Answered step by step

Verified Expert Solution

Question

1 Approved Answer

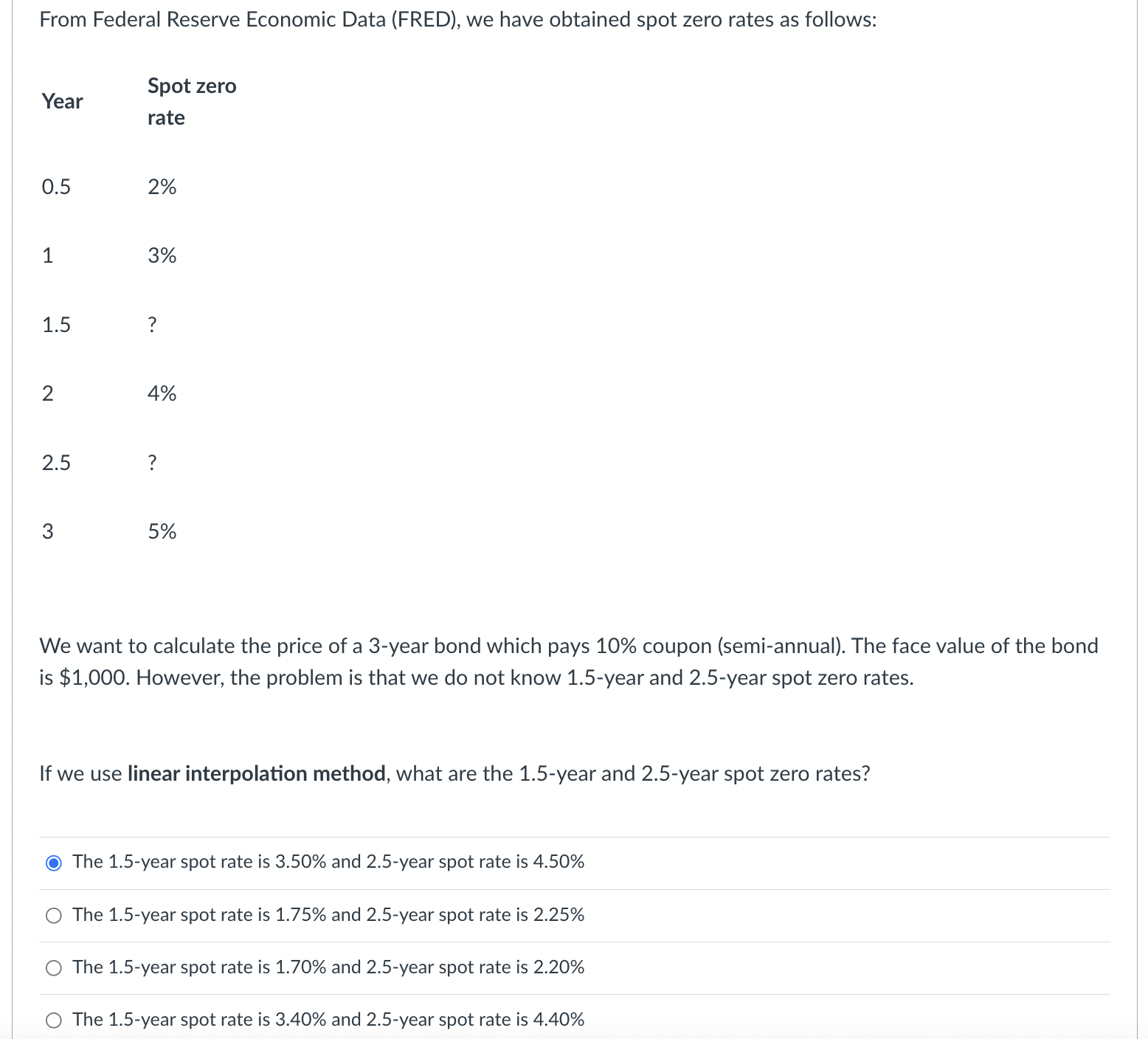

From Federal Reserve Economic Data ( FRED ) , we have obtained spot zero rates as follows: Year Spot zero rate 0 . 5 2

From Federal Reserve Economic Data FRED we have obtained spot zero rates as follows:

Year

Spot zero

rate

We want to calculate the price of a year bond which pays coupon semiannual The face value of the bond

is $ However, the problem is that we do not know year and year spot zero rates.

If we use linear interpolation method, what are the year and year spot zero rates?

The year spot rate is and year spot rate is

The year spot rate is and year spot rate is

The year spot rate is and year spot rate is

The year spot rate is and year spot rate is

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Stocks Bonds And Taxes A Comprehensive Handbook And Investment Guide For Everybody

Authors: Phillip B. Chute

1st Edition

1732885532, 978-1732885530