Answered step by step

Verified Expert Solution

Question

1 Approved Answer

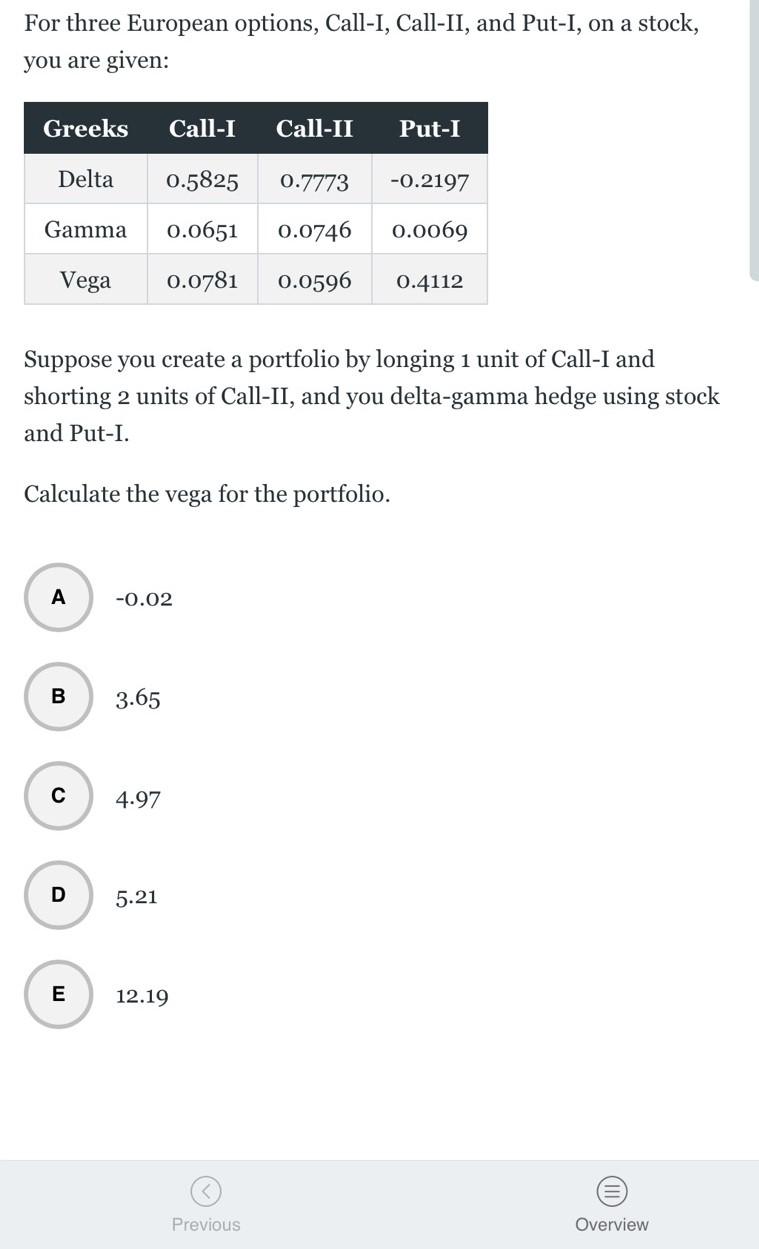

For three European options, Call-I, Call-II, and Put-I, on a stock, you are given: Greeks Call-I Call-II Put-I Delta 0.5825 0.7773 -0.2197 Gamma 0.0651 0.0746

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Real Estate Investment Strategies Structures Decisions

Authors: David Hartzell, Andrew E. Baum

2nd Edition

1119526094, 978-1119526094