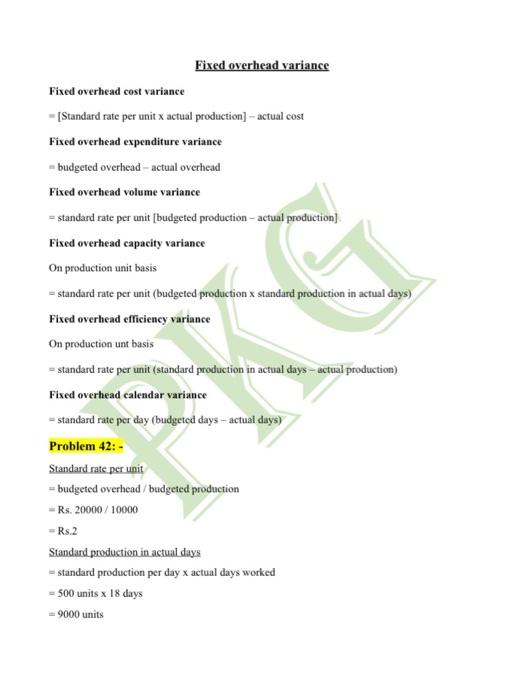

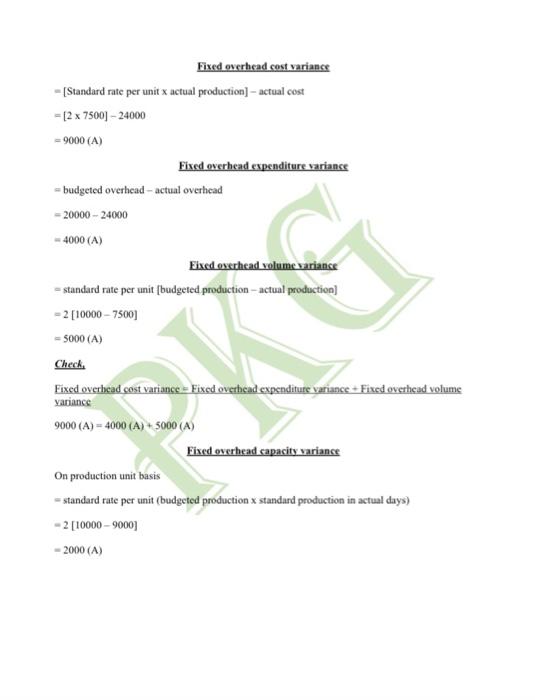

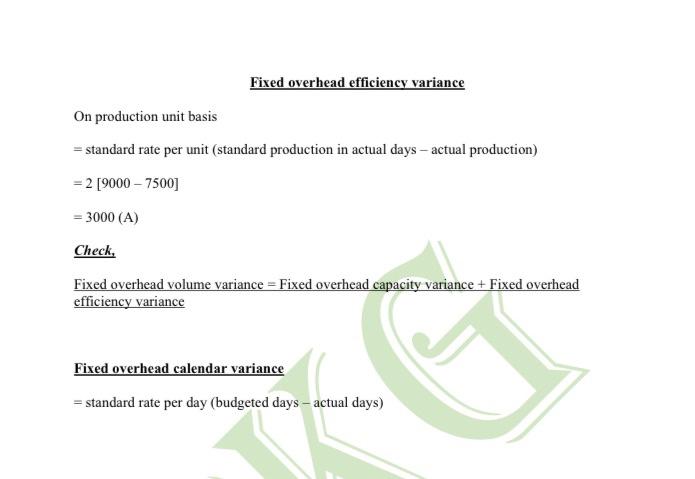

Fixed overhead variance Fixed overhead cost variance - [Standard rate per unit x actual production) actual cost Fixed overhead expenditure variance - budgeted overhead - actual overhead Fixed overhead volume variance = standard rate per unit [budgeted production - actual production) Fixed overhead capacity variance On production unit basis = standard rate per unit (budgeted production x standard production in actual days) Fixed overhead efficiency variance On production unt basis = standard rate per unit (standard production in actual days - actual production) Fixed overhead calendar variance - standard rate per day (budgeted days - actual days) Problem 42:- Standard rate per unit = budgeted overhead / budgeted production = Rs. 20000/10000 - Rs.2 Standard production in actual days - standard production per day x actual days worked = 500 units x 18 days = 9000 units Fixed overhead cost variance - [Standard rate per unit x actual production) actual cost = [2 x 75001 - 24000 - 9000 (A) Fixed overhead expenditure variance - budgeted overhead - actual overhead -20000 - 24000 - 4000 (A) Fixed overhead volume variance standard rate per unit (budgeted production - actual production) -2 [10000 - 7500 - 5000 (A) Check Fixed overhead cost variance - Fixed overhead expenditure variance - Fixed overhead volume variance 9000 (A) = 4000 (A) + 5000 (A) Fixed overhead capacity variance On production unit basis standard rate per unit (budgeted production standard production in actual days) -2 [10000 - 9000) - 2000 (A) Fixed overhead efficiency variance On production unit basis = standard rate per unit (standard production in actual days - actual production) = 2 [9000 - 7500] = 3000 (A) Check, Fixed overhead volume variance = Fixed overhead capacity variance + Fixed overhead efficiency variance Fixed overhead calendar variance = standard rate per day (budgeted days - actual days) Fixed overhead variance Fixed overhead cost variance - [Standard rate per unit x actual production) actual cost Fixed overhead expenditure variance - budgeted overhead - actual overhead Fixed overhead volume variance = standard rate per unit [budgeted production - actual production) Fixed overhead capacity variance On production unit basis = standard rate per unit (budgeted production x standard production in actual days) Fixed overhead efficiency variance On production unt basis = standard rate per unit (standard production in actual days - actual production) Fixed overhead calendar variance - standard rate per day (budgeted days - actual days) Problem 42:- Standard rate per unit = budgeted overhead / budgeted production = Rs. 20000/10000 - Rs.2 Standard production in actual days - standard production per day x actual days worked = 500 units x 18 days = 9000 units Fixed overhead cost variance - [Standard rate per unit x actual production) actual cost = [2 x 75001 - 24000 - 9000 (A) Fixed overhead expenditure variance - budgeted overhead - actual overhead -20000 - 24000 - 4000 (A) Fixed overhead volume variance standard rate per unit (budgeted production - actual production) -2 [10000 - 7500 - 5000 (A) Check Fixed overhead cost variance - Fixed overhead expenditure variance - Fixed overhead volume variance 9000 (A) = 4000 (A) + 5000 (A) Fixed overhead capacity variance On production unit basis standard rate per unit (budgeted production standard production in actual days) -2 [10000 - 9000) - 2000 (A) Fixed overhead efficiency variance On production unit basis = standard rate per unit (standard production in actual days - actual production) = 2 [9000 - 7500] = 3000 (A) Check, Fixed overhead volume variance = Fixed overhead capacity variance + Fixed overhead efficiency variance Fixed overhead calendar variance = standard rate per day (budgeted days - actual days)