Answered step by step

Verified Expert Solution

Question

1 Approved Answer

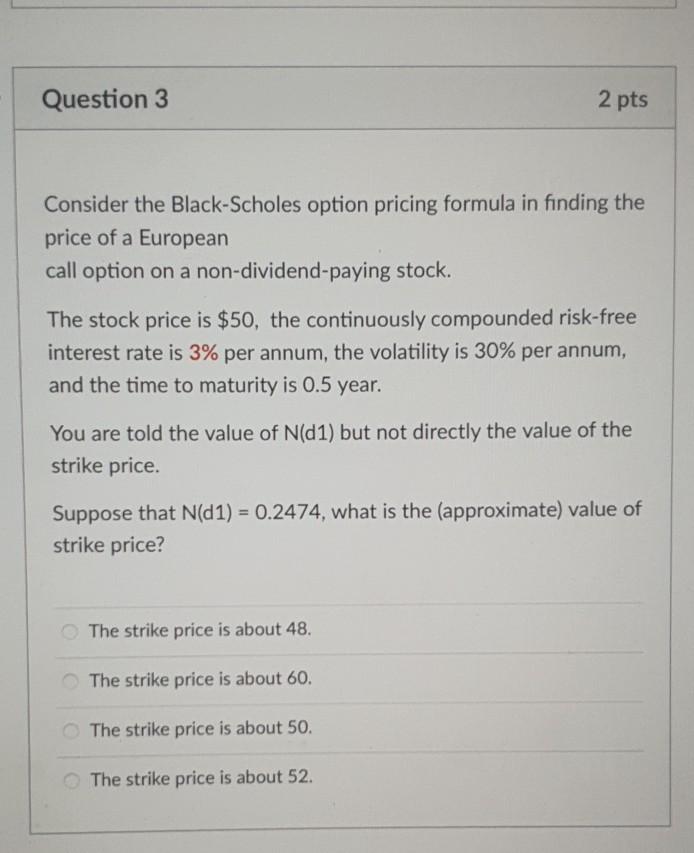

financual math question Question 3 2 pts Consider the Black-Scholes option pricing formula in finding the price of a European call option on a non-dividend-paying

financual math question

Question 3 2 pts Consider the Black-Scholes option pricing formula in finding the price of a European call option on a non-dividend-paying stock. The stock price is $50, the continuously compounded risk-free interest rate is 3% per annum, the volatility is 30% per annum, and the time to maturity is 0.5 year. You are told the value of N(d1) but not directly the value of the strike price. Suppose that N(D1) = 0.2474, what is the approximate) value of strike price? The strike price is about 48. The strike price is about 60. The strike price is about 50. The strike price is about 52Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Global Development Finance The Role Of International Banking 2008

Authors: World Bank

2008 Edition

0821373900, 9780821373903