Question

For Alphabet (GOOG), use strike prices of 1050, Use the options with April 20, 2018 expiration date for all computations, Assume dividends are zero and

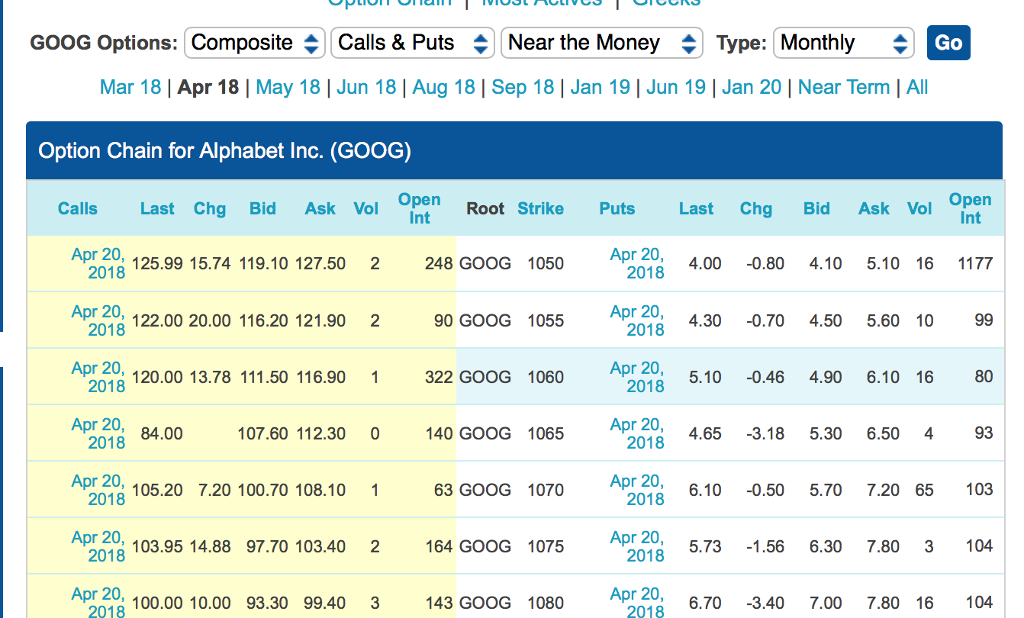

For Alphabet (GOOG), use strike prices of 1050, Use the options with April 20, 2018 expiration date for all computations, Assume dividends are zero and the risk-free interest rate is 2% in all computations . Compute the implied volatilities for puts and calls using mid price data: mid price is the average of the bid and ask prices.

For Alphabet (GOOG), use strike prices of 1050, Use the options with April 20, 2018 expiration date for all computations, Assume dividends are zero and the risk-free interest rate is 2% in all computations . Compute the implied volatilities for puts and calls using mid price data: mid price is the average of the bid and ask prices.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

An Anatomy Of The Financial Crisis

Authors: Nashwa Saleh

1st Edition

0857289616,0857286684