Answered step by step

Verified Expert Solution

Question

1 Approved Answer

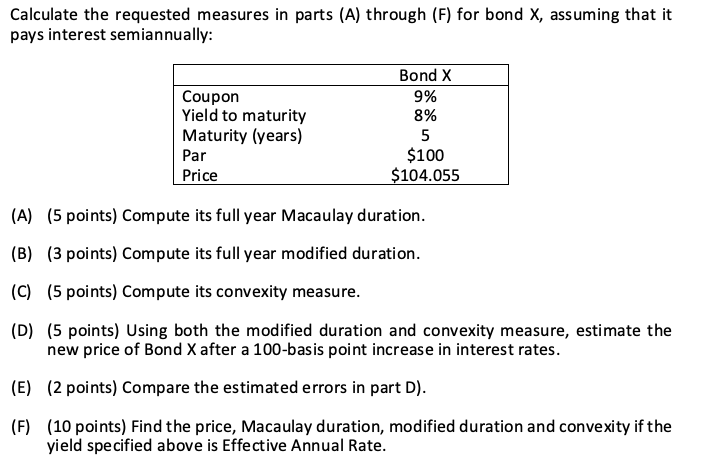

fixed income Calculate the requested measures in parts (A) through (F) for bond X, assuming that it pays interest semiannually: Coupon Yield to maturity Maturity

fixed income

Calculate the requested measures in parts (A) through (F) for bond X, assuming that it pays interest semiannually: Coupon Yield to maturity Maturity (years) Par Price Bond X 9% 8% 5 $100 $104.055 (A) (5 points) Compute its full year Macaulay duration. (B) (3 points) Compute its full year modified duration. (C) (5 points) Compute its convexity measure. (D) (5 points) Using both the modified duration and convexity measure, estimate the new price of Bond X after a 100-basis point increase in interest rates. (E) (2 points) Compare the estimated errors in part D). (F) (10 points) Find the price, Macaulay duration, modified duration and convexity if the yield specified above is Effective Annual Rate. Calculate the requested measures in parts (A) through (F) for bond X, assuming that it pays interest semiannually: Coupon Yield to maturity Maturity (years) Par Price Bond X 9% 8% 5 $100 $104.055 (A) (5 points) Compute its full year Macaulay duration. (B) (3 points) Compute its full year modified duration. (C) (5 points) Compute its convexity measure. (D) (5 points) Using both the modified duration and convexity measure, estimate the new price of Bond X after a 100-basis point increase in interest rates. (E) (2 points) Compare the estimated errors in part D). (F) (10 points) Find the price, Macaulay duration, modified duration and convexity if the yield specified above is Effective Annual RateStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Future Of Pricing How Airline Ticket Pricing Has Inspired A Revolution

Authors: E. Boyd

1st Edition

0230600190,0230606903