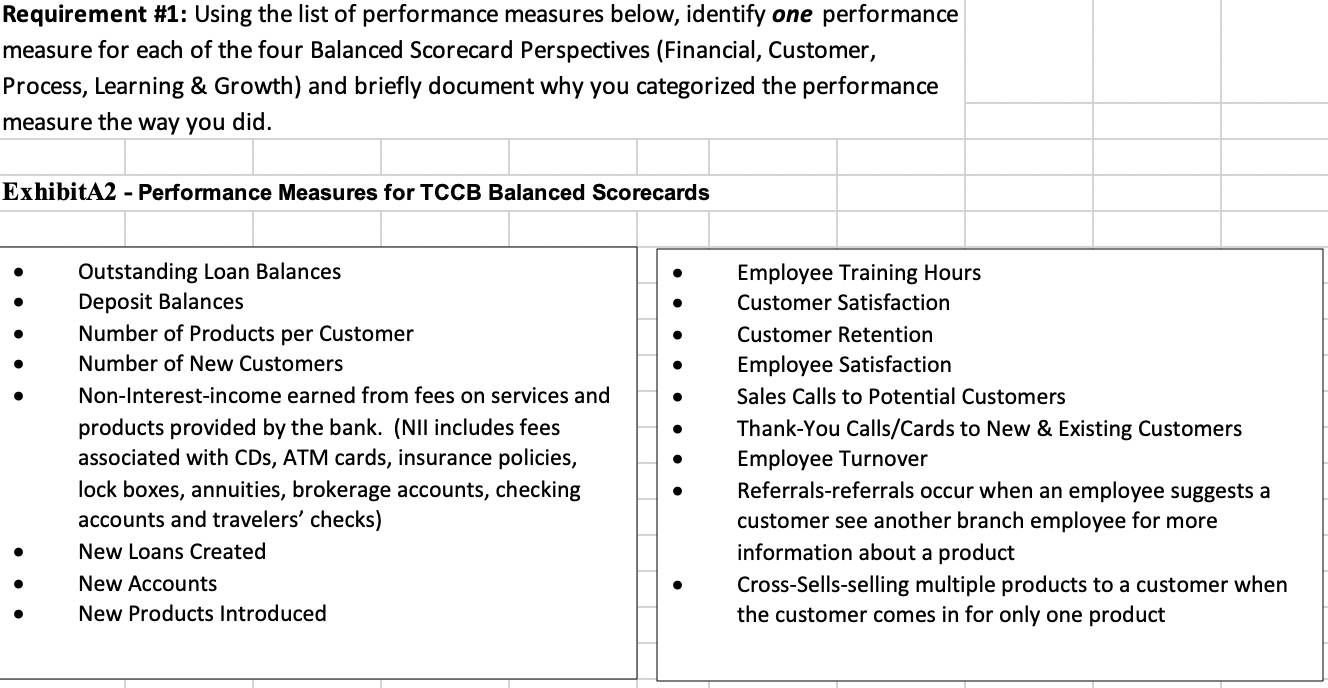

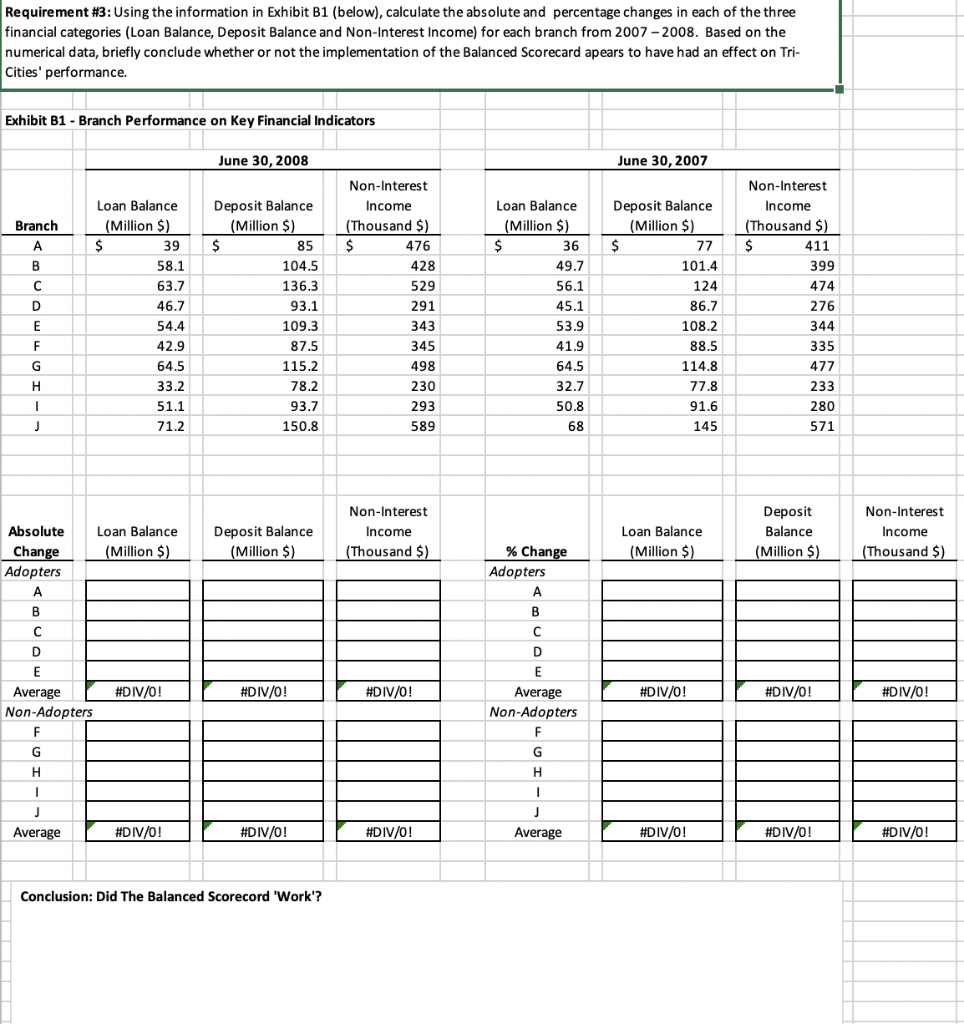

Requirement #1: Using the list of performance measures below, identify one performance measure for each of the four Balanced Scorecard Perspectives (Financial, Customer, Process, Learning & Growth) and briefly document why you categorized the performance measure the way you did. ExhibitA2 - Performance Measures for TCCB Balanced Scorecards Outstanding Loan Balances Deposit Balances Number of Products per Customer Number of New Customers Non-Interest-income earned from fees on services and products provided by the bank. (NII includes fees associated with CDs, ATM cards, insurance policies, lock boxes, annuities, brokerage accounts, checking accounts and travelers' checks) New Loans Created New Accounts New Products Introduced Employee Training Hours Customer Satisfaction Customer Retention Employee Satisfaction Sales Calls to Potential customers Thank You Calls/Cards to New & Existing Customers Employee Turnover Referrals-referrals occur when an employee suggests a customer see another branch employee for more information about a product Cross-Sells-selling multiple products to a customer when the customer comes in for only one product Requirement #3: Using the information in Exhibit B1 (below), calculate the absolute and percentage changes in each of the three financial categories (Loan Balance, Deposit Balance and Non-Interest Income) for each branch from 2007-2008. Based on the numerical data, briefly conclude whether or not the implementation of the Balanced Scorecard apears to have had an effect on Tri- Cities' performance. Exhibit B1 - Branch Performance on Key Financial Indicators June 30, 2008 June 30, 2007 85 Branch B D E Loan Balance (Million $) $ 39 58.1 63.7 46.7 54.4 42.9 64.5 33.2 51.1 71.2 Deposit Balance (Million $) $ 104.5 136.3 93.1 109.3 87.5 115.2 78.2 93.7 150.8 Non-Interest Income (Thousand $) $ 476 428 529 291 343 345 498 230 293 589 Loan Balance (Million $) $ 36 49.7 56.1 45.1 53.9 41.9 64.5 32.7 50.8 Deposit Balance (Million $) $ 77 101.4 124 86.7 108.2 88.5 114.8 77.8 91.6 145 Non-Interest Income (Thousand $) $ 411 399 474 276 344 335 477 233 280 571 F G H 1 J 68 Deposit Balance (Million $) Non-Interest Income (Thousand $) Loan Balance (Million $) Deposit Balance (Million $) Non-Interest Income (Thousand $) Absolute Loan Balance Change (Million $) Adopters A B D E Average #DIV/0! Non-Adopters F G H 1 J Average #DIV/0! % Change Adopters A B D E Average Non-Adopters F G H #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0! J Average #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0! Conclusion: Did The Balanced Scorecord 'Work? Requirement #1: Using the list of performance measures below, identify one performance measure for each of the four Balanced Scorecard Perspectives (Financial, Customer, Process, Learning & Growth) and briefly document why you categorized the performance measure the way you did. ExhibitA2 - Performance Measures for TCCB Balanced Scorecards Outstanding Loan Balances Deposit Balances Number of Products per Customer Number of New Customers Non-Interest-income earned from fees on services and products provided by the bank. (NII includes fees associated with CDs, ATM cards, insurance policies, lock boxes, annuities, brokerage accounts, checking accounts and travelers' checks) New Loans Created New Accounts New Products Introduced Employee Training Hours Customer Satisfaction Customer Retention Employee Satisfaction Sales Calls to Potential customers Thank You Calls/Cards to New & Existing Customers Employee Turnover Referrals-referrals occur when an employee suggests a customer see another branch employee for more information about a product Cross-Sells-selling multiple products to a customer when the customer comes in for only one product Requirement #3: Using the information in Exhibit B1 (below), calculate the absolute and percentage changes in each of the three financial categories (Loan Balance, Deposit Balance and Non-Interest Income) for each branch from 2007-2008. Based on the numerical data, briefly conclude whether or not the implementation of the Balanced Scorecard apears to have had an effect on Tri- Cities' performance. Exhibit B1 - Branch Performance on Key Financial Indicators June 30, 2008 June 30, 2007 85 Branch B D E Loan Balance (Million $) $ 39 58.1 63.7 46.7 54.4 42.9 64.5 33.2 51.1 71.2 Deposit Balance (Million $) $ 104.5 136.3 93.1 109.3 87.5 115.2 78.2 93.7 150.8 Non-Interest Income (Thousand $) $ 476 428 529 291 343 345 498 230 293 589 Loan Balance (Million $) $ 36 49.7 56.1 45.1 53.9 41.9 64.5 32.7 50.8 Deposit Balance (Million $) $ 77 101.4 124 86.7 108.2 88.5 114.8 77.8 91.6 145 Non-Interest Income (Thousand $) $ 411 399 474 276 344 335 477 233 280 571 F G H 1 J 68 Deposit Balance (Million $) Non-Interest Income (Thousand $) Loan Balance (Million $) Deposit Balance (Million $) Non-Interest Income (Thousand $) Absolute Loan Balance Change (Million $) Adopters A B D E Average #DIV/0! Non-Adopters F G H 1 J Average #DIV/0! % Change Adopters A B D E Average Non-Adopters F G H #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0! J Average #DIV/0! #DIV/0! #DIV/0! #DIV/0! #DIV/0! Conclusion: Did The Balanced Scorecord 'Work