Answered step by step

Verified Expert Solution

Question

1 Approved Answer

first options ( sell, buy) Problem 1 - Part B (In continuation to the previous problem.) In a financial market, the following three securities are

first options ( sell, buy)

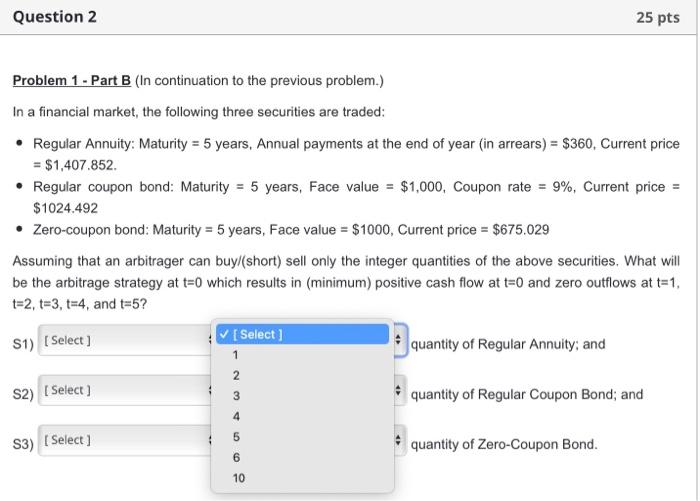

Problem 1 - Part B (In continuation to the previous problem.) In a financial market, the following three securities are traded: - Regular Annuity: Maturity =5 years, Annual payments at the end of year (in arrears) =$360, Current price =$1,407.852. - Regular coupon bond: Maturity =5 years, Face value =$1,000, Coupon rate =9%, Current price = $1024.492 - Zero-coupon bond: Maturity =5 years, Face value =$1000, Current price =$675.029 Assuming that an arbitrager can buy/(short) sell only the integer quantities of the above securities. What will be the arbitrage strategy at t=0 which results in (minimum) positive cash flow at t=0 and zero outflows at t=1, t=2,t=3,t=4, and t=5 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

States And The Reemergence Of Global Finance

Authors: Eric Helleiner

1st Edition

0801428599, 978-0801428593