Answered step by step

Verified Expert Solution

Question

1 Approved Answer

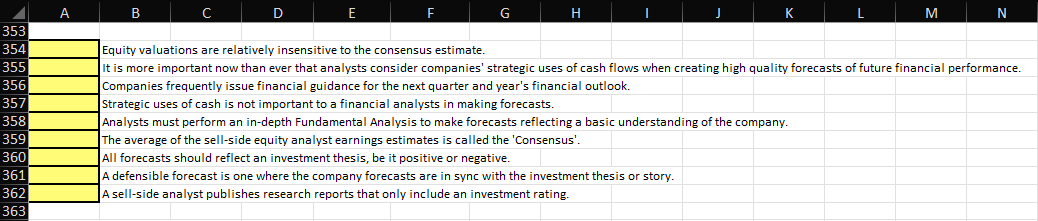

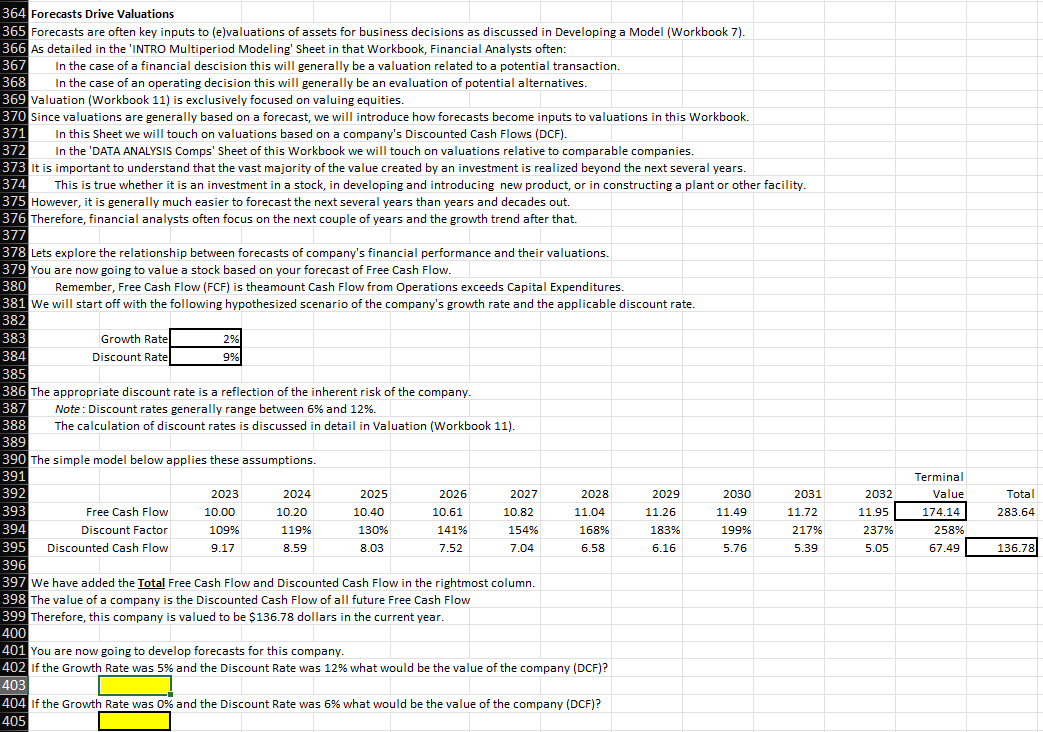

First part is TRUE OR FALSE! Zoom into the image if it is too blury. I need the correct inputs for the yellow cells! A

First part is TRUE OR FALSE!

Zoom into the image if it is too blury. I need the correct inputs for the yellow cells!

A B C D F G H K M N 2 353 354 355 356 357 358 359 360 361 362 363 Equity valuations are relatively insensitive to the consensus estimate It is more important now than ever that analysts consider companies' strategic uses of cash flows when creating high quality forecasts of future financial performance. Companies frequently issue financial guidance for the next quarter and year's financial outlook. Strategic uses of cash is not important to a financial analysts in making forecasts. Analysts must perform an in-depth Fundamental Analysis to make forecasts reflecting a basic understanding of the company. The average of the sell-side equity analyst earnings estimates is called the 'Consensus'. All forecasts should reflect an investment thesis, be it positive or negative. A defensible forecast is one where the company forecasts are in sync with the investment thesis or story. A sell-side analyst publishes research reports that only include an investment rating. 367 364 Forecasts Drive Valuations 365 Forecasts are often key inputs to (e)valuations of assets for business decisions as discussed in Developing a Model (Workbook 7). 366 As detailed in the 'INTRO Multiperiod Modeling' Sheet in that Workbook, Financial Analysts often: In the case of a financial descision this will generally be a valuation related to a potential transaction. 368 In the case of an operating decision this will generally be an evaluation of potential alternatives. 369 Valuation (Workbook 11) is exclusively focused on valuing equities. 370 Since valuations are generally based on a forecast, we will introduce how forecasts become inputs to valuations in this Workbook. 371 In this Sheet we will touch on valuations based on a company's Discounted Cash Flows (DCF). 372 In the 'DATA ANALYSIS Comps' sheet of this Workbook we will touch on valuations relative to comparable companies. 373 It is important to understand that the vast majority of the value created by an investment is realized beyond the next several years. 374 This is true whether it is an investment in a stock, in developing and introducing new product, or in constructing a plant or other facility. 375 However, it is generally much easier to forecast the next several years than years and decades out. 376 Therefore, financial analysts often focus on the next couple of years and the growth trend after that. 377 378 Lets explore the relationship between forecasts of company's financial performance and their valuations. 379 You are now going to value a stock based on your forecast of Free Cash Flow. 380 Remember, Free Cash Flow (FCF) is theamount Cash Flow from Operations exceeds Capital Expenditures. 381 We will start off with the following hypothesized scenario of the company's growth rate and the applicable discount rate. 382 383 Growth Ratel 2% 384 Discount Ratel 9% 385 386 The appropriate discount rate is a reflection of the inherent risk of the company. 387 Note: Discount rates generally range between 6% and 12%. 388 The calculation of discount rates is discussed in detail in Valuation (Workbook 11). 389 390 The simple model below applies these assumptions. 391 392 2023 2024 2025 2026 2027 2028 2029 2030 2031 393 Free Cash Flow 10.00 10.20 10.40 10.61 10.82 11.04 11.26 11.49 11.72 394 Discount Factor 109% 119% 130% 141% 154% 168% 183% 199% 217% 395 Discounted Cash Flow 9.17 8.59 8.03 7.52 7.04 6.58 6.16 5.76 5.39 396 397 We have added the Total Free Cash Flow and Discounted Cash Flow in the rightmost column 398 The value of a company is the Discounted Cash Flow of all future Free Cash Flow 399 Therefore, this company is valued to be $136.78 dollars in the current year. 400 401 You are now going to develop forecasts for this company. 402 If the Growth Rate was 5% and the Discount Rate was 12% what would be the value of the company (DCF)? 403 404 If the Growth Rate was 0% and the Discount Rate was 6% what would be the value of the company (DCF)? 405 Terminal Value 174.14 258% 67.49 2032 11.95 237% 5.05 Total 283.64 136.78 A B C D F G H K M N 2 353 354 355 356 357 358 359 360 361 362 363 Equity valuations are relatively insensitive to the consensus estimate It is more important now than ever that analysts consider companies' strategic uses of cash flows when creating high quality forecasts of future financial performance. Companies frequently issue financial guidance for the next quarter and year's financial outlook. Strategic uses of cash is not important to a financial analysts in making forecasts. Analysts must perform an in-depth Fundamental Analysis to make forecasts reflecting a basic understanding of the company. The average of the sell-side equity analyst earnings estimates is called the 'Consensus'. All forecasts should reflect an investment thesis, be it positive or negative. A defensible forecast is one where the company forecasts are in sync with the investment thesis or story. A sell-side analyst publishes research reports that only include an investment rating. 367 364 Forecasts Drive Valuations 365 Forecasts are often key inputs to (e)valuations of assets for business decisions as discussed in Developing a Model (Workbook 7). 366 As detailed in the 'INTRO Multiperiod Modeling' Sheet in that Workbook, Financial Analysts often: In the case of a financial descision this will generally be a valuation related to a potential transaction. 368 In the case of an operating decision this will generally be an evaluation of potential alternatives. 369 Valuation (Workbook 11) is exclusively focused on valuing equities. 370 Since valuations are generally based on a forecast, we will introduce how forecasts become inputs to valuations in this Workbook. 371 In this Sheet we will touch on valuations based on a company's Discounted Cash Flows (DCF). 372 In the 'DATA ANALYSIS Comps' sheet of this Workbook we will touch on valuations relative to comparable companies. 373 It is important to understand that the vast majority of the value created by an investment is realized beyond the next several years. 374 This is true whether it is an investment in a stock, in developing and introducing new product, or in constructing a plant or other facility. 375 However, it is generally much easier to forecast the next several years than years and decades out. 376 Therefore, financial analysts often focus on the next couple of years and the growth trend after that. 377 378 Lets explore the relationship between forecasts of company's financial performance and their valuations. 379 You are now going to value a stock based on your forecast of Free Cash Flow. 380 Remember, Free Cash Flow (FCF) is theamount Cash Flow from Operations exceeds Capital Expenditures. 381 We will start off with the following hypothesized scenario of the company's growth rate and the applicable discount rate. 382 383 Growth Ratel 2% 384 Discount Ratel 9% 385 386 The appropriate discount rate is a reflection of the inherent risk of the company. 387 Note: Discount rates generally range between 6% and 12%. 388 The calculation of discount rates is discussed in detail in Valuation (Workbook 11). 389 390 The simple model below applies these assumptions. 391 392 2023 2024 2025 2026 2027 2028 2029 2030 2031 393 Free Cash Flow 10.00 10.20 10.40 10.61 10.82 11.04 11.26 11.49 11.72 394 Discount Factor 109% 119% 130% 141% 154% 168% 183% 199% 217% 395 Discounted Cash Flow 9.17 8.59 8.03 7.52 7.04 6.58 6.16 5.76 5.39 396 397 We have added the Total Free Cash Flow and Discounted Cash Flow in the rightmost column 398 The value of a company is the Discounted Cash Flow of all future Free Cash Flow 399 Therefore, this company is valued to be $136.78 dollars in the current year. 400 401 You are now going to develop forecasts for this company. 402 If the Growth Rate was 5% and the Discount Rate was 12% what would be the value of the company (DCF)? 403 404 If the Growth Rate was 0% and the Discount Rate was 6% what would be the value of the company (DCF)? 405 Terminal Value 174.14 258% 67.49 2032 11.95 237% 5.05 Total 283.64 136.78Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Divine Dollars And Digital Gold

Authors: Finally Detached

1st Edition

979-8859504534