Answered step by step

Verified Expert Solution

Question

1 Approved Answer

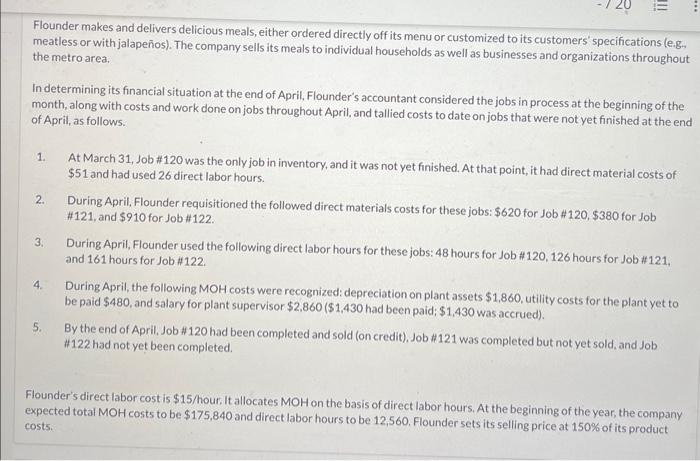

Flounder makes and delivers delicious meals, either ordered directly off its menu or customized to its customer's 'specifications (e.g. meatless or with jalapeos). The company

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Quality Assessment Manual For The Internal Audit Activity

Authors: The Internal Audit Foundation

2017 Edition

0894139975, 978-0894139970