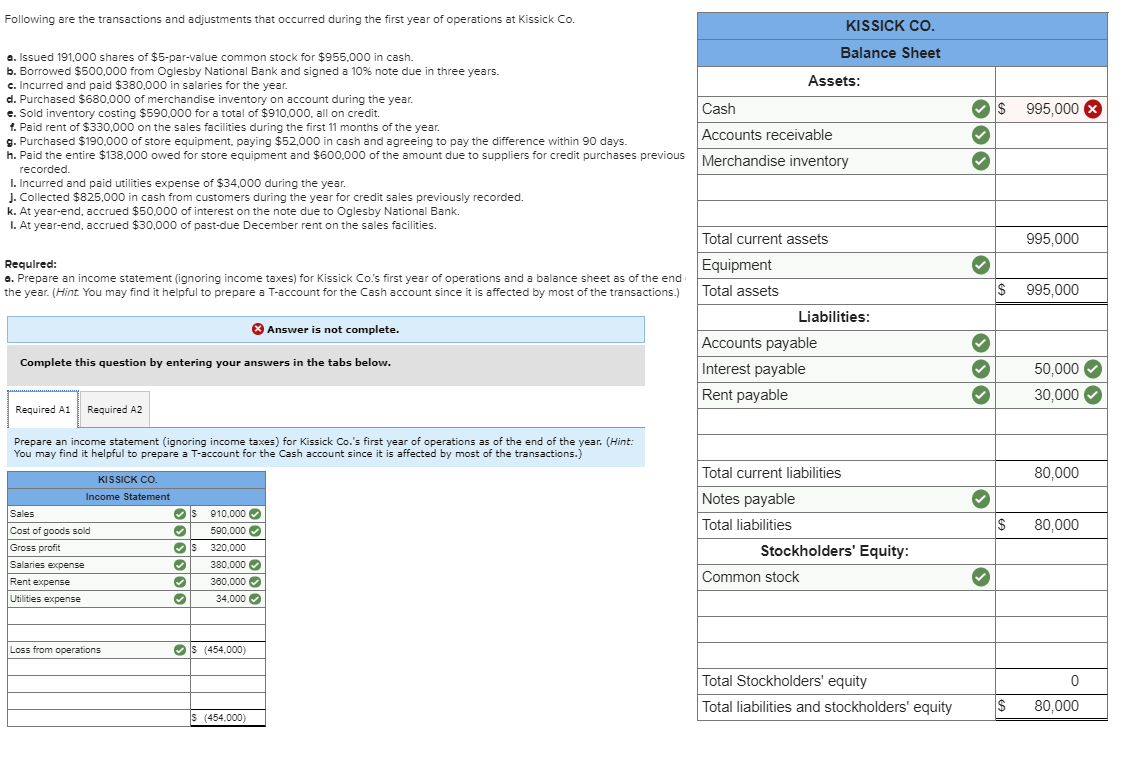

Following are the transactions and adjustments that occurred during the first year of operations at Kissick Co. KIS SICK CO. Balance Sheet Assets: Cash $ 995,000 x a. Issued 191,000 shares of $5-par-value common stock for $955,000 in cash. b. Borrowed $500,000 from Oglesby National Bank and signed a 10% note due in three years. c. Incurred and paid $380,000 in salaries for the year. d. Purchased $680,000 of merchandise inventory on account during the year. e. Sold inventory costing $590.000 for a total of $910,000, all on credit. f. Paid rent of $330,000 on the sales facilities during the first 11 months of the year. g. Purchased $190.000 of store equipment paying $52,000 in cash and agreeing to pay the difference within 90 days. h. Paid the entire $138.000 owed for store equipment and $600,000 of the amount due to suppliers for credit purchases previous recorded. 1. Incurred and paid utilities expense of $34.000 during the year. J. Collected $825.000 in cash from customers during the year for credit sales previously recorded. k. At year-end, accrued $50,000 of interest on the note due to Oglesby National Bank. I. At year-end, accrued $30,000 of past-due December rent on the sales facilities. Accounts receivable Merchandise inventory Total current assets 995,000 Equipment > Required: a. Prepare an income statement (ignoring income taxes) for Kissick Co.'s first year of operations and a balance sheet as of the end the year. (Hint You may find it helpful to prepare a T-account for the Cash account since it is affected by most of the transactions.) $ 995,000 * Answer is not complete. Total assets Liabilities: Accounts payable Interest payable Rent payable Complete this question by entering your answers in the tabs below. 50,000 30,000 Required A1 Required A2 Prepare an income statement (ignoring income taxes) for Kissick Co.'s first year of operations as of the end of the year. (Hint: You may find it helpful to prepare a T-account for the Cash account since it is affected by most of the transactions.) 80,000 KIS SICK CO Income Statement Sales Cost of goods sold Gross profit Salaries expense Rent expense Utilities expense 80,000 Total current liabilities Notes payable Total liabilities Stockholders' Equity: $ 10,000 590,000 320,000 380,000 360.000 34,000 Common stock Loss from operations (454,000) 0 Total Stockholders' equity Total liabilities and stockholders' equity $ 80,000 S (454.000)