Answered step by step

Verified Expert Solution

Question

1 Approved Answer

FOR THIS PROBLEM, USE TARGET CORPORATION (TGT) AS THE CHOSEN STOCK. that is the one I chose and all I am asking is for you

FOR THIS PROBLEM, USE TARGET CORPORATION (TGT) AS THE CHOSEN STOCK. that is the one I chose and all I am asking is for you to answer PART C. I also used Yahoo Finance

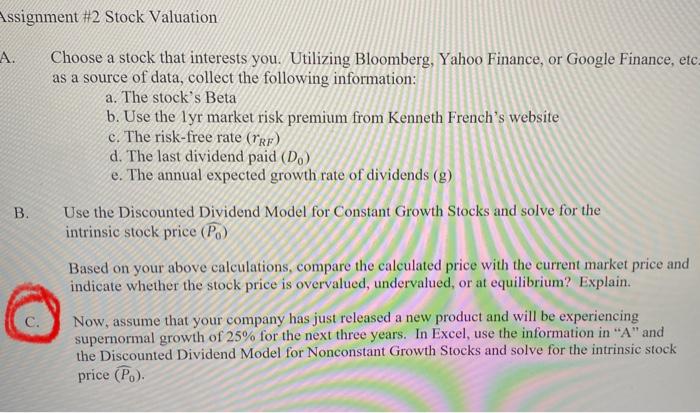

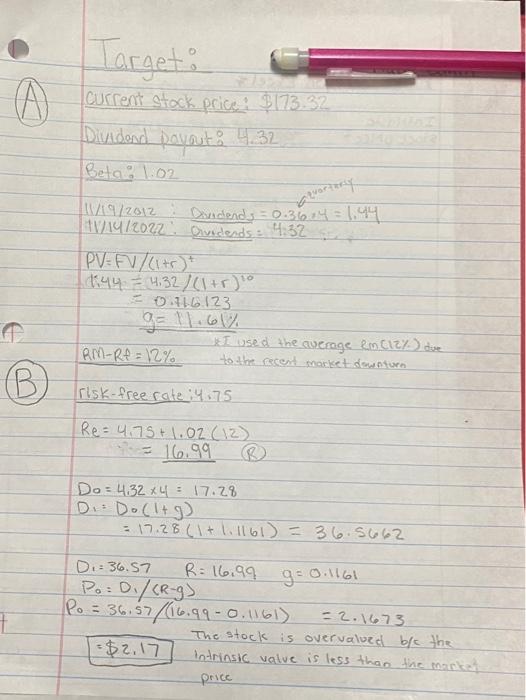

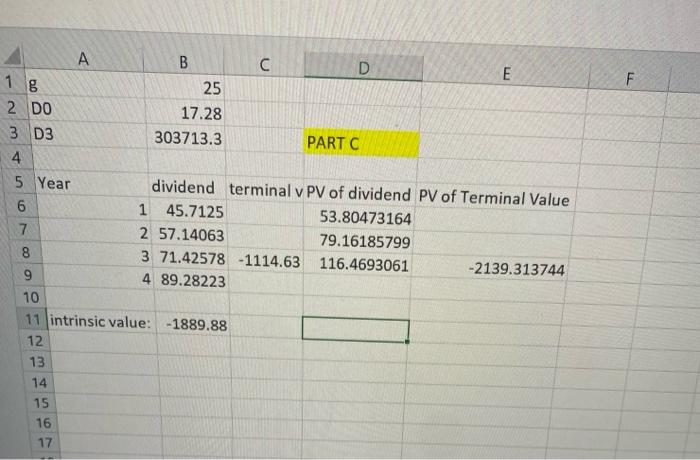

Choose a stock that interests you. Utilizing Bloomberg, Yahoo Finance, or Google Finance, etc as a source of data, collect the following information: a. The stock's Beta b. Use the lyr market risk premium from Kenneth French's website c. The risk-free rate (rRF) d. The last dividend paid (D0) e. The annual expected growth rate of dividends ( g) B. Use the Discounted Dividend Model for Constant Growth Stocks and solve for the intrinsic stock price P0) Based on your above calculations, compare the calculated price with the current market price and indicate whether the stock price is overvalued, undervalued, or at equilibrium? Explain. C. Now, assume that your company has just released a new product and will be experiencing supernormal growth of 25% for the next three years. In Excel, use the information in "A" and the Discounted Dividend Model for Nonconstant Growth Stocks and solve for the intrinsic stock price (P0). 11/19/2012: Axdends =0.36.4=1.44 TW/14/2022: PV=FV/(1+r)t d.44=4.32/(1+r)10 =0.716.123 g=11.6% RMRt=12% osed the average enciz\% risk-free rate: 4.75 Re=4.75+1.02(12) =16.99 (B) D0=4.324=17.28 D1=D0(1+g) =17.28(1+1.1161)=36.5662 D1=36.57R=16.99g=0.1161 P0=D1/(Rg) 0=36.57/(16.990.1161)=2.1673 i have aready solved the whole problem and will attach my work for it to help, i dont think i did part C right and need help solving it.

for the problem, my professor asked us to use 12% for Rm-Rf

Thank you.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Financial Markets Dynamics And Evolution

Authors: Thorsten Hens

1st Edition

0323165478, 978-0323165471