Answered step by step

Verified Expert Solution

Question

1 Approved Answer

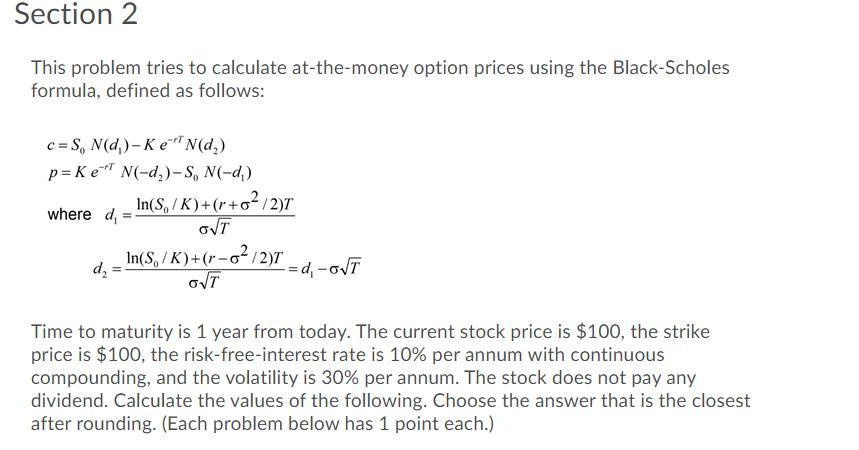

Find N(-d1) in the following question. Section 2 This problem tries to calculate at-the-money option prices using the Black-Scholes formula, defined as follows: CES, N(d)

Find N(-d1) in the following question.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Engines That Move Markets Technology Investing From Railroads To The Internet And Beyond

Authors: Alasdair Nairn

1st Edition

0857195999, 978-0857195999