Question

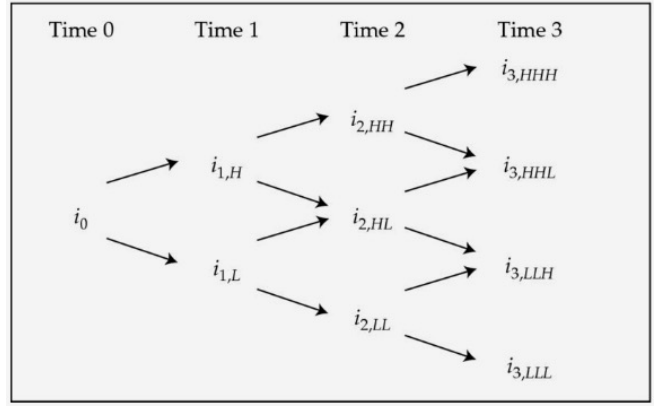

From the spot rates, find the 1y1y, 2y1y forward rates and assume that interest rates follow a lognormal random walk, Given a volatility of 20%,

From the spot rates, find the 1y1y, 2y1y forward rates and assume that interest rates follow a lognormal random walk, Given a volatility of 20%, construct the binomial interest rate tree. (Probability of high vs. low states are equal.)

| years | spot rate |

| 1 | 0.65% |

| 2 | 0.876% |

| 3 | 1.118% |

Time 0 Time 1 Time 2 Time 3 13,HHH in,H 11,H 13,HHL io 12,HL ill 13,LLH 12,LL 13,LLL Time 0 Time 1 Time 2 Time 3 13,HHH in,H 11,H 13,HHL io 12,HL ill 13,LLH 12,LL 13,LLL

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Engineers Cost Handbook Tools For Managing Project Costs

Authors: Richard E. Westney

1st Edition

0824797965, 978-0824797966