Answered step by step

Verified Expert Solution

Question

1 Approved Answer

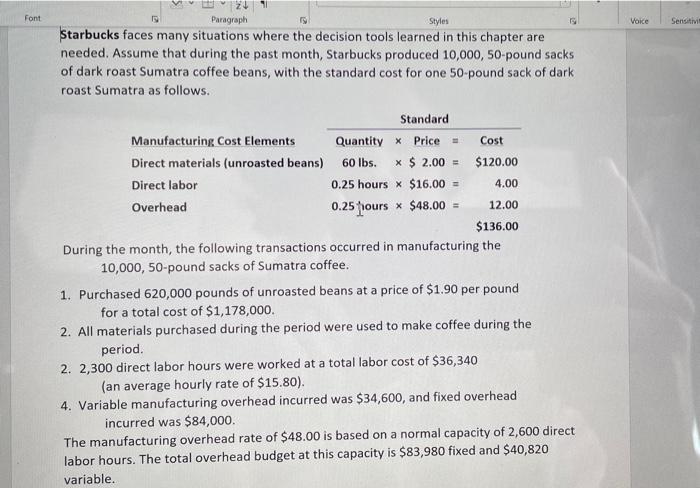

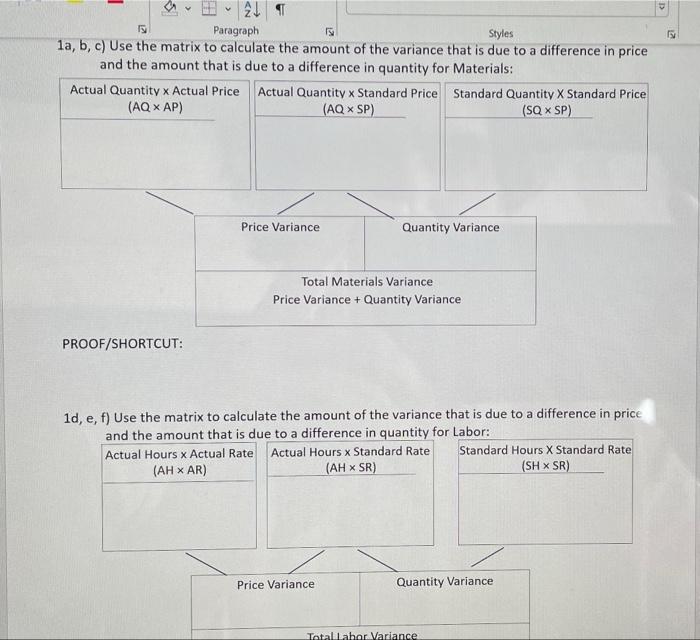

Font Voice Sensitive X Paragraph Styles Starbucks faces many situations where the decision tools learned in this chapter are needed. Assume that during the past

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting

Authors: Robert Libby, Patricia Libby, Frank Hodge

10th Edition

1260481352, 978-1260481358