Answered step by step

Verified Expert Solution

Question

1 Approved Answer

for this question part B when calculating the 4 year bonds no-arbitrage price should i the different rates for each year, or should i just

for this question part B when calculating the 4 year bonds no-arbitrage price should i the different rates for each year, or should i just use the same rate of z4 when discounting all cash flows of bond B

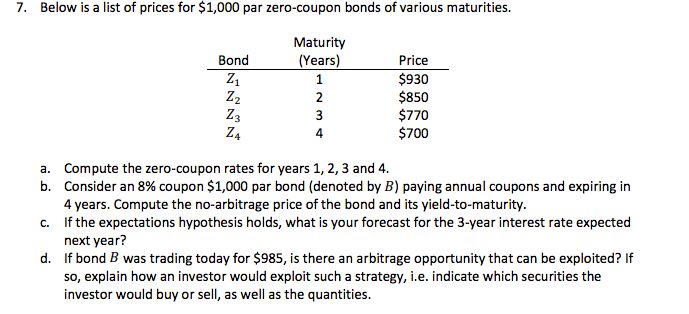

7. Below is a list of prices for $1,000 par zero-coupon bonds of various maturities. Maturity (Years) Bond Price $930 $850 $770 $700 a. Compute the zero-coupon rates for years 1, 2, 3 and 4. b. Consider an 8% coupon $1,000 par bond (denoted by B) paying annual coupons and expiring in 4 years. Compute the no-arbitrage price of the bond and its yield-to-maturity. c. If the expectations hypothesis holds, what is your forecast for the 3-year interest rate expected next year? d. If bond B was trading today for $985, is there an arbitrage opportunity that can be exploited? If so, explain how an investor would exploit such a strategy, i.e. indicate which securities the investor would buy or sell, as well as the quantitiesStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Research In Finance

Authors: John W. Kensinger

1st Edition

0857245414, 978-0857245410