FINANCING NEW VENTURES Chapter 4 - Determining the amount of capital you need

Could someone answer several questions of the following? Just please answer what you make sure, don't need all of them:

Too little, you may miss your milestone and next round will be costly, if available at all

Too much, current round is too costly. Too much dilution and tendency to waste it.

Like Goldilocks, it should be just right.

Market for capital is very cyclical.

Reached $100 billion is 1999, and dropped to $10 billion by 2009, and was not exceeded again until 2018 and 2019. This year? Who knows but it won't be much.

How to determine needs?

TRADITIONAL - Build a cash flow statement projection. Generally out 4 to 5 years. Always do monthly or at least quarterly. Why?

Seasonality. Can kill companies. Think of a snowboard company that one of my students had. Received lots of money in winter. None in summer. But when did he need to buy materials? Yup, in the summer. Better have saved enough cash or was able to finance it.

Determine your key drivers/assumptions of cash flow growth.

STARTUP - Revenues and expenses highly variable and subjective, especially revenues.

It's either a winner or loser, not much middle ground.

Some do 2 or 3 projections.

- most likely scenario

- worst case scenario

- best case (but why bother with this one?)

Be careful with spreadsheets, they may imply a fake sense of precision. That doesn't mean don't do one. Just understand the limitations and assumptions. Be flexible, not rigid. Use high level quick and dirty projections as a gut check.

What absorbs the most capital?

1) Obviously capital assets. Equipment, buildings, vehicles, but also patents. Lease if you can. You can even lease (license) a patent rather than reinvent the wheel. Lease rates may seem high but they're cheaper than VCs. Also capital assets are less these days.

Use the cloud for computer hardware/software. Generally incurred up front first year, unless deferred thru leasing (preferred).

2) Product development. R&D. Cost of engineers and developers. Less upfront than capex but mostly in early years 1-3.

Least deferrable, must be paid. #1 priority. Without it you have no product.

3) Sales & marketing. Engineers often forget this or don't think it's important. "Build the best mousetrap and they will come." Not!

Often the biggest component of expense. Comes later. Years 2-4. Can be deferred but revenue growth will suffer.

4) Working capital (inventory & receivables). Also often overlooked. Cash versus accrual problem when projecting. Also can be very seasonal. Think farmers, ski resorts, campgrounds, sports. Affects all growing businesses all years.

5) Lastly leadership and admin. Most discretionary as leaders & execs can take equity vs. cash. Often paid out greatest in exit strategy.

See working capital models on pages 86 & 87 in the book. Ex. 4.2 and 4.3. See how growth sucks up capital.

If you can, develop a business model with positive working capital cash flows:

1) Gift cards

2) Loyalty programs. Points paid up front.

3) Some grocery stores, retailers, Walmart, although generally only if you are big. small guys must pay cash.

4) Insurance companies

5) Amazon (over 100 days!)

How do investors view the 5 spending buckets?

1) Capital assets? Nay. They would rather you lease.

2) R&D. Essential. High returns. These are the creators.

3) Leadership & admin. Leaders yes. Admin no. Outsource your HR, IT, and accounting.

4) Working capital. No. Deadweight. They won't invest in businesses with negative 180 days working capital.

5) Sales & marketing. Almost as essential as R&D.

Click into this topic to discuss the mini cases in the pictures.

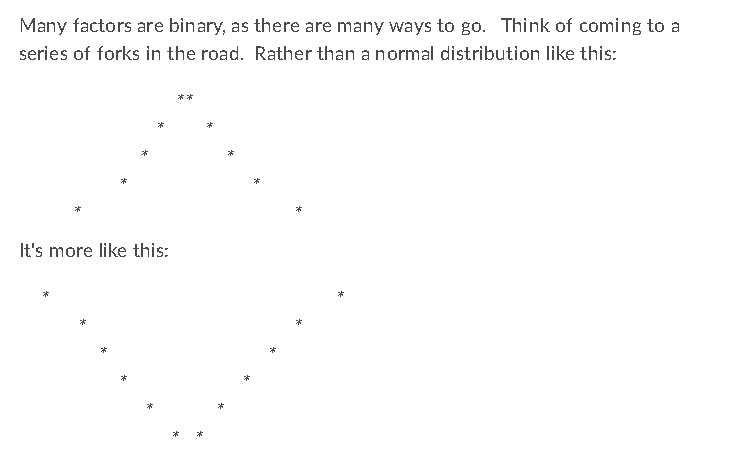

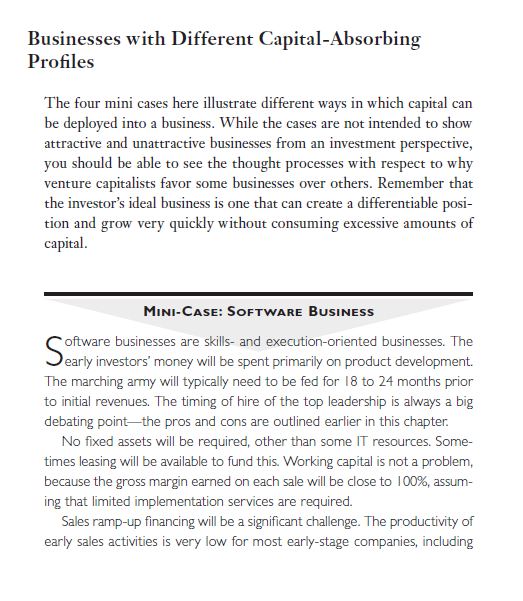

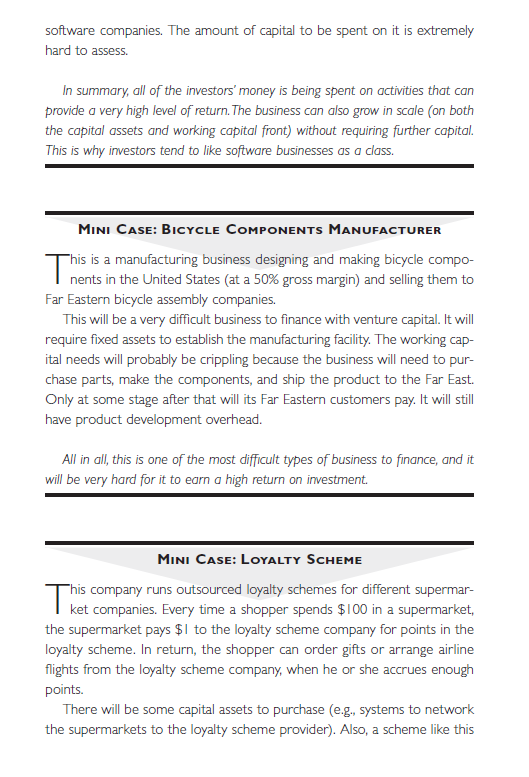

Many factors are binary, as there are many ways to go. Think of coming to a series of forks in the road. Rather than a normal distribution like this: ** * It's more like this: * * * Businesses with Different Capital-Absorbing Profiles The four mini cases here illustrate different ways in which capital can be deployed into a business. While the cases are not intended to show attractive and unattractive businesses from an investment perspective, you should be able to see the thought processes with respect to why venture capitalists favor some businesses over others. Remember that the investor's ideal business is one that can create a differentiable posi- tion and grow very quickly without consuming excessive amounts of capital. MINI-CASE: SOFTWARE BUSINESS oftware businesses are skills- and execution-oriented businesses. The The marching army will typically need to be fed for 18 to 24 months prior to initial revenues. The timing of hire of the top leadership is always a big debating pointthe pros and cons are outlined earlier in this chapter. No fixed assets will be required, other than some IT resources. Some- times leasing will be available to fund this. Working capital is not a problem, because the gross margin earned on each sale will be close to 100%, assum- ing that limited implementation services are required. Sales ramp-up financing will be a significant challenge. The productivity of early sales activities is very low for most early-stage companies, including software companies. The amount of capital to be spent on it is extremely hard to assess In summary, all of the investors' money is being spent on activities that can provide a very high level of return. The business can also grow in scale (on both the capital assets and working capital front) without requiring further capital. This is why investors tend to like software businesses as a class. MINI CASE: BICYCLE COMPONENTS MANUFACTURER This nents in the United States (at a 50% gross margin) and selling them to Far Eastern bicycle assembly companies. This will be a very difficult business to finance with venture capital. It will require fixed assets to establish the manufacturing facility. The working cap- ital needs will probably be crippling because the business will need to pur- chase parts, make the components, and ship the product to the Far East. Only at some stage after that will its Far Eastern customers pay. It will still have product development overhead. All in all, this is one of the most difficult types of business to finance, and it will be very hard for it to earn a high return on investment. . MINI CASE: LOYALTY SCHEME This company runs outsourced loyalty schemes for different supermar- ket companies. Every time a shopper spends $100 in a supermarket, the supermarket pays $1 to the loyalty scheme company for points in the loyalty scheme. In return, the shopper can order gifts or arrange airline flights from the loyalty scheme company, when he or she accrues enough points. There will be some capital assets to purchase (e.g., systems to network the supermarkets to the loyalty scheme provider). Also, a scheme like this can take a long time to achieve breakeven. Supermarkets need to be signed up, customers need to be enticed to enroll, and customers need to start using their cards at the checkout counter. But the working capital position of this type of business can be very attractive. As the supermarkets pay the scheme operator up front when points are earned, these payments can sit on the balance sheet of the loy- alty scheme provider for a long time. People take a long time to accrue points prior to cashing them in. Also, many points are ultimately never cashed in. All this benefits the scheme operator, who should be able to use this cash flow to finance the business as it grows. CM MINI CASE: WIRELESS BROADBAND ROLLOUT apital assets will be a very big part of the financing of this business. The central systems all need to be put in place, and the primary net- work needs to be built. All this needs to happen before even one customer can be signed up. But there are also capital costs associated with every sin- gle customer who signs up. The cost of customer premises equipment and the installation cost of the equipment will rarely be fully covered by the up- front cost paid by the customer. Consequently, every incremental customer (in the early years) will need to be financed by equity. The investors in this business will be looking ahead to the point where the business can transition from equity financing to debt financing. Normally, this will be determined up front in the legal documents governing the financ- ing. The debt providers will commit to providing certain levels of debt when certain milestones are reached. One key milestone might be operating cash flow breakeven. At this point the business will still need to invest in capital assets, but it is generating positive cash flow from operations. Many factors are binary, as there are many ways to go. Think of coming to a series of forks in the road. Rather than a normal distribution like this: ** * It's more like this: * * * Businesses with Different Capital-Absorbing Profiles The four mini cases here illustrate different ways in which capital can be deployed into a business. While the cases are not intended to show attractive and unattractive businesses from an investment perspective, you should be able to see the thought processes with respect to why venture capitalists favor some businesses over others. Remember that the investor's ideal business is one that can create a differentiable posi- tion and grow very quickly without consuming excessive amounts of capital. MINI-CASE: SOFTWARE BUSINESS oftware businesses are skills- and execution-oriented businesses. The The marching army will typically need to be fed for 18 to 24 months prior to initial revenues. The timing of hire of the top leadership is always a big debating pointthe pros and cons are outlined earlier in this chapter. No fixed assets will be required, other than some IT resources. Some- times leasing will be available to fund this. Working capital is not a problem, because the gross margin earned on each sale will be close to 100%, assum- ing that limited implementation services are required. Sales ramp-up financing will be a significant challenge. The productivity of early sales activities is very low for most early-stage companies, including software companies. The amount of capital to be spent on it is extremely hard to assess In summary, all of the investors' money is being spent on activities that can provide a very high level of return. The business can also grow in scale (on both the capital assets and working capital front) without requiring further capital. This is why investors tend to like software businesses as a class. MINI CASE: BICYCLE COMPONENTS MANUFACTURER This nents in the United States (at a 50% gross margin) and selling them to Far Eastern bicycle assembly companies. This will be a very difficult business to finance with venture capital. It will require fixed assets to establish the manufacturing facility. The working cap- ital needs will probably be crippling because the business will need to pur- chase parts, make the components, and ship the product to the Far East. Only at some stage after that will its Far Eastern customers pay. It will still have product development overhead. All in all, this is one of the most difficult types of business to finance, and it will be very hard for it to earn a high return on investment. . MINI CASE: LOYALTY SCHEME This company runs outsourced loyalty schemes for different supermar- ket companies. Every time a shopper spends $100 in a supermarket, the supermarket pays $1 to the loyalty scheme company for points in the loyalty scheme. In return, the shopper can order gifts or arrange airline flights from the loyalty scheme company, when he or she accrues enough points. There will be some capital assets to purchase (e.g., systems to network the supermarkets to the loyalty scheme provider). Also, a scheme like this can take a long time to achieve breakeven. Supermarkets need to be signed up, customers need to be enticed to enroll, and customers need to start using their cards at the checkout counter. But the working capital position of this type of business can be very attractive. As the supermarkets pay the scheme operator up front when points are earned, these payments can sit on the balance sheet of the loy- alty scheme provider for a long time. People take a long time to accrue points prior to cashing them in. Also, many points are ultimately never cashed in. All this benefits the scheme operator, who should be able to use this cash flow to finance the business as it grows. CM MINI CASE: WIRELESS BROADBAND ROLLOUT apital assets will be a very big part of the financing of this business. The central systems all need to be put in place, and the primary net- work needs to be built. All this needs to happen before even one customer can be signed up. But there are also capital costs associated with every sin- gle customer who signs up. The cost of customer premises equipment and the installation cost of the equipment will rarely be fully covered by the up- front cost paid by the customer. Consequently, every incremental customer (in the early years) will need to be financed by equity. The investors in this business will be looking ahead to the point where the business can transition from equity financing to debt financing. Normally, this will be determined up front in the legal documents governing the financ- ing. The debt providers will commit to providing certain levels of debt when certain milestones are reached. One key milestone might be operating cash flow breakeven. At this point the business will still need to invest in capital assets, but it is generating positive cash flow from operations