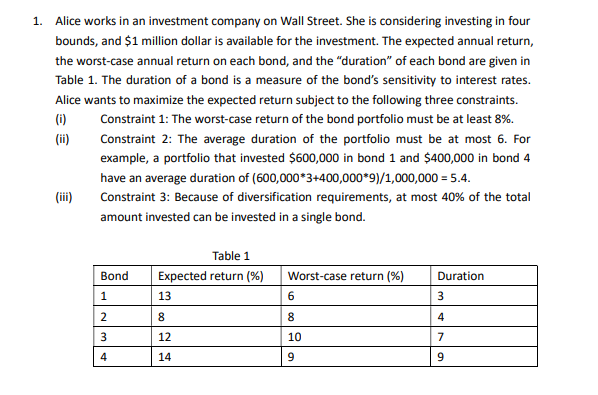

Question

Formulate the following problems into linear programming models. Clearly define your decision variables, objective function, and constraints. For each constraint, explain, in complete sentences, how

Formulate the following problems into linear programming models. Clearly define your decision variables, objective function, and constraints. For each constraint, explain, in complete sentences, how it works. If your model uses both parameters and decision variables, make sure that you indicate which is which. Finally, explain why the model that you propose is a linear optimization problem.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Exploring Public Relations Global Strategic Communication

Authors: Ralph Tench, Liz Yeomans

4th Edition

1292112182, 9781292112183