Answered step by step

Verified Expert Solution

Question

1 Approved Answer

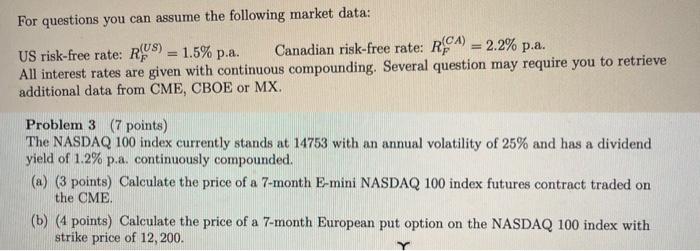

For questions you can assume the following market data: US risk-free rate: RUS) = 1.5% p.a. Canadian risk-free rate: RCA) = 2.2% p.a. All interest

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing A Practical Approach With Data Analytics

Authors: Raymond N. Johnson, Laura Davis Wiley, Robyn Moroney, Fiona Campbell, Jane Hamilton

2nd Edition

1119786045, 978-1119785996