for part c please gove answer using the sharpe ratio and provide a verbal explanation. thank you

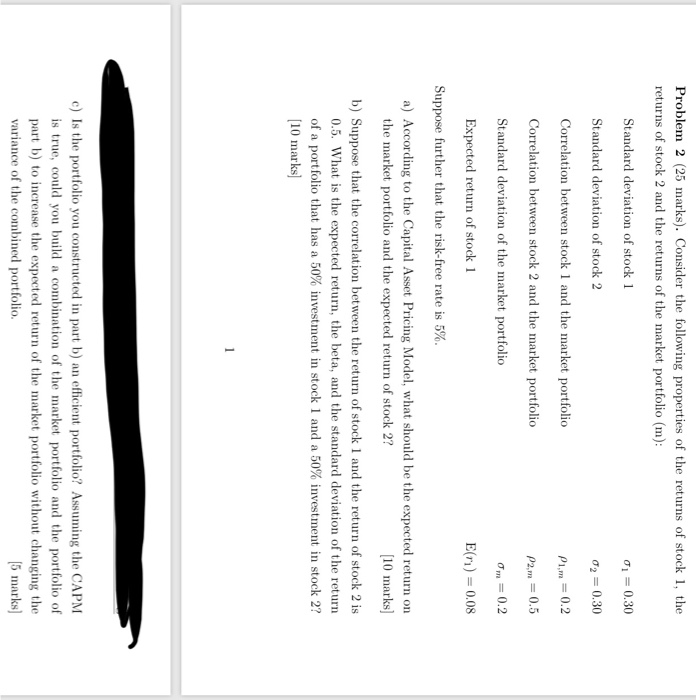

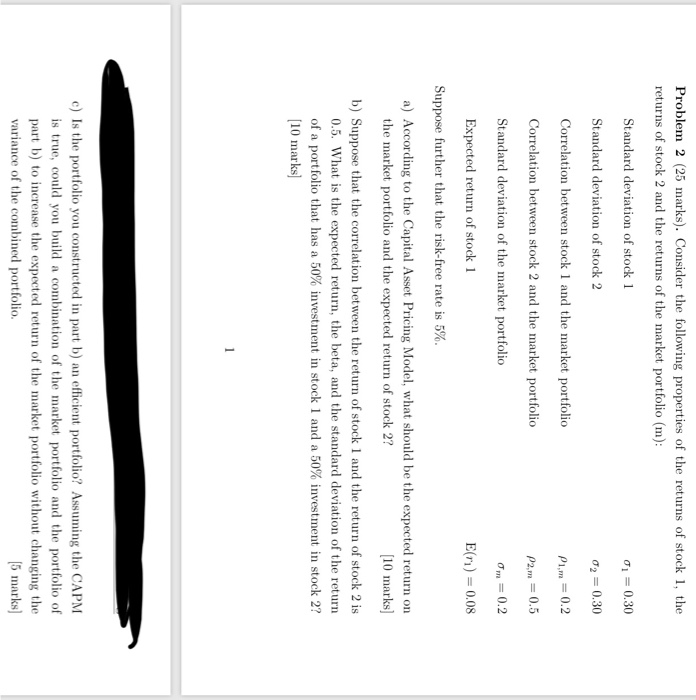

Problem 2 (25 marks). Consider the following properties of the returns of stock 1, the returns of stock 2 and the returns of the market portfolio (m): Standard deviation of stock 1 01 = 0.30 Standard deviation of stock 2 02 = 0.30 Correlation between stock 1 and the market portfolio P1m = 0.2 Correlation between stock 2 and the market portfolio P2m = 0.5 Standard deviation of the market portfolio Om = 0.2 Expected return of stock 1 Eri) = 0.08 Suppose further that the risk-free rate is 5%. a) According to the Capital Asset Pricing Model, what should be the expected return on the market portfolio and the expected return of stock 2? [10 marks) b) Suppose that the correlation between the return of stock 1 and the return of stock 2 is 0.5. What is the expected return, the beta, and the standard deviation of the return of a portfolio that has a 50% investment in stock 1 and a 50% investment in stock 2? (10 marks) c) Is the portfolio you constructed in part b) an efficient portfolio? Assuming the CAPM is true, could you build a combination of the market portfolio and the portfolio of part b) to increase the expected return of the market portfolio without changing the variance of the combined portfolio. 15 marks) Problem 2 (25 marks). Consider the following properties of the returns of stock 1, the returns of stock 2 and the returns of the market portfolio (m): Standard deviation of stock 1 01 = 0.30 Standard deviation of stock 2 02 = 0.30 Correlation between stock 1 and the market portfolio P1m = 0.2 Correlation between stock 2 and the market portfolio P2m = 0.5 Standard deviation of the market portfolio Om = 0.2 Expected return of stock 1 Eri) = 0.08 Suppose further that the risk-free rate is 5%. a) According to the Capital Asset Pricing Model, what should be the expected return on the market portfolio and the expected return of stock 2? [10 marks) b) Suppose that the correlation between the return of stock 1 and the return of stock 2 is 0.5. What is the expected return, the beta, and the standard deviation of the return of a portfolio that has a 50% investment in stock 1 and a 50% investment in stock 2? (10 marks) c) Is the portfolio you constructed in part b) an efficient portfolio? Assuming the CAPM is true, could you build a combination of the market portfolio and the portfolio of part b) to increase the expected return of the market portfolio without changing the variance of the combined portfolio. 15 marks) Problem 2 (25 marks). Consider the following properties of the returns of stock 1, the returns of stock 2 and the returns of the market portfolio (m): Standard deviation of stock 1 01 = 0.30 Standard deviation of stock 2 02 = 0.30 Correlation between stock 1 and the market portfolio P1m = 0.2 Correlation between stock 2 and the market portfolio P2m = 0.5 Standard deviation of the market portfolio Om = 0.2 Expected return of stock 1 Eri) = 0.08 Suppose further that the risk-free rate is 5%. a) According to the Capital Asset Pricing Model, what should be the expected return on the market portfolio and the expected return of stock 2? [10 marks) b) Suppose that the correlation between the return of stock 1 and the return of stock 2 is 0.5. What is the expected return, the beta, and the standard deviation of the return of a portfolio that has a 50% investment in stock 1 and a 50% investment in stock 2? (10 marks) c) Is the portfolio you constructed in part b) an efficient portfolio? Assuming the CAPM is true, could you build a combination of the market portfolio and the portfolio of part b) to increase the expected return of the market portfolio without changing the variance of the combined portfolio. 15 marks) Problem 2 (25 marks). Consider the following properties of the returns of stock 1, the returns of stock 2 and the returns of the market portfolio (m): Standard deviation of stock 1 01 = 0.30 Standard deviation of stock 2 02 = 0.30 Correlation between stock 1 and the market portfolio P1m = 0.2 Correlation between stock 2 and the market portfolio P2m = 0.5 Standard deviation of the market portfolio Om = 0.2 Expected return of stock 1 Eri) = 0.08 Suppose further that the risk-free rate is 5%. a) According to the Capital Asset Pricing Model, what should be the expected return on the market portfolio and the expected return of stock 2? [10 marks) b) Suppose that the correlation between the return of stock 1 and the return of stock 2 is 0.5. What is the expected return, the beta, and the standard deviation of the return of a portfolio that has a 50% investment in stock 1 and a 50% investment in stock 2? (10 marks) c) Is the portfolio you constructed in part b) an efficient portfolio? Assuming the CAPM is true, could you build a combination of the market portfolio and the portfolio of part b) to increase the expected return of the market portfolio without changing the variance of the combined portfolio. 15 marks)