Answered step by step

Verified Expert Solution

Question

1 Approved Answer

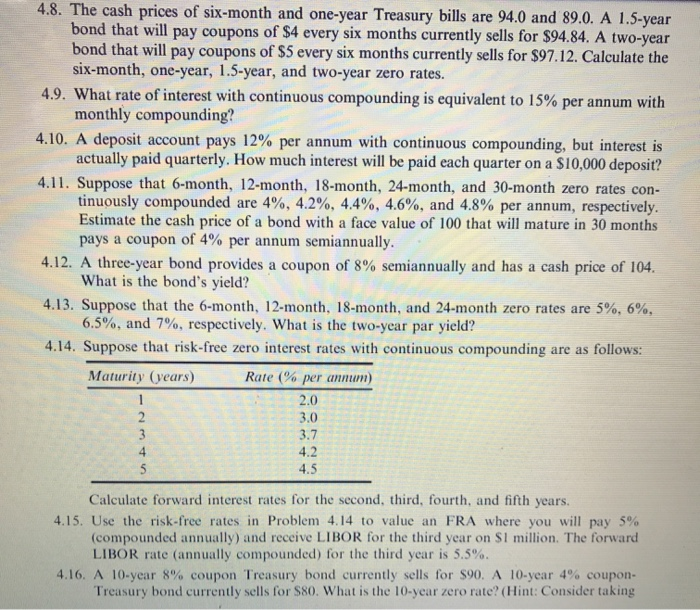

Financial Derivatives No more needs for the questions to be answered 4.8. The cash prices of six-month and one-year Treasury bills are 94.0 and 89.0.

Financial Derivatives

No more needs for the questions to be answered

4.8. The cash prices of six-month and one-year Treasury bills are 94.0 and 89.0. A 1.5-year bond that will pay coupons of $4 every six months currently sells for $94.84. A two-year bond that will pay coupons of $5 every six months currently sells for $97.12. Calculate the six-month, one-year, 1.5-year, and two-year zero rates. 4.9. What rate of interest with continuous compounding is equivalent to 15% per annum with monthly compounding? 4.10. A deposit account pays 12% per annum with continuous compounding, but interest is actually paid quarterly. How much interest will be paid each quarter on a $10,000 deposit? 4.11. Suppose that 6-month, 12-month, 18-month, 24-month, and 30-month zero rates con- tinuously compounded are 4%, 4.2%, 4.4%, 4.6%, and 4.8% per annum, respectively. Estimate the cash price of a bond with a face value of 100 that will mature in 30 months pays a coupon of 4% per annum semiannually. 4.12. A three-year bond provides a coupon of 8% semiannually and has a cash price of 104. What is the bond's yield? 4.13. Suppose that the 6-month, 12-month, 18-month, and 24-month zero rates are 5%, 6%, 6.5%, and 7%, respectively. What is the two-year par yield? 4.14. Suppose that risk-free zero interest rates with continuous compounding are as follows: Maturity (years) Rate (% per annum) Calculate forward interest rates for the second third, fourth, and fifth years. 4.15. Use the risk-free rates in Problem 4.14 to value an FRA where you will pay 5% (compounded annually) and receive LIBOR for the third year on S1 million. The forward LIBOR rate (annually compounded) for the third year is 5.5%. 4.16. A 10-year 8% coupon Treasury bond currently sells for $90. A 10-year 4% coupon- Treasury bond currently sells for $80. What is the 10-year zero rate? (Hint: Consider taking Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Nurse Managers Guide To Budgeting And Finance

Authors: Al Rundio

2nd Edition

1940446589, 978-1940446585